Accounting Business Advisory: Grow Your Australian SME

Unlock growth with accounting business advisory. Our guide for Australian SMEs explains how to improve cash flow, margins, and operations. Get expert advice.

Ansh Malhotra

Revenue is up. Profit on paper looks acceptable. Yet you still check the bank balance before approving stock, wages, or a new hire.

That's where many Australian SME owners sit right now. The books are technically “done”, BAS is lodged, payroll runs, and the accountant sends reports after month-end. But decisions are still being made from a mix of instinct, old spreadsheets, and whatever cash happens to be available this week.

That gap is where accounting business advisory matters. It moves finance from rear-view reporting to operational decision support. Instead of asking only whether the accounts are compliant, you ask better questions: where is cash getting trapped, which process is wasting team time, what margin is usable, and what needs to change this month, not next year.

Table of Contents

Beyond the Books What Is Accounting Business Advisory

A common pattern shows up in both inventory businesses and service firms. The owner has reports, but not clarity. A retailer sees sales moving but can't tell which stock lines are starving cash. A trade business is booked out, but invoices go out late and debtor follow-up is inconsistent. A consulting firm is profitable, yet payroll and tax dates still create pressure because forecasting is rough and nobody trusts the numbers enough to make fast decisions.

That's the difference between accounting and advisory. Traditional accounting records what happened and keeps the business compliant. Advisory takes those numbers and turns them into actions around pricing, cash flow, stock, hiring, payment timing, and system design.

What changes when advisory starts

With advisory in place, the finance function stops acting like a filing cabinet and starts acting like an operating system. The conversation shifts from “your reports are ready” to “your receivables are slowing, stock is overbought in one category, and your margin is being diluted by delivery and rework”.

The wider market is moving in the same direction. The global accounting services market was valued at USD 646.06 billion in 2024 and is projected to reach USD 986.50 billion by 2032, growing at a 5.40% CAGR, according to Fortune Business Insights on the accounting services market. That matters because the growth isn't being driven by basic bookkeeping alone. It reflects a broader shift toward strategic finance support, cloud systems, and technology-enabled decision-making.

What advisory is not

It isn't a fancier tax meeting.

It isn't a quarterly strategy workshop with no follow-through.

It isn't a dashboard that looks polished but doesn't change how money moves through the business.

Practical rule: If the advice doesn't improve cash in the bank, reduce wasted time, strengthen decision-making, or lower operational friction, it's probably still reporting dressed up as advisory.

For owners comparing service models, it helps to look at providers that combine finance support with systems and operational execution. A useful example is Wisely accounting services, which shows how accounting support can sit inside a broader business process model rather than existing as a standalone compliance function.

In practice, accounting business advisory gives you a financial co-pilot. Someone who doesn't just tell you the score after the game, but helps call the plays while it's still being won or lost.

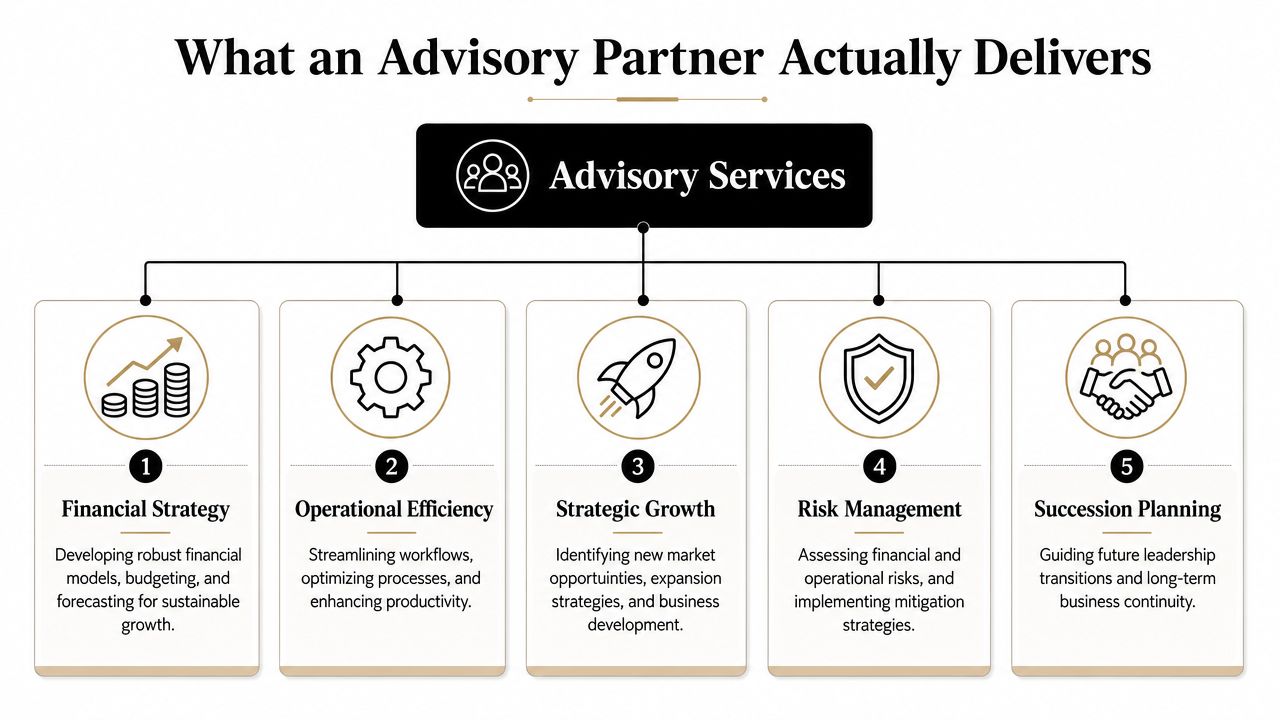

What an Advisory Partner Actually Delivers

A good advisory partner doesn't hand over a report and disappear. They build a finance rhythm around the business, then use that rhythm to improve decisions and remove friction.

The services offered by higher-growth CAS practices show what buyers value. In the CPA.com CAS Benchmark Survey, CFO/controller advisory services were offered by 92% of respondents, accounts payable by 90%, and forecasting/budgeting by 89%. That mix shows advisory is operational and forward-looking, not just compliance-focused, as noted in the CPA.com CAS Benchmark Survey summary.

The Virtual CFO function

The clearest way to think about a Virtual CFO is this: they translate finance into management action. They don't just prepare numbers. They decide which numbers matter, how often they should be reviewed, and what decisions they need to trigger.

For an inventory business, that often means:

Forecasting cash pressure: Mapping supplier payments, GST, wages, debt servicing, and stock purchases against expected receipts.

Protecting gross margin: Identifying where discounting, freight, write-offs, or purchasing decisions are eroding usable profit.

Improving decision speed: Replacing “I think we can afford it” with a forecast-backed view of timing and risk.

If you want a deeper view of that role, Nexist has a practical explainer on the Virtual Chief Financial Officer model.

Cash flow, stock, and process control

At this point, advisory becomes tangible.

A retailer or wholesaler usually doesn't need more year-end commentary. They need someone to ask why purchase orders are being raised before old stock clears, why credit terms aren't being enforced, and why supplier bills still sit in inboxes waiting for approval. A service business has a different version of the same problem. Work gets delivered, invoicing lags, timesheets are incomplete, and margin disappears into delays and admin.

A capable advisor will usually deliver a mix of the following:

Deliverable | What it does in practice |

|---|---|

Cash flow forecast | Shows upcoming pressure points before they become emergencies |

Margin review | Separates revenue growth from actual profit retention |

KPI pack | Tracks the few numbers that drive decisions, not a long vanity dashboard |

AP workflow | Tightens supplier approvals and payment timing |

AR process | Gets invoices out faster and follow-up happening consistently |

Inventory review | Highlights excess, ageing, and mismatched purchasing patterns |

The best advisory work often looks ordinary from the outside. Cleaner invoicing. Fewer spreadsheet workarounds. Better stock discipline. Faster close. That's usually where the money is.

Implementation matters more than theory

Many owners have already received advice at some point. The problem is that nobody changed the workflow. The chart of accounts stayed messy. Approval rules stayed informal. Forecasts were built once, then ignored. The “advisory” ended as a conversation, not an operating change.

That's why hands-on implementation matters. The deliverable isn't only insight. It's a rebuilt process that the team can run every week without relying on the owner to chase everything manually.

Proving the ROI of Strategic Advisory

The strongest case for advisory isn't a prettier management pack. It's a business that starts converting effort into cash and time more reliably.

A lot of founders are overloaded with strategy language while the actual leak sits in stock, receivables, or billing discipline. That's why practical working-capital intervention matters so much. As Thomson Reuters notes in its discussion of accounting firms becoming business advisors, many founders don't need another strategic narrative. They need applied help fixing cash trapped in stock and receivables.

Example one an inventory business with cash trapped on the shelf

Take an ecommerce or wholesale business with healthy top-line movement but constant cash stress. The owner sees sales every day, yet supplier payments feel tighter each month. On review, the pattern is often obvious. Too many SKUs. Slow movers mixed with good sellers. Reordering driven by instinct rather than turnover. Promotions used to clear stock after the cash is already tied up.

The ROI from advisory in that situation usually comes from a few specific moves:

Rationalising stock decisions: Separating core lines from dead or slow-moving stock.

Changing purchasing rhythm: Buying to forecast and lead times, not to supplier pressure or habit.

Tightening reporting: Reviewing stock ageing, gross margin by line, and reorder logic on a recurring basis.

Fixing process ownership: Making one person accountable for stock actions rather than leaving it spread across sales, ops, and the owner.

The measurable outcome isn't just “better inventory management”. It's cash released from overstocking, fewer rushed funding decisions, and less margin erosion from clearance behaviour.

Example two a service or trade business with hidden admin drag

Now take a freight operator, agency, or trade business. Revenue may look fine, but invoicing gets delayed because job data comes in late, approvals happen informally, and the finance person spends too much time cleaning records before month-end. Nobody notices the cost because it sits inside admin hours, debtor delays, and owner follow-up.

Advisory often produces a different kind of ROI:

Before advisory | After operational advisory |

|---|---|

Invoices depend on manual handoffs | Invoicing follows a defined workflow |

Debtor follow-up is ad hoc | Collection responsibility and cadence are clear |

Payroll, supplier bills, and jobs sit in separate systems | Core data flow is aligned |

The owner checks cash reactively | Cash decisions are tied to a rolling forecast |

That outcome matters because hours saved aren't abstract. They come from fewer approval bottlenecks, less rework, less chasing, and cleaner month-end close.

If an owner still has to personally unblock billing, supplier approvals, and basic cash decisions every week, the finance system isn't doing its job yet.

What good ROI measurement looks like

For SMEs, ROI should be tracked in terms the owner actually feels:

Cash released: Less money stuck in slow stock, late invoices, or poorly timed payments.

Hours saved: Less manual coding, less approval chasing, fewer spreadsheet reconciliations.

Decision quality: Faster calls on hiring, pricing, purchasing, and funding because the numbers can be trusted.

Operational stability: Fewer surprises around payroll, tax, supplier pressure, and seasonal swings.

Strategic advisory earns its place when it changes those realities. If it only produces commentary, the return will always feel vague.

For businesses that need the planning side formalised, the strategic and financial planning approach is often the bridge between broad ambition and practical execution.

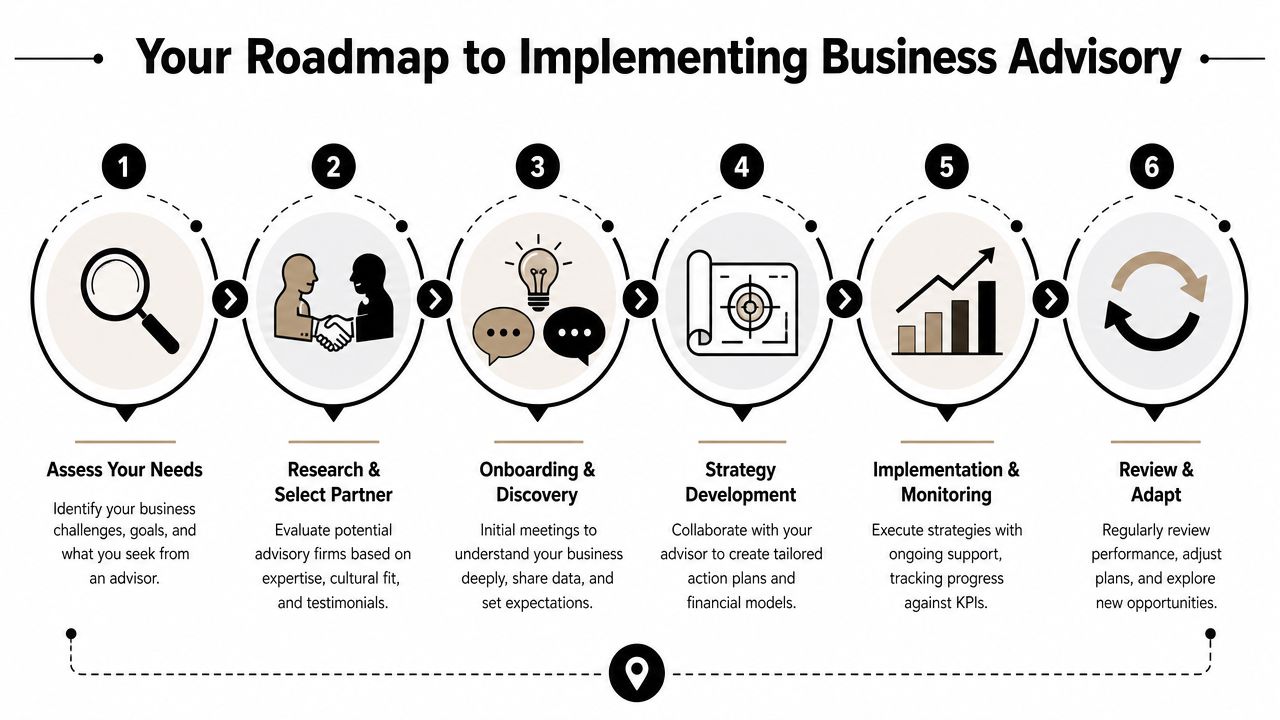

Your Roadmap to Implementing Business Advisory

The shift into advisory works best when it's treated as an operating project, not a one-off conversation. The first goal is to find the leaks. The second is to prioritise them. The third is to make sure the fix sticks in daily workflow.

A useful way to visualise the process is below.

Start with diagnosis

Before changing software, headcount, or reporting packs, the business needs a clean view of where cash and time are leaking. In practice, that means reviewing reconciliations, billing flow, approval steps, stock controls, and the quality of current reporting.

The most useful lens here is working capital. Industry guidance for advisory practices treats debtor days, creditor days, inventory turns, and the cash conversion cycle as core metrics because one weak area can distort cash availability across the whole business. The Calxa guidance on accounting advisory services makes the point well. Regular health checks on these KPIs help management act before liquidity problems become hard to reverse.

A diagnostic phase should answer questions like:

Where is cash sitting too long: Receivables, inventory, prepayments, or poorly timed supplier outflows?

Which process is slowing finance: Job completion to invoice, purchase approval, payroll inputs, or bank reconciliation?

What does the owner still carry personally: Cash decisions, reporting cleanup, collections, or stock calls?

Build the operating model

Once the leaks are clear, the next step is to build a finance model the business can run. That usually includes a rolling forecast, a small KPI set, role clarity, and recurring review points.

A simple operating model tends to work better than a complex one. Most SMEs do not need dozens of measures. They need a short scoreboard tied to actions:

Focus area | Weekly or monthly question |

|---|---|

Receivables | Are invoices out, and are collections moving? |

Payables | What must be paid now, and what can be scheduled intelligently? |

Inventory | What is turning, what is ageing, and what should not be reordered? |

Margin | Which jobs, channels, or products are underperforming? |

Capacity | Is the team spending time on work that should be automated or standardised? |

Execute the fixes

Weak implementation is a common reason many advisory projects fail. The analysis is fine, but execution is weak.

The business usually needs practical changes such as invoice triggers, approval thresholds, payment runs, SKU governance, payroll checklists, SOPs, and clearer handoffs between operations and finance. For one business, that might mean redesigning how supplier bills are approved. For another, it means linking completed jobs to invoicing so revenue doesn't sit unbilled.

A short walkthrough can help owners see what a more structured finance function looks like in practice:

Field note: A forecast only works when someone trusts it enough to act on it. That trust comes from cleaner inputs and recurring review, not from making the spreadsheet more complicated.

Review and adjust

Advisory shouldn't create a static annual plan. It should create a management rhythm. Monthly and quarterly reviews are where assumptions get tested, bottlenecks surface, and actions are reset before issues become expensive.

That's also where a firm like Nexist can fit. It combines virtual CFO support with operational execution around cash flow, inventory, AP, AR, payroll, SOPs, and automation, which is the kind of integrated model many SMEs need when finance issues are tied directly to process friction.

How Technology and AI Supercharge Advisory

Technology only helps when it removes friction from real workflows. If a business adds apps without redesigning the process underneath, it usually ends up with more systems, more logins, and the same bottlenecks.

The practical use of AI in advisory is narrower and more valuable than the hype suggests. It works best in repetitive finance tasks where speed and consistency matter. Think invoice coding, reconciliations, document extraction, reporting prep, and workflow routing. Human judgment still matters for exceptions, margin interpretation, stock decisions, pricing changes, and capital allocation.

That gap between interest and delivery is real. Buyer interest in data analytics and technology services is rising, yet only about 14% of firms in the CPA.com survey offer them, as discussed in this analysis of the gap between tradition and innovation for tax advisory. For Australian SMEs, that creates an opening to work with advisors who can redesign both the finance process and the supporting technology.

Where automation usually pays off

The strongest use cases tend to be specific:

Accounts payable automation: Supplier bills are captured, coded, routed, and approved with less manual handling.

Bank reconciliation support: Routine matching is accelerated so finance staff spend more time reviewing exceptions.

Reporting workflows: Data is pulled into recurring management packs faster and with fewer spreadsheet breaks.

Payroll and compliance prep: Inputs are standardised so the cycle is less dependent on memory and last-minute chasing.

For businesses exploring this area, Nexist's article on accounts payable automation in Australia is a practical starting point because AP is often one of the fastest places to remove admin load.

The ROI test for AI in finance

Don't ask whether a tool is “smart”. Ask whether it reduces admin, shortens close cycles, improves data quality, or gives management cleaner timing signals.

A smaller operator can even learn from adjacent examples outside the SME finance space. This guide to automating finances for freelancers is useful because it shows the same principle in a leaner setting. Remove repetitive finance tasks first, then use the reclaimed time for judgment, planning, and client or customer work.

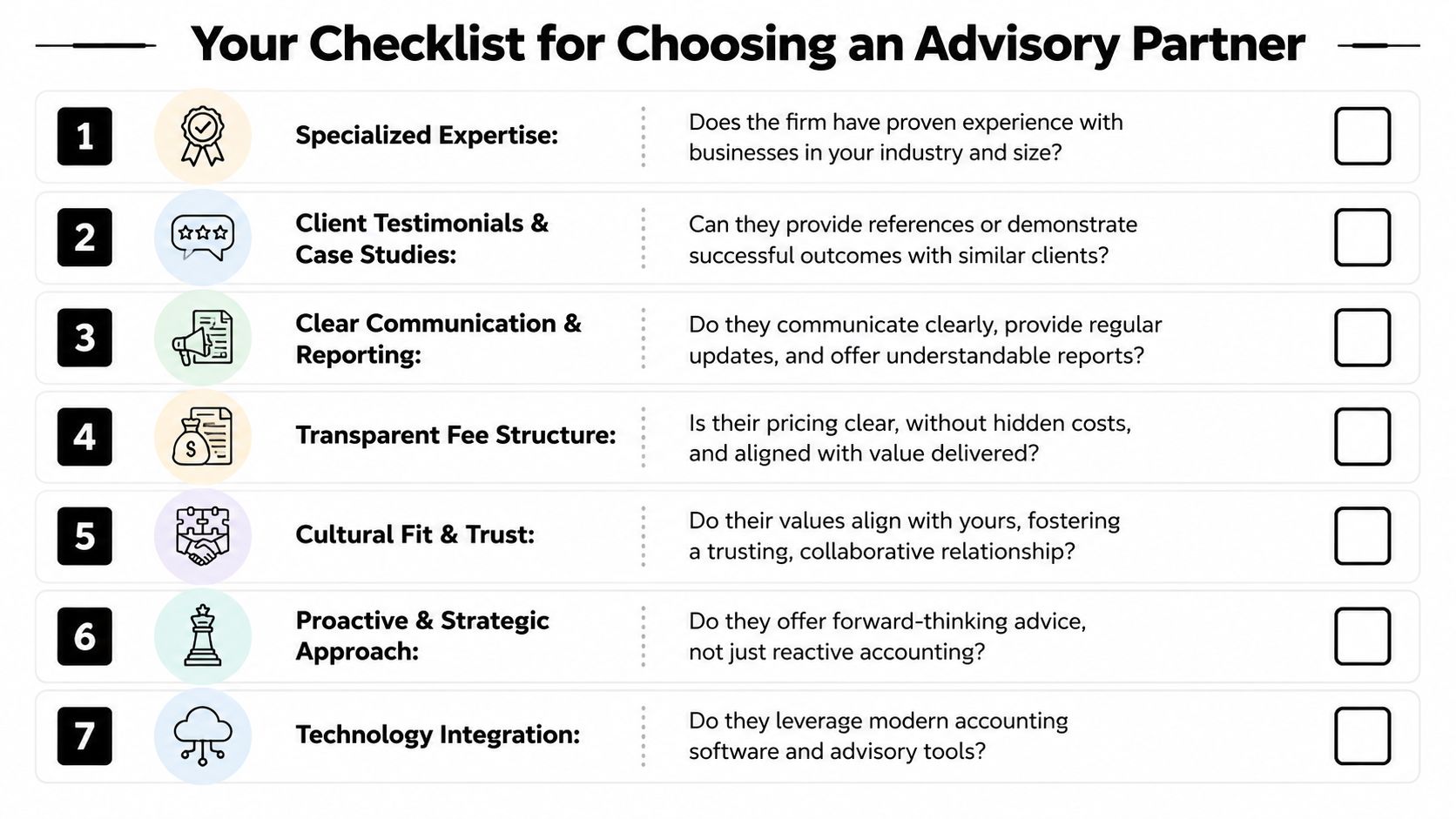

Your Checklist for Choosing an Advisory Partner

A business doesn't need another provider who can talk fluently about growth but leaves all the implementation with the owner. The right advisory partner should be able to diagnose issues, prioritise them, and help put the fix into the workflow.

Questions that separate real advisory from dressed-up compliance

Use these in a first meeting and pay attention to how concrete the answers are.

How will you improve cash conversion, not just reporting? A strong advisor should talk about receivables, payables, inventory, billing flow, approval timing, and forecast discipline.

What do you implement directly? If the answer is limited to meetings and recommendations, you'll probably carry the main workload yourself.

How do you handle inventory-heavy businesses? Retail, ecommerce, wholesale, hospitality, and manufacturing all need someone who understands stock, supplier cadence, and working capital.

What does your KPI pack truly contain? You want a focused scorecard tied to actions, not pages of low-value metrics.

How do you use automation and AI? Good answers are specific. AP workflows, reconciliation support, reporting cadence, payroll controls, and SOPs. Not buzzwords.

Who will I deal with each month? Advisory works when communication is direct and regular, not filtered through layers.

How do you measure success? Look for answers tied to released cash, cleaner close, fewer bottlenecks, and better decision-making.

Red flags worth taking seriously

Some warning signs show up quickly.

Red flag | What it usually means |

|---|---|

Everything starts and ends with tax | The firm is still compliance-led |

Advice is broad but not operational | You'll get ideas, not execution |

No clear process for forecasting | Cash surprises will keep happening |

No view on stock, debtors, or payables | Working-capital issues will stay hidden |

Reporting is heavy but decision-making is light | The output looks polished but won't change much |

A capable advisor should be able to tell you, in plain language, where they expect to find cash leaks within your business model.

The standard to hold them to

Choose someone who can work at the level your business struggles. That may be pricing, stock turns, approvals, payroll flow, debtor discipline, or management reporting.

If they can't connect finance to operations, they're not really delivering accounting business advisory. They're still describing the business after the fact.

From Watchman to Visionary The Final Step

Most owners don't start a business because they want to chase overdue invoices, approve every bill by hand, or stare at stock reports trying to guess what to reorder. They want control, visibility, and enough confidence in the numbers to make decisions without constant cash anxiety.

That's what strategic advisory changes. It takes finance out of the compliance corner and turns it into a management tool. For inventory businesses, that often means releasing cash trapped in stock and tightening purchasing discipline. For service businesses, it usually means fixing billing flow, reducing admin drag, and creating forecasts that can be trusted.

The shift is personal as much as financial. You move from watchman to visionary. Less firefighting. More deliberate decisions. Better use of your time and a business that isn't held together by memory, spreadsheets, and owner effort.

If you want a practical starting point, Nexist offers a Business Scorecard that helps founders identify where cash is leaking through stock, receivables, margins, and process friction. It's a straightforward way to see whether your finance function is only keeping score or helping you grow.

accounting business advisory, virtual cfo australia, sme business advice, cash flow management, business growth strategy

" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="dSFdkJotL" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="wscNJE44G" transform="translate(0 0.129)" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="sTpjGo1tb" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="s7ffpmKOD" transform="translate(0 0.129)" width="24px"/><g d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.000006px" id="D0ecaHEcW" transform="translate(0 0)" width="24px"><path d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z" fill="rgb(55, 184, 218)" height="24.000006px" id="IPLFE6zXx" width="24px"/><path d="M 4.02 0 L 0 0 L 0 12.092 L 4.02 12.092 Z" fill="rgb(255, 255, 255)" height="12.09201px" id="FWhtzAyuY" transform="translate(2.863 8.375)" width="4.02px"/><path d="M 2.274 0 C 0.899 0 0 0.904 0 2.089 C 0 3.25 0.871 4.179 2.221 4.179 L 2.247 4.179 C 3.648 4.179 4.521 3.25 4.521 2.089 C 4.495 0.904 3.649 0 2.274 0 Z" fill="rgb(255, 255, 255)" height="4.17876px" id="VmOsKv4kO" transform="translate(2.625 2.545)" width="4.52095px"/><path d="M 7.641 0 C 5.509 0 4.554 1.173 4.019 1.996 L 4.019 0.284 L 0 0.284 C 0.053 1.419 0 12.376 0 12.376 L 4.019 12.376 L 4.019 5.623 C 4.019 5.262 4.045 4.9 4.151 4.642 C 4.442 3.92 5.103 3.172 6.214 3.172 C 7.667 3.172 8.25 4.282 8.25 5.907 L 8.25 12.376 L 12.269 12.376 L 12.269 5.442 C 12.269 1.728 10.286 0 7.641 0 Z" fill="rgb(255, 255, 255)" height="12.37626px" id="n1XUbhaq0" transform="translate(9.105 8.09)" width="12.268830000000001px"/></g></g></g></g></svg>)