Travel to Work Tax Deduction: An ATO Guide for 2026

Can you claim a travel to work tax deduction in Australia? Our 2026 guide explains ATO rules, calculation methods, and record-keeping for SMEs and founders.

Ansh Malhotra

Most advice on the travel to work tax deduction is too blunt to be useful. You'll hear, “commuting isn't deductible,” and that's often true. But it's not the full answer founders, contractors, and finance teams need when real work happens across client sites, depots, job locations, temporary offices, and hybrid setups.

The expensive mistake isn't only claiming too much. It's also failing to claim what the rules do allow because nobody explained the distinction properly. The ATO doesn't just look at whether you got in a car and went somewhere for work. It looks at the connection between the trip and your income-earning activity. That's where many claims succeed or fail.

For Australian businesses, this issue matters more than people think. A legitimate deduction can have a meaningful tax effect for higher-income owners because the top marginal income tax rate is 45%, plus the 2% Medicare levy, as noted in KBS Chartered Accountants on Australian travel deduction rules. But the same rules can also expose weak claims very quickly if your records are thin or your team treats ordinary commuting as business travel.

This guide deals with the part most articles skip. It covers when travel can move from private to deductible, how to choose between the car claim methods, what records hold up, and why employers also need to think about reimbursement and FBT consequences.

Table of Contents

Introduction The Truth About Your Commute and Tax

If you drive from home to your usual office each morning, that trip usually isn't deductible. It doesn't matter that the drive is essential for you to show up and do your job. For tax purposes, that's still generally treated as private travel, not income-producing travel.

That answer frustrates people because it feels artificial. From a business owner's point of view, getting to work feels inseparable from earning money. The ATO draws the line differently. It asks whether the travel itself happened in the course of earning income, or whether it only got you to the place where earning income begins.

That distinction sounds technical, but in practice it's straightforward. A chef driving to their restaurant is commuting. A chef driving from the restaurant to a second event venue to cater a function is travelling for work. Same car, same person, different tax result.

Practical rule: Don't judge a trip by its destination alone. Judge it by its role in the workday.

Many founders and contractors often miss valid claims. The strongest opportunities often sit in the middle of the day, not at the start of it. Multi-site work, temporary job locations, site visits, and travel between separate work obligations can all change the analysis.

A proper travel to work tax deduction review should also look beyond the individual. If your company reimburses travel, provides a vehicle, or covers costs for hybrid staff, there may be payroll and FBT consequences even where the employee can't personally claim the trip.

The ATO's Golden Rule of Travel Deductions

The test that decides everything

The rule is stricter than many business owners expect. A travel expense is only deductible if it is incurred in gaining or producing assessable income, and it is not private or domestic in character. For travel claims, the key question is whether the trip forms part of the income-earning activity itself, or whether it only gets you to the place where work starts.

A simple comparison helps. Driving to your accountant's office to sign your tax return is personal. Driving from your office to a client site to inspect a job is part of doing the work. Travel deductions follow that same logic. The cost must attach to the work activity, not to your private choice of where you live or how you get to your regular base.

That is the ATO's golden rule. Focus on the character of the trip, not the fact that work sits at the end of it.

Why the commute often fails

Home-to-work travel is commonly denied because the ATO treats it as private expenditure. The trip may be necessary in a practical sense, but tax law asks a narrower question. Did the travel happen while you were earning income, or did it only put you in position to begin earning it?

For a founder or contractor, that distinction matters more than intent. A long drive, an early start, or the lack of public transport does not change the character of the trip. ATO guidance on car and travel expenses makes that line clear, particularly for travel to a regular workplace and for claims that need written evidence and a travel diary for certain overnight trips, as explained on the Australian Taxation Office website.

The practical test is the work nexus. If the trip happens in the course of carrying on duties, the claim has a path. If the trip is just the morning commute to your usual place of work, it stays private.

Records decide close cases.

Wolters Kluwer's discussion of business-related travel expenses makes the point well. The stronger the evidence connecting the trip to a work task, the easier it is to defend the deduction. In practice, that means diary notes, client addresses, rosters, job sheets, meeting confirmations, and logbook entries that let an outsider trace the day without relying on your memory.

A good rule of thumb is to ask one blunt question. Would this trip have occurred in the same way if there were no work duty attached? If the answer is yes, the expense is likely private. If the answer is no because the travel arose from a client visit, a second work location, or a temporary assignment, the claim may be deductible, provided the records support it.

For employers, there is another layer. Reimbursing or paying for travel does not automatically make it deductible to the employee, and it does not remove fringe benefits tax risk. If the underlying trip is private, the tax issue may shift from an income tax deduction question to an FBT compliance problem.

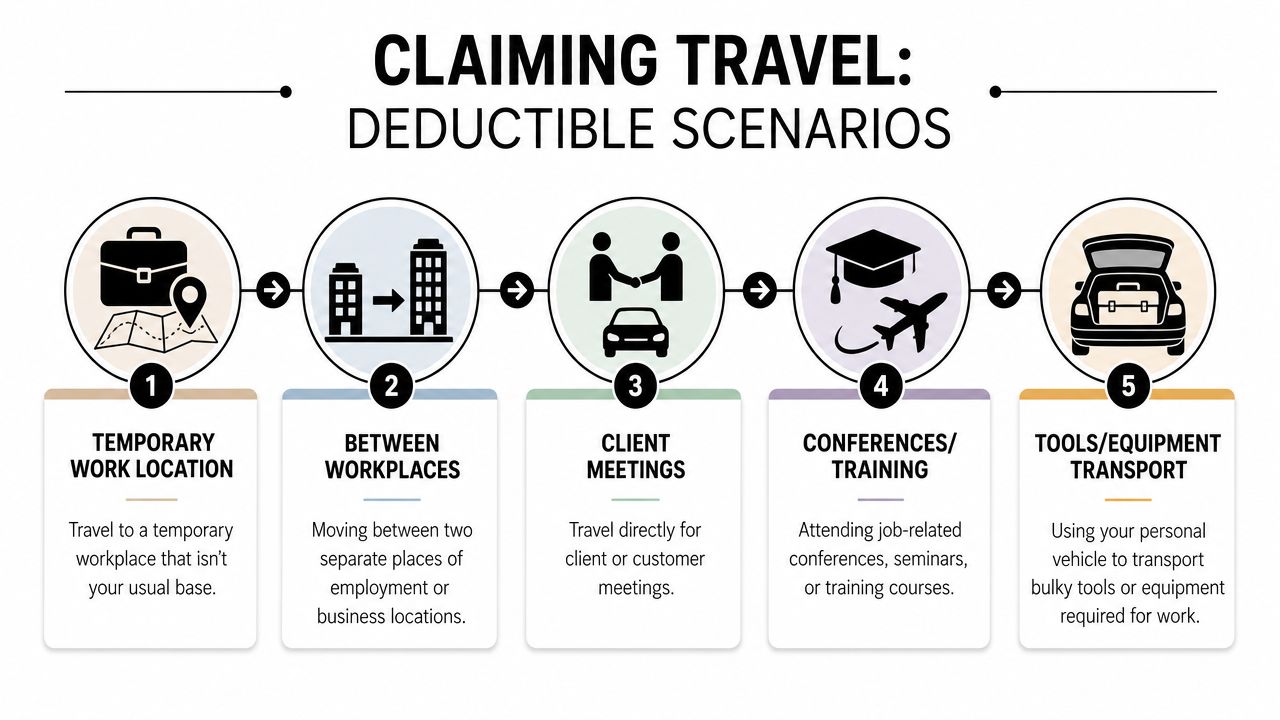

Deductible Travel Scenarios You Can Actually Claim

The best claims are rarely glamorous. They're ordinary trips that sit clearly inside the workday and are supported by records.

When the trip becomes part of the job

A common deductible scenario is travel between workplaces. If a founder visits the warehouse in the morning and then drives to a retail site, that travel is part of carrying on the business. The same applies where an employee moves from their usual office to a client meeting, or from one employer location to another.

Another legitimate category is travel between separate jobs. If someone has two distinct income-earning roles and travels directly from one to the other, that travel can take on a deductible character.

Then there's the temporary workplace situation. This is one of the most misunderstood areas. If the worker is travelling to a location that isn't their regular base and the trip arises because work duties have temporarily moved there, the tax outcome can be different from ordinary commuting.

The exceptions people miss

The biggest blind spot is the sequence of work locations across a day. Many people search for a travel to work tax deduction expecting a yes or no answer about the morning commute. That misses where key opportunities usually sit. Trout CPA's discussion of transportation and travel to the office notes that travel may become deductible when a worker is moving between jobsites, carrying bulky equipment, or starting from a genuine home office that is a place of business.

That matters for tradies, mobile operators, consultants, and sales staff. If the day starts at a real business base at home and continues to changing work sites, the analysis is very different from someone leaving the house and driving to their usual office tower.

Examples make this easier:

Tradie with multiple sites: The day starts with loading required equipment, then travelling across several jobsites. The most valuable claim often sits in the pattern of site-to-site movement.

Consultant visiting clients: Home to regular office is usually private. Office to client and client to second client is a different category.

Director working across locations: Driving from a head office to a warehouse, then to a supplier meeting, is travel within the business activity.

Worker carrying bulky tools: This can change the position, but only in narrow circumstances. The tools must be required for work, not merely convenient to bring along.

If you want to improve a travel claim, map the day, not just the first trip.

A genuine home office that is a place of business can also change the result. That's a narrow concept. A desk in the spare room used for occasional admin isn't automatically enough. The home location has to function as a real business base, not just a convenient place to answer emails.

The practical lesson is clear. Don't ask, “Can I claim my commute?” Ask, “Which trips in my work pattern were part of producing income?”

How to Calculate Your Car Expense Deduction

Choosing the wrong method doesn't just create admin pain. It can leave money on the table or produce a claim you can't support.

Two methods with very different outcomes

For motor vehicle claims, the ATO allows either the cents per kilometre method or the logbook method. The tax effect can differ materially because the logbook approach lets you claim the business-use percentage of running costs, while the cents-per-kilometre method is capped and is often simpler to run, as explained in KMCo's guide to deductible business travel expenses.

The practical trade-off is simple. The cents per kilometre method suits people with relatively low business travel and a preference for ease. The logbook method usually rewards taxpayers with frequent work travel, mixed business and private use, or higher actual vehicle costs.

If you run a ute, SUV, or other vehicle with meaningful fuel, insurance, servicing, and ownership costs, don't assume the simple method is best. Simplicity has a price.

For businesses looking at alternative transport options, especially where staff or owners use bikes or e-bikes for city travel, it's also worth thinking about the broader risk and cost picture. A practical example is this guide to Punk Ride insights on e-bike insurance, which helps frame why transport decisions should be documented and assessed as part of overall operating policy, not just tax.

Cents per kilometre vs logbook method at a glance

Aspect | Cents Per Kilometre Method | Logbook Method |

|---|---|---|

How it works | Claim using business kilometres travelled | Claim business-use percentage of car running costs |

Best fit | Lower-kilometre users who want a simpler process | Businesses with regular work travel or higher vehicle costs |

Main strength | Less paperwork day to day | Often produces a stronger claim where business use is substantial |

Main limitation | Capped annual claim per car | Requires stronger substantiation and ongoing discipline |

Receipts | Doesn't require individual expense receipts for each trip | Requires records for actual running costs |

Key compliance focus | Reasonable basis for kilometres claimed | Contemporaneous logbook, odometer records, and cost evidence |

A useful way to think about it is this. The cents-per-kilometre method is like using a standard meal allowance when you want convenience. The logbook method is like itemising every actual cost because you know the details matter.

For many founders, the right answer isn't permanent. If travel patterns change, your best method may change too. A business that starts with low site travel may later open another location, add field staff, or increase client visits. At that point, the more detailed method often becomes commercially sensible as well as tax-effective.

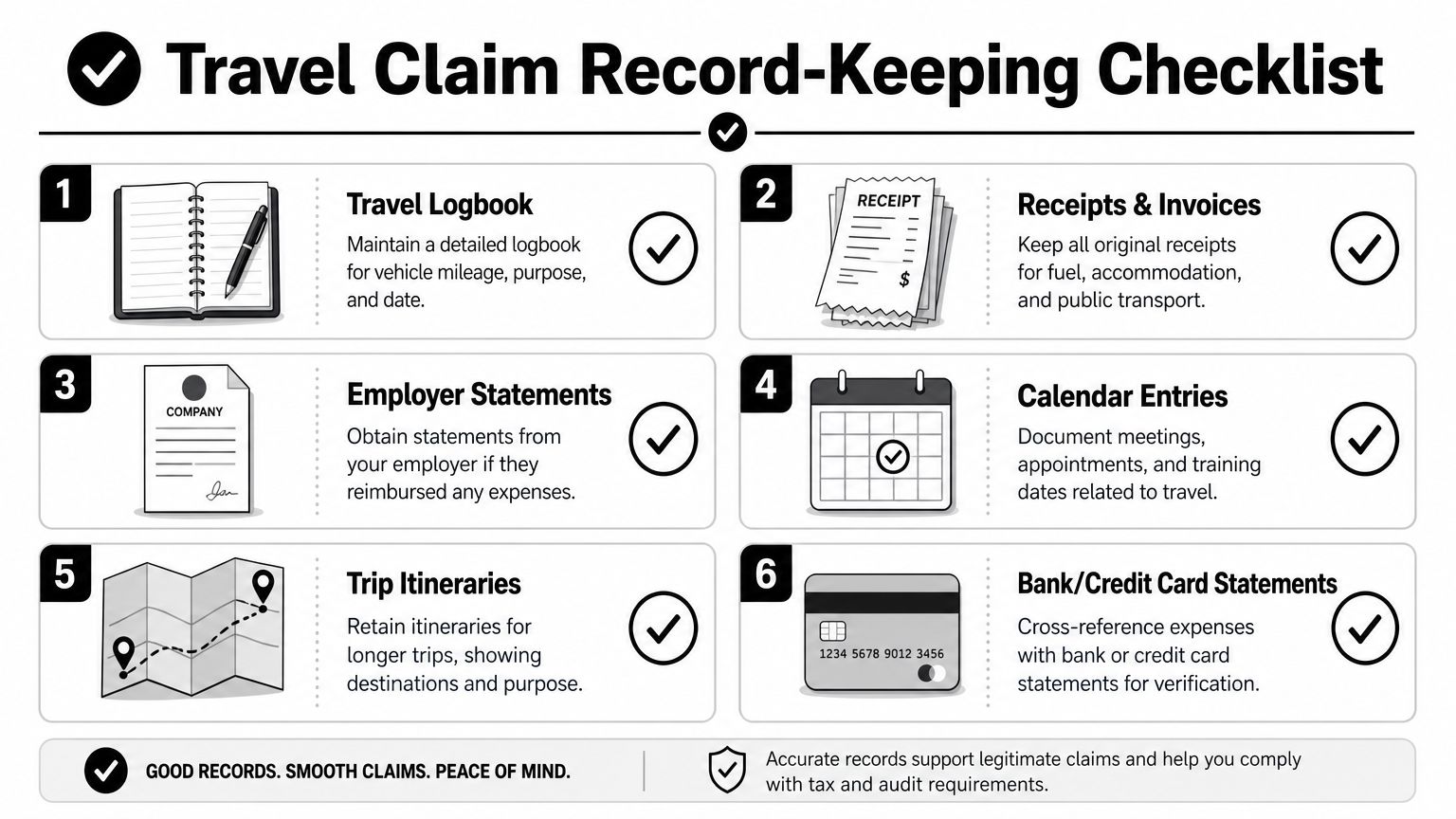

Record-Keeping The ATO Expects for Travel Claims

A deduction with weak records isn't a deduction. It's an argument waiting to happen.

Evidence turns a story into a deduction

The ATO's approach to travel claims is document-heavy because travel is easy to blur with private activity. That's why the control point isn't enthusiasm. It's evidence.

If you use the cents-per-kilometre method, you still need to show that your kilometre estimate is reasonable. If you use the logbook method, contemporaneous records become the backbone of the claim. In both cases, the trip purpose matters just as much as the distance.

I usually tell clients to build records as if someone else will need to understand them six months later. “Client meeting” is weak. “Client meeting at Port Melbourne warehouse re stock discrepancy” is much better.

What a defensible record set looks like

A solid record trail usually includes:

Trip details: Date, start and finish locations, kilometres travelled, and the business purpose.

Odometer support: Opening and closing readings where relevant, especially if you use a logbook approach.

Expense evidence: Fuel, servicing, registration, insurance, tolls, parking, and other actual running costs if your method requires them.

Calendar proof: Diary entries, appointment confirmations, site schedules, and meeting invites.

Payment trace: Bank or card statements that line up with the receipts.

For teams trying to standardise this process, good expense capture software can save a lot of rework. If you're reviewing systems, these Xpenses accounting software recommendations are a useful starting point because they focus on practical small-business workflows rather than theory. The same principle applies if you're cleaning up finance processes more broadly. This article on accounts payable automation in Australia is useful if your receipts, approvals, and reimbursements are still spread across inboxes and paper folders.

Clean records do two jobs. They support the claim and they reduce the time your team spends defending it.

One more point matters for overnight travel. Written evidence is generally required for work-related travel expenses, and travel diary requirements can apply in longer overnight situations. If your people travel regularly, make diary completion part of the trip process, not an afterthought at tax time.

Rules for Employees Contractors and SMEs

Tax treatment changes depending on who incurs the cost and who claims it.

Employees claiming personally

Employees need to be careful because many travel costs feel work-related without meeting the deduction test. A regular trip from home to the office usually remains private even if the employee works long hours, carries a laptop, or has no practical public transport option.

The issue for SMEs is that staff often assume reimbursement and deductibility are the same thing. They're not. An employee may have no personal deduction for a trip, yet the employer still needs to decide whether paying or reimbursing that cost creates another tax consequence.

For a growing business, that's where finance leadership matters. If your team is setting reimbursement policy, vehicle policy, and payroll treatment at the same time, the tax answer needs to align with operating reality. That's one reason founders often bring in virtual chief financial officer support when travel, payroll, and reporting processes start overlapping.

When the business pays instead

For Australian SMEs, one of the more nuanced issues is whether an employer can reimburse home-to-office travel tax-effectively. Australian FBT guidance distinguishes between ordinary commuting and travel that is part of performing duties, with treatment depending on the facts. The ATO's compliance focus on substantiation has also intensified recently, as discussed in HR Block's business travel deduction guidance.

That means a founder shouldn't assume that “the company paid for it” solves the problem. It may solve the employee cashflow issue while creating an FBT or payroll issue for the business.

Here's a useful summary video on the broader tax treatment businesses need to keep in mind before reimbursing travel costs.

Contractors and sole traders often sit in a cleaner position because they usually claim business travel directly in the business context. Even then, the same core problem remains. If the trip is private in character, the business structure won't rescue it.

Reimbursement changes who pays first. It doesn't automatically change the nature of the trip.

The practical answer for SMEs is to set written travel rules. Define ordinary commuting, define site-to-site travel, require evidence before reimbursement, and review any recurring home-to-office support through an FBT lens before it becomes habit.

Common Pitfalls and Your Tax-Time Checklist

Mistakes that trigger trouble

The most common error is claiming the everyday commute because it feels work-related. The second is having a story that makes sense commercially but not enough records to prove the tax treatment. The third is choosing a car claim method for convenience without checking whether it still fits the year's actual travel pattern.

Other problems are more subtle:

Mixing trip types: Including private errands in business kilometre totals.

Weak descriptions: Recording “meeting” without naming the site, client, or job purpose.

Assuming a home office fixes everything: It doesn't. A genuine place of business is a narrower concept.

Ignoring employer consequences: Reimbursing staff travel without checking FBT treatment.

A practical checklist and quick FAQ

Before lodging a claim, run through this short list:

Identify the trip type. Was it ordinary commuting, travel between workplaces, a temporary site visit, or another work-connected trip?

Match the method to the facts. If your vehicle costs are significant and business use is regular, compare the simple method with a logbook outcome.

Pull the evidence together. Calendar, receipts, invoices, payment records, odometer support, and job details should line up.

Review reimbursements separately. Employee deduction rules and employer tax treatment aren't always the same.

Test the claim objectively. If a third party read the records, would the business purpose be obvious?

A few quick answers to common edge cases:

Can you claim tolls and parking? They may be claimable when attached to deductible work travel. Their treatment follows the character of the underlying trip.

Is public transport deductible? It can be where the travel itself is work-related rather than ordinary commuting.

Does having a home office make office travel deductible? Not automatically. The home setup must amount to a genuine place of business, not just a place where some work gets done.

What if another tax article says something different? Check the facts and records first. Broad summaries often miss the details that decide the result. The same applies in other deduction areas, including health-related questions people often misunderstand, such as those covered in this guide on claiming medical expenses on taxes.

If you want clearer answers on travel claims, reimbursements, FBT exposure, and the finance systems behind them, Nexist helps Australian founders turn messy tax and cashflow questions into clean operating decisions.

travel to work tax deduction, ato travel expenses, car expense deductions, logbook method australia, small business tax deductions

" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="dSFdkJotL" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="wscNJE44G" transform="translate(0 0.129)" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="sTpjGo1tb" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="s7ffpmKOD" transform="translate(0 0.129)" width="24px"/><g d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.000006px" id="D0ecaHEcW" transform="translate(0 0)" width="24px"><path d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z" fill="rgb(55, 184, 218)" height="24.000006px" id="IPLFE6zXx" width="24px"/><path d="M 4.02 0 L 0 0 L 0 12.092 L 4.02 12.092 Z" fill="rgb(255, 255, 255)" height="12.09201px" id="FWhtzAyuY" transform="translate(2.863 8.375)" width="4.02px"/><path d="M 2.274 0 C 0.899 0 0 0.904 0 2.089 C 0 3.25 0.871 4.179 2.221 4.179 L 2.247 4.179 C 3.648 4.179 4.521 3.25 4.521 2.089 C 4.495 0.904 3.649 0 2.274 0 Z" fill="rgb(255, 255, 255)" height="4.17876px" id="VmOsKv4kO" transform="translate(2.625 2.545)" width="4.52095px"/><path d="M 7.641 0 C 5.509 0 4.554 1.173 4.019 1.996 L 4.019 0.284 L 0 0.284 C 0.053 1.419 0 12.376 0 12.376 L 4.019 12.376 L 4.019 5.623 C 4.019 5.262 4.045 4.9 4.151 4.642 C 4.442 3.92 5.103 3.172 6.214 3.172 C 7.667 3.172 8.25 4.282 8.25 5.907 L 8.25 12.376 L 12.269 12.376 L 12.269 5.442 C 12.269 1.728 10.286 0 7.641 0 Z" fill="rgb(255, 255, 255)" height="12.37626px" id="n1XUbhaq0" transform="translate(9.105 8.09)" width="12.268830000000001px"/></g></g></g></g></svg>)