Virtual Chief Financial Officer A Founder's Guide

What is a virtual chief financial officer and do you need one? This 2026 guide explains the services, costs, ROI, and Australian-specific benefits for SMEs.

Ansh Malhotra

Revenue is up. The sales dashboard looks healthy. Your accountant says the P&L is profitable. Then payroll lands, a BAS payment is due, a supplier wants to be paid, and you're moving money around trying to keep everything upright.

That's where a lot of founders get stuck. On paper, the business is growing. In the bank, it feels tight. In your head, finance becomes a constant background hum. You're not just running the business anymore. You're watching every invoice, every stock order, every wage run, every tax deadline.

A virtual chief financial officer sits in that gap between “the numbers are done” and “the business is under control”. For Australian SMEs, that matters because the problem usually isn't a lack of effort. It's that cash, margins and compliance all interact, and they rarely break in obvious places.

Table of Contents

The Founder's Dilemma Profit on Paper No Cash in the Bank

A founder in retail knows this feeling well. Sales have had a strong month, stock has been moving, and the team's flat out. But the cash account doesn't reflect the effort because money is sitting in unsold inventory, in unpaid invoices, or in upcoming liabilities that haven't hit yet.

That tension is common in Australia because the business environment is dominated by smaller operators. In June 2024, Australia had about 2.59 million actively trading businesses, and 98% were small businesses with fewer than 20 employees, according to this Australian virtual CFO market overview. Most of those businesses need financial judgement, but not a full-time CFO salary.

Why founders feel trapped in the numbers

When this happens, the owner becomes the watchman. You check the bank before making routine decisions. You delay hiring because you don't trust the cash position. You approve every supplier payment yourself because no one has given you a clear forecast you believe.

That's usually not an accounting problem. It's a finance operating problem.

A bookkeeper can keep records clean. A tax accountant can lodge what needs lodging. But neither role is automatically responsible for helping you decide whether you can afford to buy more stock, extend payment terms to a customer, or carry an extra apprentice through a slow month.

Profit doesn't pay wages. Cash does.

The gap between tidy books and business control

Founders often discover the issue in basic areas first. Expense coding is inconsistent, gross margin is blurred, and overheads get buried in broad categories. If that sounds familiar, a solid resource like this founder's guide to expense classification helps clean up the inputs before you try to make bigger decisions from them.

A virtual chief financial officer works above compliance and below strategy theatre. The role is practical. Build a forecast. Pressure-test assumptions. See where cash is getting trapped. Set a reporting rhythm. Turn the numbers into actions the business can execute.

What a Virtual Chief Financial Officer Really Does

A lot of business owners hear the phrase and think it means “accountant, but more expensive”. That's not the right frame.

A virtual chief financial officer is better understood as your financial co-pilot. The bookkeeper keeps the engine maintained. The tax accountant makes sure the aircraft is cleared to fly. The CFO sits beside you in the cockpit and tells you whether your route, fuel and timing make sense before you hit trouble.

The difference between recording and steering

The practical difference comes down to time and decision-making.

A bookkeeping function is mostly about accuracy, order and completion. Were the transactions coded properly? Have the accounts been reconciled? Is payroll processed? Has BAS support been prepared?

A CFO function asks different questions:

Cash position: Can the business fund payroll, supplier payments and tax obligations over the next period?

Margin quality: Which jobs, products, customers or channels are making money?

Growth pressure: Will additional sales improve cash, or swallow more of it?

Decision support: What happens if you hire, raise prices, open a location, buy equipment or carry more stock?

That's why the role matters most when complexity rises faster than the internal finance function.

A good virtual CFO doesn't just report that cash is tight. They show why it's tight, what caused it, and which lever to pull first.

Why the model works now

This model works because Australian businesses now have better financial plumbing than they did years ago. The viability of virtual CFOs in Australia is tied to the spread of digital finance tools and cloud accounting platforms, supported by the ATO's digital service ecosystem, which makes timely data available for forward-looking forecasting and KPI analysis, as explained in this overview of virtual CFO KPI reporting.

In plain English, that means a remote finance leader can work from live or near-live data instead of waiting for month-end packs that arrive too late to be useful.

If you're using tools like Xero, MYOB, QuickBooks, Dext, Hubdoc, Employment Hero, Deputy, Shopify, Cin7, Unleashed or a job management platform, a virtual CFO can usually pull the financial story together without sitting in your office.

What doesn't work is hiring someone for “strategy” while the underlying data is a mess. If bank feeds are unreliable, stock records are wrong, payroll controls are loose, and reporting arrives weeks late, the virtual format isn't the problem. The finance stack is.

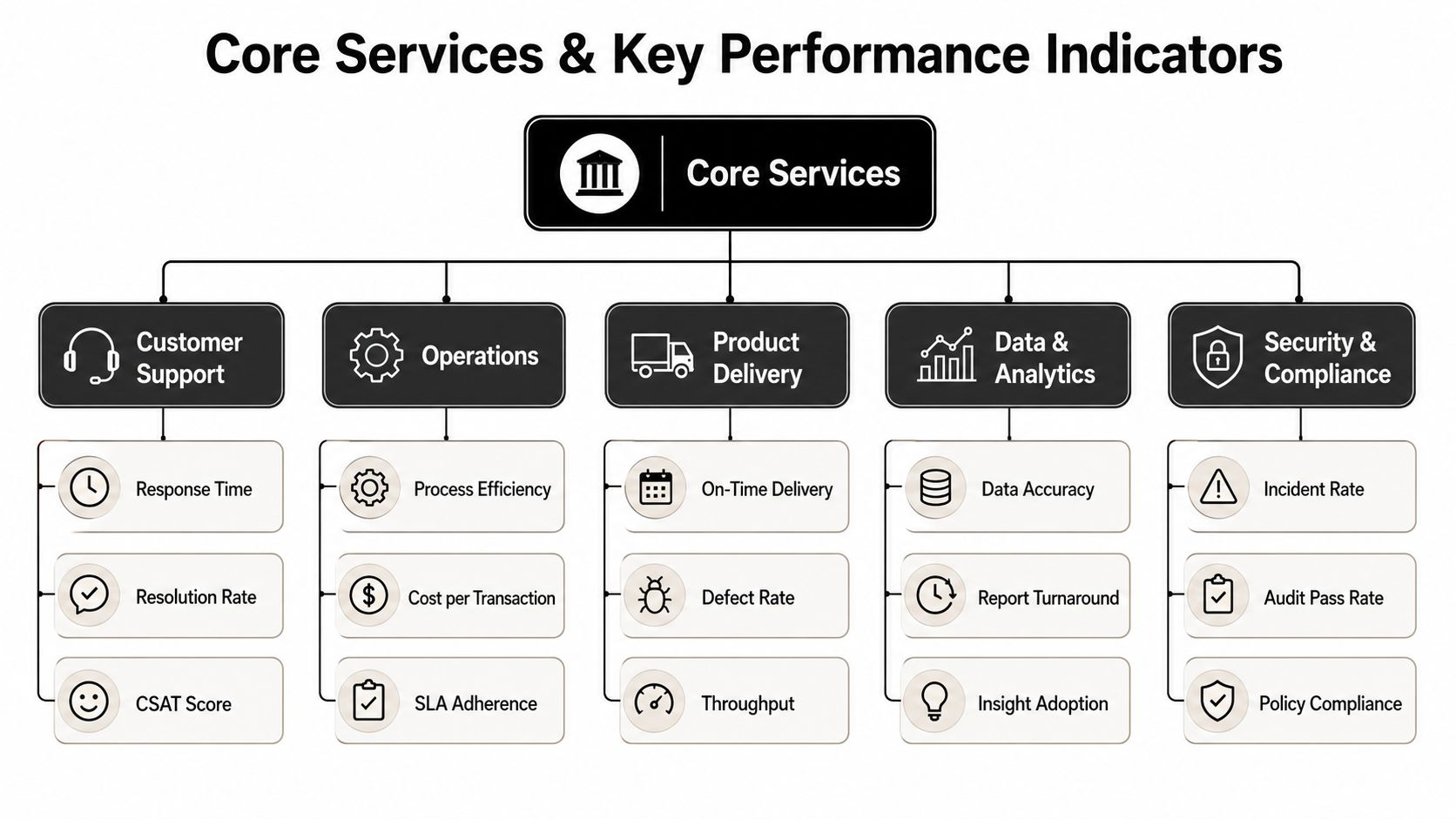

Core Services and Key Performance Indicators

A virtual chief financial officer earns their keep by converting scattered finance activity into a managed system. Not more reports. Better control.

What the work looks like in practice

At a practical level, the core services usually include:

Forecasting and budgeting: Rolling cash flow forecasts, scenario planning, hiring decisions, and spending limits that reflect actual trading conditions.

Performance reporting: Monthly dashboards that connect revenue, gross profit, operating expenses and cash movement instead of dumping a generic P&L in your inbox.

Working capital management: Receivables follow-up, inventory review, supplier term analysis, and timing decisions around large purchases.

Debt and funding support: Better visibility for loan applications, covenant monitoring, and clearer information for lenders or investors.

Systems improvement: Tightening workflows across invoicing, approvals, payroll, purchasing and stock control so the business isn't leaking cash through admin friction.

These services only work if the underlying data is clean. That's why reconciliation still matters. A useful practical reference is DigiParser's guide on account reconciliation, because a forecast built on unreconciled numbers is like pricing a job from a tape measure with the first ten centimetres missing.

The KPIs that actually matter

For Australian SMEs, the most useful liquidity KPIs are the working-capital ratio, quick ratio, and cash conversion cycle, according to this guide to CFO KPIs and dashboards. The same source defines the quick ratio as (cash + marketable securities + accounts receivable) / current liabilities, and the cash conversion cycle as Days Inventory Outstanding + Days Sales Outstanding − Days Payables Outstanding.

Those sound technical, but the logic is simple.

KPI | What it tells you | Why founders should care |

|---|---|---|

Working-capital ratio | Whether current assets can cover current liabilities | Helps you see short-term pressure before it becomes a scramble |

Quick ratio | Whether the business can meet near-term obligations without relying on selling stock | Useful when inventory looks valuable but can't turn into cash quickly |

Cash conversion cycle | How long cash stays tied up in stock and receivables before it comes back | Critical for retail, ecommerce, wholesale, manufacturing and project businesses |

For an inventory-heavy business, the cash conversion cycle is often the metric that tells the truth fastest. Revenue can rise while cash worsens because you bought stock earlier, held it longer, and collected customer cash later.

For a service business or trade business, a shorter list often matters more: debtor days, labour recovery, gross margin by job, committed overhead, and cash due in the next period.

If you want a broader view of which metrics deserve dashboard space, this guide to business performance indicators is a useful starting point.

Practical rule: If the KPI doesn't lead to an action, it's decoration.

Common Business Problems a Virtual CFO Solves

Most founders don't ask for a virtual CFO because they want “strategic finance”. They ask because something feels off.

Sales are happening, the team is busy, and still the business feels heavier than it should. That usually means cash is leaking through operations.

The issue is broad, not niche. Small businesses make up a huge share of the Australian economy, and around 5.2 million people are employed by small businesses, while working capital remains a constant challenge, as noted in this discussion of virtual CFO cash leak problems.

Cash flow leaks that hide inside growth

Growth often creates pressure before it creates relief.

An ecommerce business can have a strong month and still suffer because reorder decisions were made without a proper stock forecast. Best sellers sell out, slow lines sit too long, and cash gets trapped on shelves or in a warehouse. The founder feels busy, but the business has less flexibility.

A wholesale distributor gets hit differently. Debtor days stretch, large customers pay on their own timeline, and the owner keeps funding working capital from the business account. On paper, sales look healthy. In reality, customers are using the business as their bank.

A virtual CFO tackles this by narrowing the problem:

Receivables discipline: Invoice faster, chase earlier, segment debtors, and identify which accounts need tighter terms.

Stock control: Review stock turns, reorder points and purchasing patterns so buying follows demand rather than habit.

Payment timing: Match supplier terms to the operating cycle instead of paying early just because someone emailed twice.

Forecasting cadence: Run a rolling cash forecast that updates often enough to support decisions, not just post-mortems.

Margin and system problems that look smaller than they are

Margin leakage is quieter. It hides in discounting, freight recovery, job overruns, underquoted labour, warranty rework, and “small” software subscriptions no one owns.

For a trades business, that might mean the hourly rate looks fine until travel time, rework and scheduling gaps are layered in. For hospitality, it could be menu items with solid sales but weak contribution after wages and waste. For freight, the problem might sit in route profitability, fuel pass-throughs or customer-specific servicing costs.

Then there are systems. Manual approvals slow invoicing. Poor handovers create payroll mistakes. Stock counts don't reconcile with purchasing. People copy data between systems and assume someone else has checked it.

That's where a virtual CFO adds value beyond analysis. They connect operations to finance.

A founder who also owns client delivery should think the same way about internal metrics as they do about customer performance. This piece on essential client success KPIs is useful because it shows how service quality, retention and delivery metrics often feed financial outcomes more directly than owners expect.

The fastest way to improve cash isn't always more sales. Often it's fewer leaks.

When and How to Engage a Virtual CFO

Most businesses wait too long. They engage a CFO after the stress is obvious, when the better move was to bring one in when the signals first appeared.

The signs are usually operational first

You probably need a virtual chief financial officer when finance starts consuming founder energy out of proportion to the business size.

Common triggers include:

You don't trust the numbers: Reports arrive, but you still check the bank account to make decisions.

Cash surprises keep happening: Payroll, BAS, super, supplier bills or debt repayments feel more reactive than planned.

Growth is creating strain: More sales are bringing more stock pressure, more staffing complexity or more receivables drag.

A major decision is coming: Expansion, equipment purchases, funding, pricing changes or a restructure need proper modelling.

You've become the approval bottleneck: Every payment, every hire and every stock purchase comes back to you.

There's also a simpler sign. You're spending too much time stitching together spreadsheets from Xero, Shopify, payroll software and bank exports, and still not getting a clear answer.

A sensible engagement process

A good engagement shouldn't feel like hiring a Big Four advisory team to tell you things you already know.

The practical version usually looks like this:

Discovery conversation

The founder explains what hurts. Tight cash. Confusing margins. Messy reporting. Pressure around payroll, BAS or supplier timing.Quick diagnostic

Someone reviews the finance stack, recent reporting, workflows and risk points. The aim is to find the bottleneck, not write a thesis.Prioritised scope

The first work should be narrow and useful. Usually cash forecasting, reporting cleanup, margin review, or working-capital control.Operating rhythm

Monthly reviews, short decision meetings, clear ownership, and actions that feed back into the next month.

What doesn't work is a vague retainer with no clear outcomes, no access to the owner, and no implementation support. If the advisor only talks in boardroom language and never gets into invoicing delays, purchasing habits or payroll controls, you're paying for opinion, not results.

Comparing Your CFO Options and Pricing Models

Founders often compare the wrong things. They ask whether to hire a CFO or not. The central question is which model gives the business the right level of financial leadership without creating unnecessary overhead.

CFO Model Comparison

Attribute | In-House CFO | Fractional CFO | Virtual CFO Service |

|---|---|---|---|

Presence | Full-time employee inside the business | Part-time senior operator, sometimes on-site | Remote service delivered through cloud systems and scheduled cadence |

Best fit | Larger businesses with ongoing executive finance needs | Businesses needing senior input but not every day | SMEs needing strategy plus hands-on finance improvement |

Cost structure | Fixed salary and employment overhead | Part-time fee arrangement | Retainer or scoped service model |

Operational involvement | Can own finance team directly | Usually focused on high-level decisions and oversight | Often blends reporting, cash flow, systems and implementation support |

Flexibility | Lower. Harder to scale down | Moderate | Higher. Scope can adjust with business needs |

Speed to start | Slower recruitment and onboarding | Moderate | Usually faster if systems are cloud-based |

The trade-off is straightforward. An in-house CFO gives depth and internal availability, but only makes sense when the workload is there consistently. A fractional CFO can be ideal if you need senior judgement in bursts. A virtual CFO service often suits founder-led businesses that want both strategic guidance and practical finance execution without building a full finance department.

For some founders, the decision sits alongside broader wealth and capital planning. If that's part of your thinking, this article on private wealth advisor considerations gives helpful adjacent context.

How pricing usually works

Most providers use one of two pricing models:

Monthly retainer: Best when the business needs ongoing forecasting, reporting, reviews and operational follow-through.

Project-based fee: Better for a defined problem like cash flow cleanup, system redesign, pricing review, or funding readiness.

There isn't a universal “right price” because the scope drives the fee. A founder with a stable service business and clean books needs something very different from a wholesale operator juggling stock, debtors, payroll complexity and multiple systems.

A better way to judge value is to ask what the engagement should change.

If the work doesn't improve cash visibility, sharpen decisions, reduce founder firefighting or tighten control, the fee is too high even if it looks cheap.

The wrong buying behaviour is choosing the lowest-cost option and then expecting executive thinking, implementation support and accountability. Cheap finance advice often becomes expensive when nobody owns the outcomes.

The Australian Advantage A Localised Approach

In Australia, a virtual chief financial officer isn't just a growth partner. They're also part of your control environment.

That matters because the local compliance load isn't theoretical. BAS, PAYG, super, payroll, leave, awards, and record-keeping all sit close to cash flow. When owners separate “strategy” from “compliance”, they usually create blind spots.

Compliance is part of the job

A local finance lead should understand where operational pressure turns into compliance risk.

In 2023–24, the Fair Work Ombudsman recovered over A$470 million for workers, which highlights how costly wage and payroll failures can become for employers, as noted in this article on the rise of the virtual CFO. In practice, that means payroll accuracy, wage interpretation, super timing, and record-keeping aren't admin details. They are financial risk controls.

A capable Australian virtual CFO helps build:

Audit-ready payroll processes: Clear approvals, reconciliations and documented workflows

Cash buffers for statutory obligations: So super, tax and payroll don't compete with each other at deadline time

Monthly control routines: Review cycles for wages, entitlements, BAS inputs and payment timing

Better coordination across advisors: So bookkeeping, payroll, tax and leadership aren't all working from different assumptions

Local context changes the advice

Generic overseas CFO advice often misses what Australian founders deal with. A retailer here doesn't just need a margin dashboard. They need timing discipline around BAS, wages and supplier payments. A trades business doesn't just need better reporting. It needs confidence that payroll, super and project cash timing line up.

The best local advice sits at the intersection of finance operations and founder reality. It understands cloud accounting, but it also understands how Australian businesses run week to week.

If you want to see the kind of background that shapes this approach, Neha Malhotra's profile provides a useful reference point for the blend of accounting and operational finance leadership this work demands.

A virtual CFO should help you grow, yes. In Australia, they should also help you sleep.

If your business is profitable on paper but still feels tight in the bank, Nexist helps founders regain control of cash flow, margins and time. The team works with Australian SMEs to find cash leaks, improve forecasting, tighten systems and build a finance function that supports growth without founder burnout.

virtual chief financial officer, outsourced cfo australia, cfo services, cashflow management, business financial planning

" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="dSFdkJotL" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="wscNJE44G" transform="translate(0 0.129)" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="sTpjGo1tb" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="s7ffpmKOD" transform="translate(0 0.129)" width="24px"/><g d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.000006px" id="D0ecaHEcW" transform="translate(0 0)" width="24px"><path d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z" fill="rgb(55, 184, 218)" height="24.000006px" id="IPLFE6zXx" width="24px"/><path d="M 4.02 0 L 0 0 L 0 12.092 L 4.02 12.092 Z" fill="rgb(255, 255, 255)" height="12.09201px" id="FWhtzAyuY" transform="translate(2.863 8.375)" width="4.02px"/><path d="M 2.274 0 C 0.899 0 0 0.904 0 2.089 C 0 3.25 0.871 4.179 2.221 4.179 L 2.247 4.179 C 3.648 4.179 4.521 3.25 4.521 2.089 C 4.495 0.904 3.649 0 2.274 0 Z" fill="rgb(255, 255, 255)" height="4.17876px" id="VmOsKv4kO" transform="translate(2.625 2.545)" width="4.52095px"/><path d="M 7.641 0 C 5.509 0 4.554 1.173 4.019 1.996 L 4.019 0.284 L 0 0.284 C 0.053 1.419 0 12.376 0 12.376 L 4.019 12.376 L 4.019 5.623 C 4.019 5.262 4.045 4.9 4.151 4.642 C 4.442 3.92 5.103 3.172 6.214 3.172 C 7.667 3.172 8.25 4.282 8.25 5.907 L 8.25 12.376 L 12.269 12.376 L 12.269 5.442 C 12.269 1.728 10.286 0 7.641 0 Z" fill="rgb(255, 255, 255)" height="12.37626px" id="n1XUbhaq0" transform="translate(9.105 8.09)" width="12.268830000000001px"/></g></g></g></g></svg>)