Can You Claim Medical Expenses on Taxes 2026

Can you claim medical expenses on taxes in Australia for 2026? Understand ATO rules, deductions for business owners, & private health insurance rebates.

Ansh Malhotra

In Australia, you generally can't claim a tax deduction for personal medical expenses on your tax return. The big exceptions are narrow: some people can still access the Net Medical Expenses Tax Offset for specific disability aids or attendant care, and many founders get more value by managing the private health insurance rebate and avoiding the Medicare Levy Surcharge.

That's the part most search results get wrong. A lot of what people read about “medical expense deductions” is imported from the US, where itemised deductions work very differently. If you run a business in Australia, that confusion is more than annoying. It leads to bad tax assumptions, missed offsets, and poor cash flow planning.

Founders usually ask the wrong question. They ask, “Can you claim medical expenses on taxes?” The better question is, “Which medical costs are non-deductible personally, which ones are claimable in a business context, and which tax offsets reduce the damage?” That's where the actual money sits.

Table of Contents

The Short Answer Is No But That's Not the Whole Story

If you're asking can you claim medical expenses on taxes because you paid for dental, physio, prescriptions, glasses, or specialist appointments out of pocket, the answer for most Australians is no.

That's not a loophole you missed. That's the system.

Australian tax rules are not built around broad personal medical deductions. The ATO's framework is different, and it catches people who rely on US-style advice. As the ATO guidance makes clear, personal medical expenses, even for business owners, are typically non-deductible, and following overseas advice like the US 7.5% AGI threshold creates compliance risk in Australia through ATO guidance on income deductions offsets and records.

Why founders get tripped up

Business owners often blur personal and business spending. That's where errors start.

You pay personally and assume it's deductible: It usually isn't.

You run the cost through the business account: That doesn't make it deductible.

You read an overseas article: It may be accurate for another country and totally wrong here.

Practical rule: If the cost exists because you're a person needing healthcare, it's usually private. If the cost exists because the business or role requires it, you may have a claim.

What actually matters instead

The tax upside in Australia usually sits in three places:

Area | What it is | Why founders should care |

|---|---|---|

Personal medical costs | Usually not deductible | Stops you wasting time chasing invalid claims |

Tax offsets and rebates | Different from deductions | Can still reduce tax or premium cost |

Business-related health costs | Sometimes deductible | Legitimate claims improve cash flow and compliance |

The point isn't to force a claim where none exists. The point is to use the rules that apply.

Why Australia's Tax System Handles Medical Costs Differently

Australia didn't build its healthcare tax settings around itemised personal deductions. It built them around Medicare, the Medicare levy, and targeted offsets.

For most taxpayers, the Medicare levy is 2% of taxable income. That broad-based structure is one reason there isn't a general “claim your doctor bills” mechanism like people expect from US content. The government's approach is less about deducting ad hoc health spending and more about funding a public system, then using rebates and surcharge settings to push behaviour around private cover.

The old system is mostly gone

A lot of outdated advice still references the Net Medical Expenses Tax Offset as if it were broadly available. It isn't.

The offset was fully phased out on 30 June 2019 for general claims and replaced, in practical terms, by a system centred on the private health insurance rebate and the Medicare Levy Surcharge. In 2022 to 23, the private health insurance rebate delivered $6.7 billion in benefits to 12.5 million Australians through the framework outlined by the ATO private health insurance rebate rules.

Why this matters for cash flow

Founders tend to think in deductions. You should think in after-tax cash movement.

A deduction reduces taxable income. An offset reduces tax payable. A rebate can reduce premiums upfront or be claimed through the tax system. Those are not the same thing, and treating them as interchangeable leads to bad decisions.

Consider the practical difference:

A non-deductible personal expense: You wear the full cost.

A rebate on eligible private health insurance: You reduce the effective cost of cover.

A surcharge avoided: You stop extra tax from being added in the first place.

The smartest move isn't “claim everything”. It's “stop paying tax you didn't need to pay and stop booking private costs as business deductions”.

The founder's lens

If you own a company or operate as a sole trader, the risk is doubled. You can overclaim on the business side and underuse legitimate offsets on the personal side.

That's why the right mindset is simple:

Separate private health spending from business health spending.

Stop searching for a broad medical deduction that doesn't exist.

Focus on the narrow offset rules and the private cover settings that affect tax payable.

The Key Exceptions The Net Medical Expenses Tax Offset

There is still one narrow area where “medical expenses” can affect your tax directly. It's the Net Medical Expenses Tax Offset, and it survives only in limited circumstances.

For a specific group, this isn't relevant. For a small minority, it matters a lot.

Who can still use it

The remaining NMETO rules apply to people with eligible disability aids or attendant care expenses. Eligibility also depends on your net medical expenses exceeding the threshold.

For 2023 to 24, the threshold is $2,432, and the offset is 20% of the excess amount. The ATO also notes that only 0.5% of taxpayers claimed NMETO in 2022 to 23, which tells you how narrow this has become under the ATO medical expenses tax offset rules.

How the maths works

This is an offset, not a deduction.

That means you don't subtract the full eligible expense from income. You calculate the amount above the threshold, then apply the offset percentage to that excess.

An easy way to understand the process:

Step | What you do |

|---|---|

1 | Add up eligible net medical expenses |

2 | Subtract the threshold of $2,432 |

3 | Apply 20% to the excess |

4 | Claim the resulting offset if eligible |

If you don't clear the threshold, there's nothing to claim.

What founders should do with this

Most business owners should not assume this applies just because they spent a lot on health. It won't cover ordinary, everyday treatment just because the bill was painful.

Use this filter instead:

Relevant: Disability aids, attendant care, and other expenses that fit the ATO's narrow remaining rules.

Not relevant: Regular check-ups, standard dental, common prescriptions, general eyewear, and everyday personal healthcare unless they fall into a specific eligible category.

If you have to argue hard that a private medical cost is somehow “close enough”, it probably isn't claimable.

The real mistake to avoid

The danger isn't only missing a claim. The bigger danger is assuming every medical bill belongs somewhere in the return.

For most founders, NMETO is not the main lever. It's a specialist rule. If it applies, use it carefully and document it properly. If it doesn't, move on quickly and focus on the areas that genuinely change cash flow.

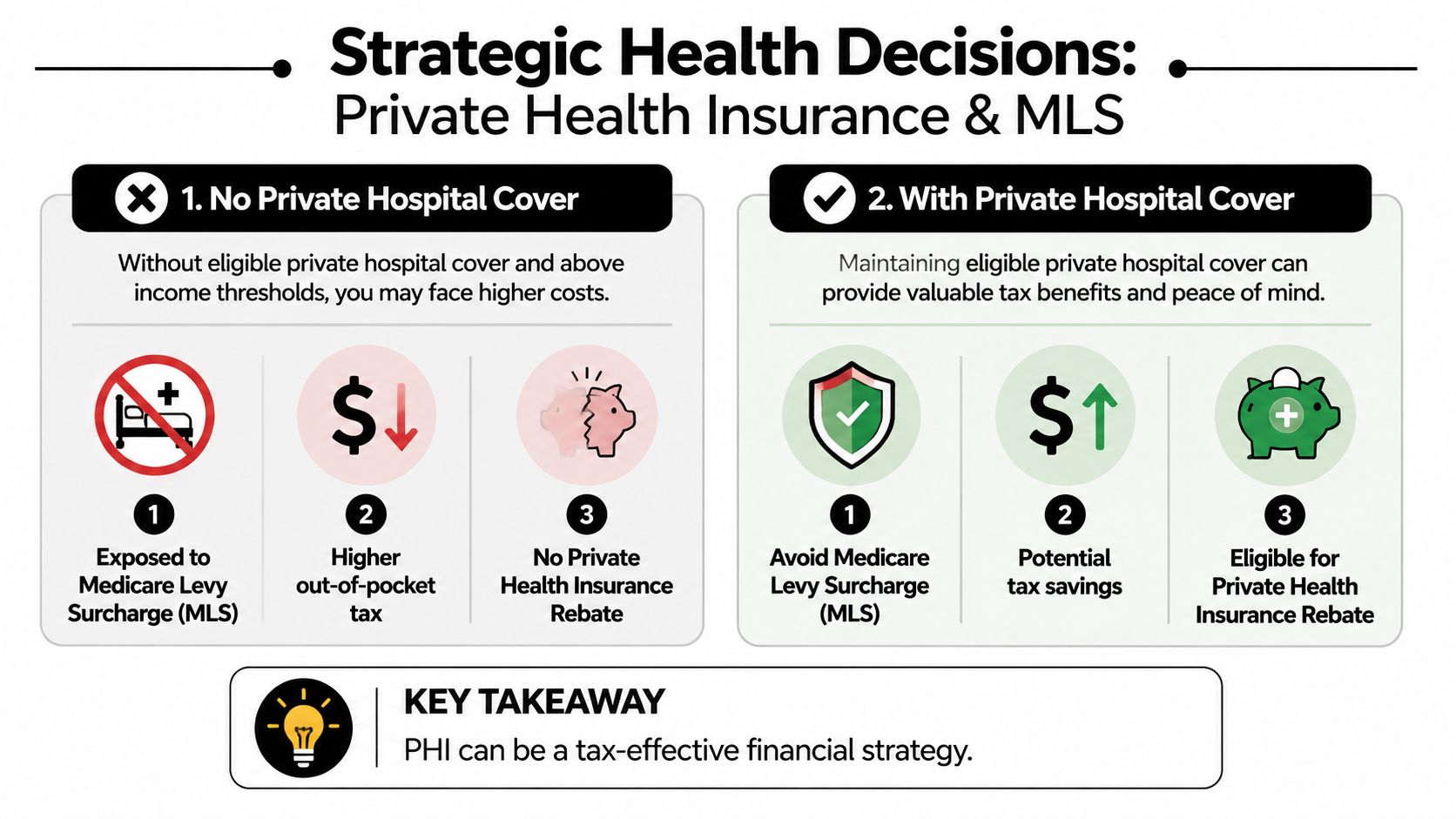

Strategic Tax Savings Private Health Insurance and the MLS

Most founders should pay attention to this topic. Private health insurance may not be exciting, but it directly affects tax.

The Australian system rewards some taxpayers for holding complying private hospital cover and penalises some who don't. If your income is above the relevant threshold, this stops being a health decision and becomes a cash flow decision.

The rebate and the surcharge work together

The private health insurance rebate is tiered by age and income. For singles under 65 earning less than $93,000, the rebate can be 24.608%. On the other side, higher-income earners without adequate private hospital cover may face the Medicare Levy Surcharge at 1% to 1.5%. The ATO notes that for a family income of $200,000, that can mean a tax hit of over $2,770, based on the ATO Medicare levy surcharge settings.

That's the key mechanic. One setting reduces your effective premium cost. The other adds tax if you go without qualifying cover.

The founder decision is usually straightforward

If your income is near or above the threshold, stop treating private cover as a lifestyle extra. Model it as part of your annual tax position.

Here's the practical comparison:

Scenario | Likely effect |

|---|---|

No complying private hospital cover | Possible MLS added to tax bill |

Complying private hospital cover | MLS may be avoided |

Eligible rebate tier | Premium cost reduced through rebate |

The wrong way to handle this is waiting until tax time to discover the surcharge.

The right way is reviewing the position before renewal and before year-end. If you want a plain-English breakdown of tax strategies for avoiding MLS, that guide is useful because it focuses on the decision itself rather than generic health insurance marketing.

Why this belongs in your cash flow model

Founders often focus on operating margins and ignore personal tax leakage. That's a mistake, especially when owner drawings and household cash affect business pressure.

If you're managing both business obligations and personal tax exposure, your private cover decision should sit in the same review cycle as BAS planning, salary strategy, and owner cash forecasting. A disciplined finance process matters more than the product itself. Tools and reporting support from firms like Nexist's finance and cash flow advisory team exist for exactly this reason, even if the underlying tax mechanics are still your responsibility to understand.

A founder who ignores MLS isn't being tax efficient. They're choosing surprise tax over planned cash outflow.

My recommendation

If you're above the income thresholds, review your private hospital cover before the year closes. Confirm it's complying cover. Confirm your rebate tier. Confirm whether you're exposed to MLS.

Do that once, properly. Then stop letting this issue drift.

Deductible Medical Costs for Business Owners and Founders

Here's where the conversation finally shifts from “mostly no” to “sometimes yes”.

Personal medical expenses are usually private and non-deductible. But some business-related health costs are deductible when they're directly tied to business activities or employment requirements. That distinction matters.

The line that matters

Ask one question first. Did the expense arise because of your personal health needs, or because the business or role required it?

If it's the first one, it's usually private. If it's the second, you may have a legitimate business claim.

The ATO allows self-employed people to claim work-related medical costs directly tied to business activities, such as health checks for occupational health and safety compliance. For employees, businesses can deduct wellness program costs like flu shots as FBT-exempt benefits up to $300 per employee annually, based on the ATO business income and deductions guidance.

What can be deductible in practice

Founders need discipline in these situations. A valid claim usually has a clear operational reason.

Role-required medicals: A medical assessment required for someone to perform a specific role can be deductible if it's tied to that work requirement.

OHS compliance costs: Health checks or treatments connected to occupational health and safety obligations are more likely to be claimable.

Employee wellness support: Benefits like flu shots can be deductible and may also fall within FBT-exempt treatment when structured properly.

Business-required vaccinations or testing: If the role or work environment makes them necessary, they may fall on the business side rather than the private side.

What usually is not deductible

A founder often tries to push personal wellbeing costs into the business because the business income paid for them. That isn't the test.

The following are typically private in substance:

Cost | Usual treatment |

|---|---|

GP visits for your own health | Private |

Dental treatment for you | Private |

General physio or therapy not tied to business requirements | Private |

Prescription medication for personal conditions | Private |

Routine personal eyewear | Private |

The FBT angle matters

If you employ staff, health-related support can create value beyond retention. It can also be structured sensibly.

A small wellness benefit that qualifies for FBT-exempt treatment is often cleaner than trying to reimburse random private costs later. That's especially true when you want a repeatable policy instead of ad hoc founder decisions.

Owner trap: Paying a private medical bill from the company account doesn't convert it into a business deduction. It often just creates bookkeeping clean-up and tax risk.

A better way to think about it

Treat medical spending in one of three buckets:

Private owner expense

Keep it out of the P&L as a tax deduction unless there is a clear business basis.Employee benefit with defined treatment

Build a simple policy for eligible wellness support and document it.Operational health cost

Link it to OHS, role requirements, or compliance. Keep evidence showing why the business incurred it.

If you're a sole trader, be even stricter. The line between you and the business is thinner in practice, but the ATO still expects a real connection to income-producing activity or business compliance.

Your ATO Checklist Record Keeping and How to Claim

Good tax outcomes come from good records. Not heroic memory in June.

If you're claiming anything connected to medical costs, the ATO will expect the paperwork to show what the expense was, who incurred it, when it was paid, and why it qualifies. That applies whether you're dealing with an offset, a rebate, or a business deduction.

What to keep for each type of claim

Don't lump everything into one folder called “medical”. Split records by claim type.

For NMETO claims: Keep invoices, receipts, and any supporting documents that show the expense fits the eligible category.

For private health insurance rebate and MLS review: Keep your annual statement from the health fund and confirm the policy details match your return.

For business deductions: Keep tax invoices, payment proof, and documentation showing the business purpose or role requirement.

For employee wellness items: Keep the policy, the invoices, and a clear record of which employees received the benefit.

A simple document workflow matters more than fancy software. But if your files are scattered across inboxes, PDFs, and chat threads, a tool like a Finance tax document analyzer can help pull information out of statements and supporting documents faster before you hand them to your accountant.

How to lodge without making a mess

If you use myTax, enter each item in the section that matches its treatment. Don't force everything into “deductions” because that's the word you recognise.

Use this order:

Review your private health insurance statement first.

Confirm whether any NMETO claim is eligible.

Separate business-related health costs from private costs before you send records to your bookkeeper or tax agent.

Make sure the bookkeeping system doesn't code private owner spending into business expense accounts.

If you want more practical finance clean-up and record discipline, the articles on the Nexist blog for founders and finance operations are useful because they focus on systems, not just year-end theory.

A quick refresher can also help if you're unsure what the ATO expects in a return workflow:

The checklist I'd give any founder

Check | Why it matters |

|---|---|

Separate private and business medical costs | Prevents invalid deductions |

Keep insurer statements | Supports rebate and MLS reporting |

Retain invoices and proof of payment | Basic ATO evidence |

Document business purpose | Critical for OHS and employee claims |

Review coding before year-end | Stops messy reclasses later |

Clean records save more time than clever tax arguments.

FAQ When to Call Your Virtual CFO

Can I claim dental work

For the majority of taxpayers, no. Standard dental spending is usually a private medical expense, which means it isn't deductible just because you paid it yourself or paid a lot for it.

If you're trying to answer can you claim medical expenses on taxes by looking at personal dental bills, you're usually looking in the wrong place.

What about glasses or contact lenses

Usually private as well.

The narrow NMETO rules are the exception zone, not the default rule. If the expense doesn't fit those remaining eligibility settings, ordinary eyewear generally won't become deductible just because it helps you work better.

Are cosmetic procedures ever claimable

Usually no if they are personal in nature.

The tax treatment turns on the underlying character of the expense. If it's private healthcare for you as an individual, calling it important doesn't change the tax outcome.

What if I'm a sole trader

You still don't get to claim private medical costs just because you work for yourself.

That's one of the biggest misconceptions in small business tax. Being self-employed doesn't convert private health spending into a business deduction. You need a direct business connection, such as a work-related medical cost tied to business activities or compliance requirements.

What about employee flu shots or wellness support

These can be worth doing properly.

Where the benefit fits the ATO rules, a business can deduct eligible wellness costs, and some benefits can be FBT-exempt up to $300 per employee annually under the business guidance cited earlier. The win isn't just tax. It's clean policy, cleaner records, and fewer arguments later.

When should a founder get help

Bring in a finance lead when any of these are true:

You mix private and business spending regularly: That creates tax and reporting errors.

You're above the MLS thresholds: Private cover becomes a tax planning issue, not just a personal one.

You employ staff and offer benefits: FBT treatment needs to be handled properly.

Your bookkeeping is reactive: Claims get missed, and bad coding spreads through BAS, reporting, and year-end tax.

You want owner cash flow clarity: Personal tax decisions often pressure business cash more than founders realise.

If you want a credible operator's view on that kind of finance leadership, Neha Malhotra's background and approach to growth accounting gives a good sense of what strong virtual CFO support should look like.

The bottom line is simple. Most Australians can't claim personal medical expenses as a deduction. Founders should stop chasing that myth and focus on what changes cash flow: valid business-related health deductions, the narrow NMETO rules where they apply, and disciplined management of private health insurance rebates and MLS exposure.

If you want help turning tax rules into better cash flow decisions, Nexist helps Australian founders clean up reporting, tighten systems, and stop money leaking through bad finance habits.

Authored using Outrank app

claim medical expenses taxes, ato medical expenses, tax deductions australia, nmeto, business tax advice

" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="dSFdkJotL" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="wscNJE44G" transform="translate(0 0.129)" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="sTpjGo1tb" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="s7ffpmKOD" transform="translate(0 0.129)" width="24px"/><g d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.000006px" id="D0ecaHEcW" transform="translate(0 0)" width="24px"><path d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z" fill="rgb(55, 184, 218)" height="24.000006px" id="IPLFE6zXx" width="24px"/><path d="M 4.02 0 L 0 0 L 0 12.092 L 4.02 12.092 Z" fill="rgb(255, 255, 255)" height="12.09201px" id="FWhtzAyuY" transform="translate(2.863 8.375)" width="4.02px"/><path d="M 2.274 0 C 0.899 0 0 0.904 0 2.089 C 0 3.25 0.871 4.179 2.221 4.179 L 2.247 4.179 C 3.648 4.179 4.521 3.25 4.521 2.089 C 4.495 0.904 3.649 0 2.274 0 Z" fill="rgb(255, 255, 255)" height="4.17876px" id="VmOsKv4kO" transform="translate(2.625 2.545)" width="4.52095px"/><path d="M 7.641 0 C 5.509 0 4.554 1.173 4.019 1.996 L 4.019 0.284 L 0 0.284 C 0.053 1.419 0 12.376 0 12.376 L 4.019 12.376 L 4.019 5.623 C 4.019 5.262 4.045 4.9 4.151 4.642 C 4.442 3.92 5.103 3.172 6.214 3.172 C 7.667 3.172 8.25 4.282 8.25 5.907 L 8.25 12.376 L 12.269 12.376 L 12.269 5.442 C 12.269 1.728 10.286 0 7.641 0 Z" fill="rgb(255, 255, 255)" height="12.37626px" id="n1XUbhaq0" transform="translate(9.105 8.09)" width="12.268830000000001px"/></g></g></g></g></svg>)