Accounts Receivable Aging Report: A Founder's Guide 2026

Unlock cash flow with our guide to the accounts receivable aging report. Learn to create, interpret, and use it to improve collections for your Australian SME.

Ansh Malhotra

Your profit and loss says the business is making money. Your bank account says otherwise. Payroll is coming up, BAS is around the corner, and you're chasing customers who keep saying the payment is “in the next run”.

That gap is where a lot of Australian founders get stuck. Sales have happened. Invoices are out. Revenue is booked. But the cash is still sitting in someone else's accounts payable queue.

The document that exposes this problem fastest is the accounts receivable aging report. Not because it's glamorous. It isn't. But it shows exactly which invoices are current, which are drifting, and which customers are turning your business into their lender.

If your overdue debt is starting to shape hiring decisions, supplier payments, or founder stress levels, this is the report to watch. It also sits alongside broader cash planning. If you're tightening finance operations more broadly, this guide to strategic and financial planning is useful context, and some founders also look at a broader financial BPO strategy for SMEs when internal follow-up is inconsistent.

Table of Contents

Why Your Profit Is Not Showing Up as Cash

A founder can look profitable on paper and still feel broke in real life.

It usually starts the same way. Sales improve, the P&L looks respectable, and the business should be breathing easier. Instead, cash stays tight. Wages need covering. Stock needs buying. Tax obligations don't wait. The owner starts asking the wrong question, which is “why aren't we profitable?” The harder question is usually “who owes us, and how old is that debt?”

The hidden leak is often receivables

When I review SME cash flow problems, I rarely start with the revenue line. I start with unpaid invoices.

A business can book revenue today and still wait weeks or months to collect it. During that gap, the company is funding labour, materials, rent, and tax from its own cash. If enough invoices slip past due, a profitable month turns into a cash squeeze.

Practical rule: If you're relying on next week's debtor receipts to meet core obligations, your receivables process is already a cash-flow issue, not just an admin issue.

The accounts receivable aging report shows where the blockage sits. It tells you which customers are paying inside terms, which accounts always drift, and which invoices have crossed from normal delay into active collections risk. That's the point where finance stops being bookkeeping and becomes operational control.

Why founders miss it

Founders usually see overdue debt customer by customer. They know one client is slow. They know another always has a query. What they don't see is the pattern across the full ledger.

That pattern matters more than any single invoice. If late payments cluster around one customer segment, one service line, or one invoicing habit, the issue isn't collections discipline alone. The business model is carrying too much customer financing.

Aging reports are useful because they turn vague frustration into a visible queue. Once the debt is grouped by age, it becomes obvious where cash is stuck and what needs action first.

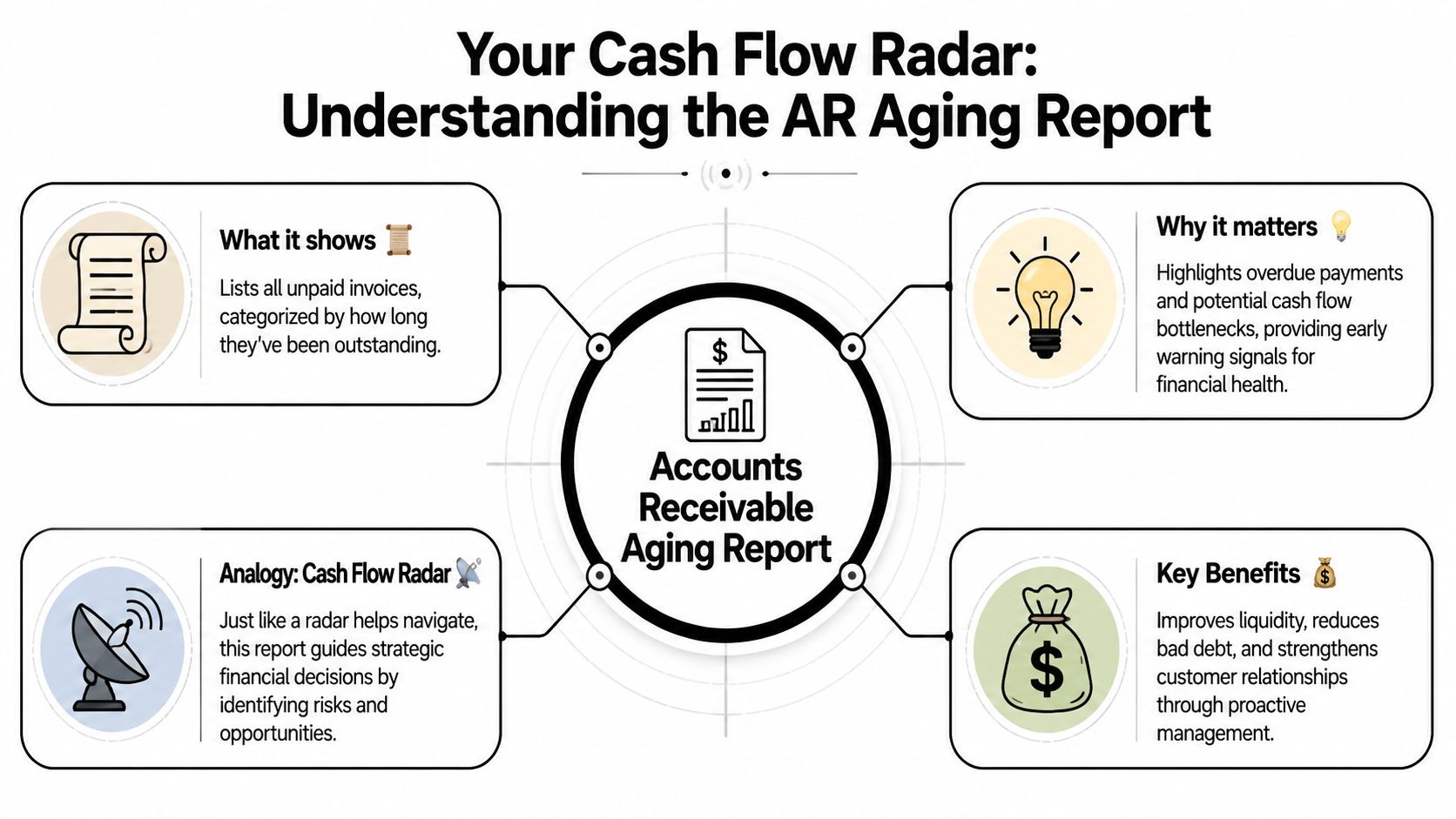

What Is an Accounts Receivable Aging Report

An accounts receivable aging report is a list of open customer invoices organised by how long each balance has been outstanding.

Think of it as your cash flow radar. It doesn't just show that money is owed. It shows how old that money is, which customers are becoming risky, and where follow-up should happen first.

What the report actually tells you

A standard aging report answers three basic questions:

Who owes you money

How long the balance has been outstanding

How much is sitting in each time band

That's why it's more useful than a simple debtor list. A debtor list can tell you total outstanding receivables. An aging report tells you whether those receivables are healthy, drifting, or becoming doubtful.

If most balances are current, collections are usually under control. If old balances are piling up, cash is being trapped outside the business.

Why it matters in Australia

This report also matters for governance, not just collections.

Australian record-keeping standards put weight on accurate financial records, and receivables visibility has become more important since the Treasury Laws Amendment (Combating Illegal Phoenixing) Act 2019 strengthened rules around improper manipulation of company records, with the reform commencing in 2020, as outlined in Stripe's guide to what an aging report is and how to use it. If invoice dates, terms, or balances are distorted, the aging report stops being reliable, and cash planning goes off course with it.

Good AR control starts with clean invoice dates, clean due dates, and one version of the truth in your ledger.

What it is not

It isn't just a month-end report for the accountant. It's not a static spreadsheet you glance at when cash gets uncomfortable.

Used properly, it's an operating document. Sales can use it before approving more credit. Finance can use it to prioritise follow-up. Founders can use it to decide whether a customer stays on terms, moves to deposits, or gets paused until old balances are cleared.

Understanding the Components and Aging Buckets

A useful aging report is built from open customer invoices, not guesses, not reminder notes, and not a rough list exported from email. Each line should tie back to an actual invoice that's still unpaid.

According to Indiana University's guide to the accounts receivable aging and detail report, a robust report should be segmented into current, 1–30 days, 31–60 days, 61–90 days, and 90+ days, with each item linked to invoice date, due date, customer, and outstanding amount so it can be reconciled to the general ledger.

The core fields that matter

Every founder should know what each column is doing.

Component | Why it matters |

|---|---|

Customer name | Shows who is carrying the balance and where exposure is concentrated |

Invoice number | Lets your team trace disputes, part-payments, and follow-up history |

Invoice date | Shows when the receivable started and supports reconciliation |

Due date | Determines whether the balance is current or overdue |

Outstanding amount | Shows what is still collectible, not just the original invoice value |

If one of these fields is wrong, the whole report gets weaker. A missing due date can place an invoice in the wrong bucket. A duplicate invoice number can confuse collections. An outdated balance can make a customer look slower than they are.

How the aging buckets work

The buckets create a risk ladder. They help your team separate routine debt from debt that needs escalation.

Current

These invoices aren't overdue yet. They still matter because they indicate expected cash coming in under normal terms.1–30 days

This is often the first warning zone. Some invoices here are overlooked in a customer payment run. Some are the start of a pattern.31–60 days

This bucket usually needs active follow-up. By now, you're no longer dealing with a simple timing issue on every account.61–90 days

Risk is rising. The customer may have process issues, dispute issues, or cash issues. Credit decisions should start changing here.90+ days

At this stage, old debt starts consuming disproportionate management time. Recovery becomes harder, and every new sale to that customer needs scrutiny.

Older debt doesn't just reduce collection confidence. It also distorts your view of future cash receipts.

What founders should look at first

Don't start by reading line by line. Start with concentration.

Look at which bucket holds the most value. Then check whether old balances are spread across many customers or stacked on a few. A few concentrated problem accounts call for targeted action. Broad deterioration usually points to a process problem in billing, collections, or credit terms.

How to Create and Maintain Your Aging Report

Most Australian SMEs can generate an aging report directly from accounting software. If you use Xero, MYOB, or QuickBooks, the report already exists. The hard part isn't producing it. The hard part is making sure the underlying data is clean enough to trust.

That matters because your aging report starts with invoicing discipline. Under the ATO's GST rules, businesses generally must issue a tax invoice within 28 days if a buyer requests one for a taxable sale of more than $82.50 including GST, and those tax invoices are essential records for GST reporting, as noted in Maxio's explanation of the aging report and invoice timing context. If your invoice dates are sloppy, your aging logic is sloppy too.

Pulling the report from software

In Xero or MYOB, the usual path is straightforward. Go to receivables or sales reports, find the aging or receivables summary, and set the report date.

Use the report date carefully. Aging is always relative to a point in time. If you run it mid-month and again at month-end, you may see very different risk positions.

A simple operating routine looks like this:

Run the report for all open invoices

Don't filter out inconvenient accounts. You want the full picture.Check overdue groupings

Make sure invoices are falling into the right time buckets.Reconcile to the ledger

The total receivables balance in the report should agree with your accounting records.Review exceptions before sharing

Remove invoices that are clearly duplicated, already paid but not allocated, or under formal credit note review.

If you're still using a spreadsheet

A spreadsheet can work if invoice volume is modest and one person owns the file. It breaks down when multiple people update it casually.

Use a clean structure with one row per invoice:

Sample Accounts Receivable Aging Report

Customer Name | Invoice # | Due Date | Total Due | Current | 1-30 Days | 31-60 Days | 61-90 Days | 90+ Days |

|---|---|---|---|---|---|---|---|---|

Customer A | INV-001 | |||||||

Customer B | INV-002 | |||||||

Customer C | INV-003 |

The spreadsheet only works if your team updates payments promptly. Otherwise, you'll chase customers who have already paid and miss customers whose accounts have aged into older buckets.

Data hygiene is where most reports fail

Aging reports become unreliable for predictable reasons:

Wrong invoice dates because invoices were raised late or back-entered

Wrong payment terms because the customer master file was never updated

Unallocated receipts because cash was received but not matched

Open disputes hidden in notes instead of flagged in the system

Operational habit: Refresh the aging report at least monthly. If your invoice volume is high, review it more often so it becomes a live collections list instead of a historical document.

Interpreting the Report for Cash Flow and Credit Decisions

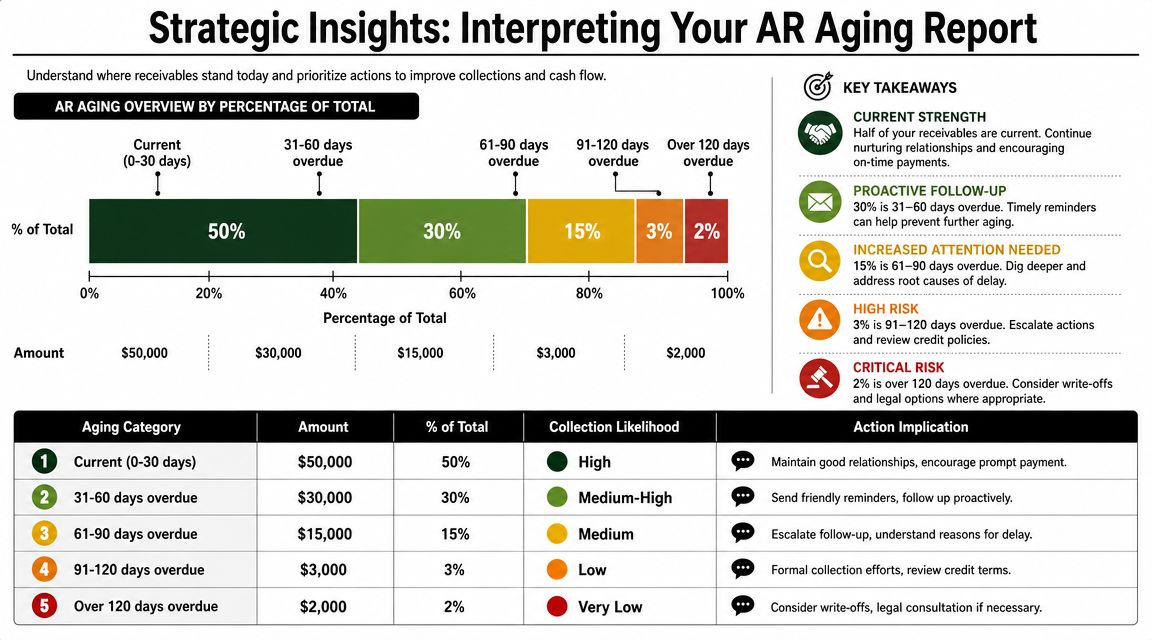

The true value of an accounts receivable aging report isn't the total at the bottom. It's the shape of the debt.

NetSuite's overview of accounts receivable aging makes the key point well. Aging works best as a collections risk map. The older the bucket, the lower the expected collectability and the higher the bad-debt risk. That's why smart finance teams focus on distribution across time bands, not just total receivables.

What a healthy report usually looks like

A healthy report is weighted toward the newest buckets. You expect some routine movement in current and early overdue balances. That's normal in most trading businesses.

An unhealthy report shows balances creeping further right. When invoices start settling in 61–90 days or 90+ days, the business is carrying more risk, and cash forecasting becomes less dependable.

Here's how to read common patterns:

Most balances are current

Terms are broadly working. Follow-up can stay light and systematic.A lot sits in 1–30 days

This can mean customers pay late as a habit, or your reminder cadence starts too late.Balances cluster in 31–60 days

Something is slowing conversion. Look at disputes, approval delays, or weak follow-up.Debt is piling up in 61–90 and beyond

Credit policy should tighten. Collections should escalate. New work on terms needs review.

Use the report to make decisions, not observations

Aging should change behaviour inside the business.

If a customer appears in older buckets repeatedly, don't just chase the latest invoice. Change the trading settings. Move them to deposits, staged billing, reduced credit exposure, or stop-credit until arrears are cleared.

If the issue affects many customers, don't blame individual clients first. Review whether your invoice terms, billing timing, or sales handover process is creating delay.

This video gives a useful visual overview of how teams read these reports in practice.

Questions worth asking every month

Instead of asking “who is overdue?”, ask:

Which customers move into old buckets again and again

Which invoice types age the slowest

Which staff or systems own disputed invoices

Whether new sales are increasing risk faster than collections are reducing it

If older buckets are growing, your future cash receipts are less certain than your P&L suggests.

Advanced Collection Strategies Based on Aging Data

Most AR advice stops at “call overdue customers”. That's too blunt. It treats all late debt the same, and it ignores the bigger problem. In many SMEs, late payment isn't just customer behaviour. It's a design flaw in how the business invoices, approves credit, and follows up.

Allianz Trade's discussion of accounts receivable aging points to an important gap in Australian guidance. Founders often need help fixing systemic payment delay, not just chasing one late invoice after another. That's where the aging curve becomes useful. It shows whether your business is funding customers too generously.

Match the collection method to the bucket

Different debt ages need different treatment.

For newer overdue invoices, keep the tone light and procedural. For older debt, tighten the tone, tighten the cadence, and tighten the trading terms.

A practical bucket-based approach looks like this:

1–30 days overdue

Use polite reminders, confirm receipt of the invoice, and make payment friction low. A simple payment link or short phone check often resolves more than a stern email at this stage.31–60 days overdue

Shift from reminder to action. Call the accounts payable contact. Confirm whether there's a dispute, missing purchase order, or approval bottleneck. Get a promised payment date in writing.61–90 days overdue

Escalate to the decision-maker. Pause further credit where appropriate. Sales should know the account is now a finance risk, not just a relationship issue.90+ days

Stop casual follow-up. Use formal collection steps, settlement discussions, or external support if the account is still trading and unresponsive.

Look for the root cause behind the debt

Founders often discover the same patterns:

Service businesses invoice too late because staff don't submit timesheets or completion notes promptly.

Trade and project businesses use broad monthly billing when milestone billing would bring cash in earlier.

Wholesale operators keep extending terms to protect volume, then wonder why working capital stays tight.

Hospitality and seasonal businesses accept customer settlement cycles that don't match their own cost base.

That's why aging data belongs in operations meetings, not just finance reviews. If one job type or customer segment ages badly every month, change the commercial model.

Use automation where it helps, not where it annoys

For early-stage follow-up, automated reminders work well if they're timed properly and written clearly. Some teams also automate text message reminders alongside email for customers who respond faster to mobile prompts.

If you're strengthening the underlying process, this guide to accounts receivable management is a useful companion because the fix usually spans invoicing, approvals, follow-up cadence, and credit control.

The best collections strategy doesn't start when an invoice is overdue. It starts when you decide the terms, trigger the invoice, and set the follow-up rules.

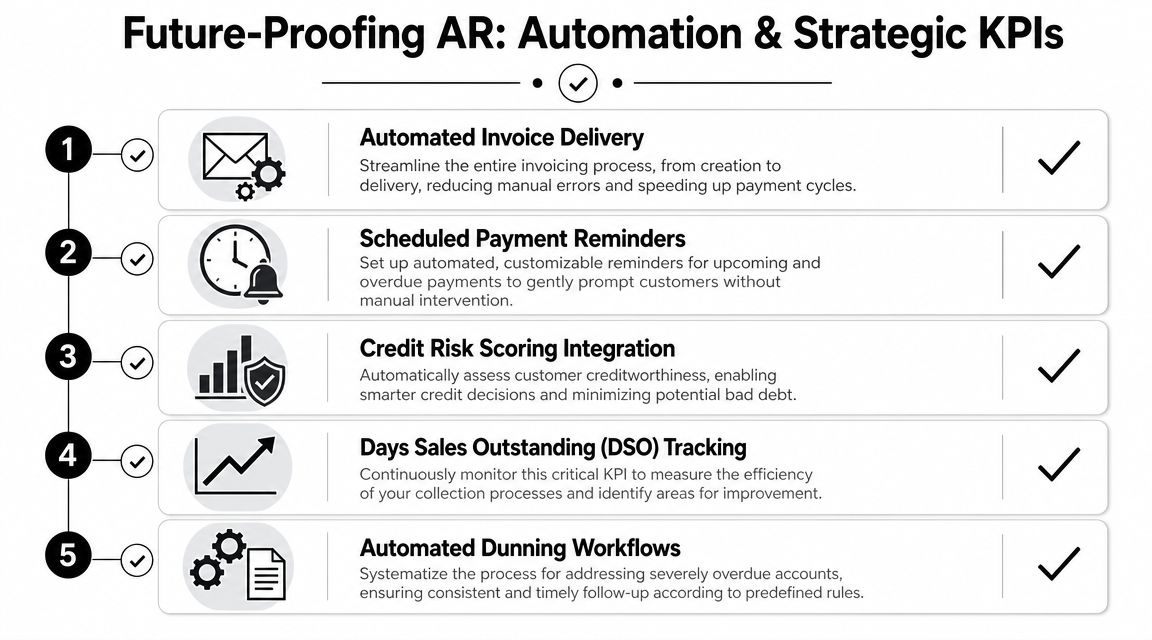

Automation SOPs and KPIs for Modern AR Management

Most businesses still treat the aging report like a static spreadsheet produced at month-end. That's outdated.

HighRadius' discussion of the accounts receivable aging report highlights the shift that matters now. As Australia's eInvoicing environment expands, the key opportunity is moving from basic categorisation to exception management. That means watching not just the aging bucket, but also whether the invoice was delivered, whether it hit a dispute, and whether reminders are converting into payments.

Build a simple AR operating rhythm

A solid AR SOP doesn't need to be complicated. It needs ownership and consistency.

Use a routine like this:

Issue invoices promptly

Don't let completed work sit unbilled.Confirm delivery status

Know whether the customer received the invoice.Schedule reminder points

Trigger messages before due date, on due date, and after due date according to risk.Flag exceptions fast

Mark disputes, missing purchase order references, and short-paid invoices clearly.Escalate by rule

Don't leave escalation to memory or founder instinct.

The KPIs that matter

The aging report is one input, not the whole dashboard. Track it alongside operational measures such as:

Days Sales Outstanding DSO

Useful for seeing how efficiently receivables convert into cash over time.Collection Effectiveness Index CEI

Useful for judging how well the team collects what became due.Dispute volume

Helps expose billing quality and handover problems.Invoice delivery confirmation

Important in automated and eInvoicing environments where “we didn't get it” should be verifiable.Auto-reminder conversion rates

Shows whether your reminder sequence is reducing manual chasing or just adding noise.

The key is not to overload the team. Pick a small set, review them consistently, and connect them to actions.

Automation still needs human oversight

Automation can send reminders, assign tasks, and route exceptions. It can't decide on commercial trade-offs by itself.

That's why finance leaders need process ownership. If you're designing workflows that combine people, software, and AI tools, even adjacent topics like managing AI employees become relevant because the challenge is no longer just software setup. It's making automated work reliable, supervised, and accountable.

For founders who want stronger cash control without building a full internal finance function, a virtual chief financial officer model often makes sense because AR only improves when collections, reporting, forecasting, and decision rules work together.

If your business is profitable but cash still feels trapped, Nexist helps Australian founders turn reports into action. From receivables clean-up and cash-flow forecasting to SOPs, KPIs, and finance automation, the team builds the systems that get overdue cash moving again. Learn more at Nexist.

accounts receivable aging report, cash flow management, sme finance australia, invoice collections, virtual cfo

" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="dSFdkJotL" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="wscNJE44G" transform="translate(0 0.129)" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="sTpjGo1tb" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="s7ffpmKOD" transform="translate(0 0.129)" width="24px"/><g d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.000006px" id="D0ecaHEcW" transform="translate(0 0)" width="24px"><path d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z" fill="rgb(55, 184, 218)" height="24.000006px" id="IPLFE6zXx" width="24px"/><path d="M 4.02 0 L 0 0 L 0 12.092 L 4.02 12.092 Z" fill="rgb(255, 255, 255)" height="12.09201px" id="FWhtzAyuY" transform="translate(2.863 8.375)" width="4.02px"/><path d="M 2.274 0 C 0.899 0 0 0.904 0 2.089 C 0 3.25 0.871 4.179 2.221 4.179 L 2.247 4.179 C 3.648 4.179 4.521 3.25 4.521 2.089 C 4.495 0.904 3.649 0 2.274 0 Z" fill="rgb(255, 255, 255)" height="4.17876px" id="VmOsKv4kO" transform="translate(2.625 2.545)" width="4.52095px"/><path d="M 7.641 0 C 5.509 0 4.554 1.173 4.019 1.996 L 4.019 0.284 L 0 0.284 C 0.053 1.419 0 12.376 0 12.376 L 4.019 12.376 L 4.019 5.623 C 4.019 5.262 4.045 4.9 4.151 4.642 C 4.442 3.92 5.103 3.172 6.214 3.172 C 7.667 3.172 8.25 4.282 8.25 5.907 L 8.25 12.376 L 12.269 12.376 L 12.269 5.442 C 12.269 1.728 10.286 0 7.641 0 Z" fill="rgb(255, 255, 255)" height="12.37626px" id="n1XUbhaq0" transform="translate(9.105 8.09)" width="12.268830000000001px"/></g></g></g></g></svg>)