Transaction Advisory Services: SME Success in 2026

Unlock your business potential with transaction advisory services. Australian SMEs: navigate due diligence, valuations, & prepare for successful deals in 2026.

Ansh Malhotra

You're probably not searching for transaction advisory services because you love finance jargon. You're searching because something material is coming. A sale. A buy-in from an investor. A management buyout. An acquisition target you don't want to overpay for. Or maybe you're not in market yet, but you know your numbers don't feel transaction-ready.

That's where most founders get stuck. They assume transaction advice starts when the data room opens and lawyers begin sending mark-ups. In practice, value usually gets created earlier, when someone works through the finance mess that would otherwise show up in diligence. Weak stock controls, patchy debtor collections, unclear margins by product line, revenue that looks fine in the P&L but converts poorly to cash. Those issues don't just slow a deal down. They shape price, terms, risk allocation and buyer confidence.

Table of Contents

What Are Transaction Advisory Services?

A founder decides it might be time. Maybe they've had an unsolicited approach. Maybe succession is on the horizon. Maybe they want growth capital but don't yet know what the business would look like through an investor's eyes. They ask their accountant for a valuation, speak to a lawyer, and then realise nobody has yet answered the practical question: what will a buyer, lender or investor challenge?

That gap is where transaction advisory services sit. In plain English, it's the financial and operational health check around a material business event. It's designed to tell you what the business looks like once the headline accounts are adjusted for deal reality.

Why it matters in Australia

This isn't a niche service for listed companies and private equity funds. In Australia, the transaction market is large enough that specialist advice matters across the SME end of the market too. Australia recorded 273 announced deals in Q4 2023, making it the largest M&A market in the Asia-Pacific region by deal count in that quarter, and reported deal value of about US$39.4 billion, according to KPMG deal data summarised by Mergers & Inquisitions.

When that much capital is moving, buyers get disciplined. Sellers get tested. Lenders ask sharper questions. Every acquisition, sale, carve-out or capital raise creates work around due diligence, valuation, tax, structure and completion mechanics.

Practical rule: A transaction doesn't expose brand-new problems. It exposes old problems that were never measured properly.

What founders usually need from it

For an SME owner, transaction advisory services usually mean help with things like:

Cleaning up earnings: separating recurring profit from one-offs, founder-specific costs, timing distortions and accounting noise.

Testing cash reality: checking whether reported profit turns into banked cash and whether working capital behaves the way management says it does.

Preparing for scrutiny: getting documents, reconciliations, contract summaries and explanations into a form that can survive diligence.

Shaping deal terms: making sure the business isn't penalised for avoidable uncertainty in settlement accounts, earn-outs or warranty negotiations.

Legal advice still matters, of course. If you want a plain-English legal perspective on transaction mechanics and issues that often surface around deals, Kons Law business transaction insights are a useful complement to the finance side.

The simplest way to think about TAS is this: it turns your internal version of the business into a transaction version of the business. Those two are rarely identical.

Inside the Transaction Advisory Toolkit

A good way to understand transaction advisory services is to think of a pre-purchase building inspection. The property might look fine from the street. The inspection tells you whether the roof is sound, whether the wiring is safe and whether the shiny renovation is hiding water damage.

A transaction works the same way. The management accounts tell a story. TAS tests whether the story holds up when money and risk transfer.

What diligence actually tests

The centre of the toolkit is usually financial due diligence. In Australian M&A, that often includes quality of earnings, proof of cash, normalised EBITDA or P&L adjustments, and net working capital analysis, as described in this overview of transaction advisory work.

Those terms sound technical, but the questions are straightforward.

Quality of earnings asks whether the profit is sustainable. If a result was lifted by a once-off project, unusual pricing, delayed maintenance, founder underpayment or revenue timing, a buyer will want that adjusted.

Proof of cash asks whether the accounting result lines up with bank receipts. A business can show profit and still have poor cash conversion if collections lag, revenue is recognised early, or balance sheet items aren't behaving properly.

Net working capital analysis asks how much cash must remain in the business at completion for it to trade normally. This matters a lot in SMEs because stock, debtors and creditor timing can swing sharply by month, season or purchasing cycle.

Buyers don't pay for profit they can't defend, and they don't like funding a working-capital hole after settlement.

For stock-heavy businesses, these reviews often expose slow-moving inventory, margin leakage, or stock that's technically on hand but commercially stale. For service firms, they often reveal WIP issues, debtor ageing concerns or revenue booked ahead of delivery.

The wider toolkit around the numbers

The full toolkit goes beyond a finance file review. It usually pulls together several disciplines:

Toolkit area | What it looks at | Why it matters |

|---|---|---|

Financial diligence | Earnings quality, cash conversion, balance sheet risks | Sets the baseline for value and negotiations |

Tax structuring | Historic tax exposures and transaction structure | Helps avoid unpleasant surprises and inefficient outcomes |

Commercial review | Customer quality, market position, contract durability | Tests whether growth assumptions are credible |

Legal review | Contracts, compliance, disputes, ownership issues | Identifies obligations that can change risk allocation |

Operational review | Systems, processes, reporting discipline, integration readiness | Shows whether the business can perform after close |

Technology now sits inside that toolkit more often than many founders expect. A buyer may ask how stock is tracked, whether reporting comes from Xero, MYOB or a spreadsheet patchwork, and whether key workflows depend on one person's memory. If your deal has a material systems component, how to protect your deal with technology is worth reviewing because tech diligence often surfaces operational risk that finance alone won't catch.

What doesn't work is treating TAS as a report-writing exercise. The best advisers convert findings into decisions. They show which issue affects price, which affects terms, which can be fixed quickly, and which should change the transaction structure altogether.

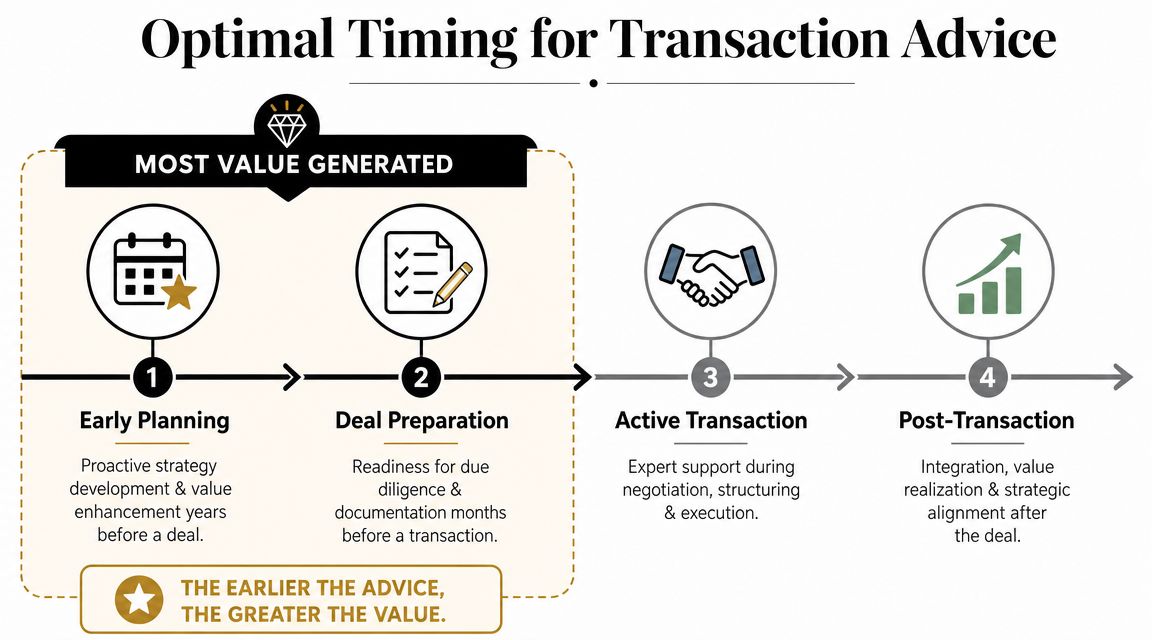

The Right Time to Seek Transaction Advice

Most founders engage transaction advisers too late. They wait until they're six months from market, or worse, after an inbound offer lands and momentum takes over. By then, everyone is trying to package the business attractively while hoping diligence doesn't uncover something expensive.

That's backwards. The strongest use of transaction advisory services is earlier, when there's still time to improve the business rather than explain it.

Why late engagement costs value

For many Australian SMEs, the biggest value leaks sit in working capital and process bottlenecks, not just headline EBITDA. That matters in a market where a large share of businesses have reported rising input costs and cash-flow pressure, a context highlighted in this discussion of SME transaction readiness.

If you only start looking at the business through a transaction lens at the point of sale, the likely outcome is one of these:

You discover cash leaks too late: overdue debtors, weak stock turns, messy rebates, and manual billing errors are now buyer discussion points.

You rely on explanations instead of evidence: management says margins are stable, but reports by customer, SKU or service line don't support the claim cleanly.

You negotiate from a weaker position: uncertainty flows into purchase price adjustments, earn-out debates, or broader protections for the buyer.

What to fix before you go to market

The useful question isn't “Do I need TAS now?” It's “What would fail under diligence if someone looked hard today?”

Founders planning growth capital or an eventual exit should usually look at transaction readiness in the same way they look at funding readiness. If you're reviewing capital options, practical guidance on funding the business sits naturally alongside transaction preparation because both depend on clean reporting, reliable forecasts and disciplined cash management.

A practical pre-transaction review often focuses on a short list:

Receivables discipline

Are aged debtors actively managed? Are credits, disputes and billing errors masking collection problems?Inventory accuracy

Do stock records match commercial reality? Are obsolete or slow-moving items distorting margin and working-capital needs?Margin clarity

Can you explain profit by product, service line, location or customer segment without rebuilding reports manually?Month-end quality

Are reconciliations current? Can someone external follow your numbers quickly without management translating every line?Forecast credibility

Does the cash forecast reflect actual trading behaviour, supplier terms and seasonality, or is it just a top-line plan?

The best time to prepare for diligence is when nobody is waiting for the file.

A founder who fixes those basics before a deal starts usually gets a better process. Not because the adviser “spins” the story better, but because there's less to defend and more to prove.

Real-World Scenarios for Aussie Businesses

Transaction advisory services become easier to understand when you look at how they behave inside different operating models. The work is not identical for every SME. The pressure points depend on how cash moves through the business.

An inventory-heavy business

Take an e-commerce brand, wholesaler or light manufacturer. Management may think the business is strong because revenue is holding and gross margin looks acceptable. A transaction adviser will go straight to stock ageing, purchasing patterns, shrinkage, write-down policy and how inventory ties up cash.

If the business carries too much slow-moving stock, the issue isn't just valuation of inventory on the balance sheet. It's also whether future purchasing has been distorted, whether discounting pressure is building, and whether cash has been trapped in product that won't turn at full margin.

A practical diligence lens asks:

Which stock lines turn predictably, and which don't

Whether stock records reconcile cleanly to the ledger

How supplier minimums affect working-capital swings

Whether gross margin is being flattered by stale cost assumptions

The founder often sees inventory as an operational issue. The buyer sees it as price, funding need and execution risk.

A service or trade business

Now take an agency, consultancy, contractor or specialist trade business. There may be little inventory, but that doesn't make diligence easier. The focus shifts to revenue quality, project profitability, customer concentration, pipeline conversion, and whether the owner is carrying too much of the commercial relationship load.

Here, TAS usually tests whether revenue is recurring, repeatable and properly recognised. It also looks for key person risk. If the founder wins the work, approves every quote, resolves every dispute and holds the client relationships personally, the business may be profitable but still harder to transfer.

A review might dig into:

Area reviewed | What the adviser is trying to understand |

|---|---|

Contract base | Are customers committed, or are revenues easy to lose? |

WIP and unbilled revenue | Is work being recognised consistently and defensibly? |

Customer concentration | Would one contract loss materially change the story? |

Delivery dependency | Can the business perform without the founder in every decision? |

A lot of owners expect TAS to confirm value. Often its first job is to show what kind of value is transferable. That's a different question, and usually the more important one.

How to Choose the Right Advisory Partner

A founder under pressure often defaults to the biggest name they recognise. That's understandable, but it isn't always the best choice. The right adviser is the one who can diagnose the issues that matter in your business model, communicate clearly with lenders or buyers, and help management act on findings before those findings become deal friction.

That distinction matters in a selective market. Recent Australian deal commentary points to buyers paying closer attention to business quality, downside protection and working-capital certainty, as noted in this transaction advisory perspective. In that environment, a generic provider can leave an SME with a polished report and very little operating improvement.

What good looks like

A strong advisory partner usually brings a few qualities that founders can test quickly.

Commercial fluency: they understand how your business makes money, not just how the accounts are presented.

SME fit: they're comfortable in imperfect environments where systems, reporting and ownership structures may still be evolving.

Decision focus: they don't just identify issues. They rank them by impact on value, timing and negotiability.

Operational awareness: they can see how finance problems are created by process problems.

For many founders, the bigger question is whether they need a one-off deal specialist or someone closer to an operator. If you're weighing that difference, what a virtual chief financial officer actually does is useful context because many transaction problems begin well before the transaction itself.

A good adviser doesn't make a business look better than it is. They help management make the business easier to believe.

Questions worth asking before you engage

Don't ask only about credentials. Ask how they work.

Try questions like these:

What issues do you see most often in businesses like mine?

How do you separate matters that affect price from matters that affect terms?

Can you help management fix reporting and working-capital issues before a process starts?

Who does the work, and who translates it to buyers, lenders and lawyers?

How do you handle founder-led businesses where information sits in people, not systems?

What doesn't work is an adviser who lives only in diligence, only in tax, or only in legal process. SMEs usually need someone who can bridge those worlds without overcomplicating them.

Beyond the Deal The Nexist Approach to Growth

The old model of transaction advisory services is project-based. A deal appears, advisers arrive, a diligence file gets built, and everyone rushes to explain the business in a compressed window. That still has its place. But it's rarely the best model for a founder-led SME whose biggest issues sit in cash flow, reporting discipline, inventory, debtor control and operating rhythm.

A more useful model starts upstream. The Asian Development Bank notes that transaction advisory services are most effective when they're used before capital is committed, to optimise capital structure and improve bankability, not only as post-hoc diligence. That broader framing appears in ADB's description of transaction advisory services. For SMEs, that means the best transaction outcome often begins with better finance operations.

Comparing advisory approaches

If the goal is to build a business that is stronger now and easier to transact later, the difference in service model matters.

Feature | Traditional Transaction Advisor | Nexist Integrated Virtual CFO |

|---|---|---|

Typical timing | Engaged around a live deal or imminent process | Engaged earlier to strengthen performance and readiness |

Main focus | Diligence, deal support, negotiation inputs | Cash flow, margins, reporting, systems and readiness |

Working style | Project-based and transaction-led | Ongoing and hands-on |

Value creation | Often identifies risks and explains them | Fixes operational finance issues before they hit diligence |

SME suitability | Strong for formal processes with established systems | Strong for founder-led businesses needing practical execution |

Post-deal utility | May reduce after completion | Continues through planning, execution and growth |

This approach fits businesses that want more than a transaction pack. They want cleaner month-end reporting, tighter receivables, better stock visibility, clearer profit drivers and a planning cadence that makes the business easier to fund, scale or sell. That's also why strategic preparation matters well beyond a deal cycle. Strategic and financial planning is what turns ad hoc finance into a business that can move when the right opportunity appears.

The strongest transaction readiness work doesn't feel like transaction work every day. It feels like good financial management, disciplined operations and fewer surprises.

If you want that kind of support, Nexist helps Australian founders improve cash flow, tighten margins, build finance systems and become transaction-ready long before a buyer or lender starts asking questions.

transaction advisory services, due diligence, business valuation, M&A Australia, SME finance

" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="dSFdkJotL" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="wscNJE44G" transform="translate(0 0.129)" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="sTpjGo1tb" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="s7ffpmKOD" transform="translate(0 0.129)" width="24px"/><g d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.000006px" id="D0ecaHEcW" transform="translate(0 0)" width="24px"><path d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z" fill="rgb(55, 184, 218)" height="24.000006px" id="IPLFE6zXx" width="24px"/><path d="M 4.02 0 L 0 0 L 0 12.092 L 4.02 12.092 Z" fill="rgb(255, 255, 255)" height="12.09201px" id="FWhtzAyuY" transform="translate(2.863 8.375)" width="4.02px"/><path d="M 2.274 0 C 0.899 0 0 0.904 0 2.089 C 0 3.25 0.871 4.179 2.221 4.179 L 2.247 4.179 C 3.648 4.179 4.521 3.25 4.521 2.089 C 4.495 0.904 3.649 0 2.274 0 Z" fill="rgb(255, 255, 255)" height="4.17876px" id="VmOsKv4kO" transform="translate(2.625 2.545)" width="4.52095px"/><path d="M 7.641 0 C 5.509 0 4.554 1.173 4.019 1.996 L 4.019 0.284 L 0 0.284 C 0.053 1.419 0 12.376 0 12.376 L 4.019 12.376 L 4.019 5.623 C 4.019 5.262 4.045 4.9 4.151 4.642 C 4.442 3.92 5.103 3.172 6.214 3.172 C 7.667 3.172 8.25 4.282 8.25 5.907 L 8.25 12.376 L 12.269 12.376 L 12.269 5.442 C 12.269 1.728 10.286 0 7.641 0 Z" fill="rgb(255, 255, 255)" height="12.37626px" id="n1XUbhaq0" transform="translate(9.105 8.09)" width="12.268830000000001px"/></g></g></g></g></svg>)