Australian SME Business Growth Strategy: Scale Without

Build a practical business growth strategy for your Australian SME. Find cash leaks, set profit targets, and scale efficiently without burnout.

Ansh Malhotra

You're probably feeling the strain already. Sales are coming in, the team is flat out, and yet the bank balance still looks tighter than it should. Payroll lands, BAS is around the corner, suppliers need paying, and somehow growth feels more stressful than stability ever did.

That's the trap many Australian founders fall into. They chase revenue, add channels, hire ahead of process, and end up with a bigger business that produces less breathing room. A workable business growth strategy for an SME has to start somewhere less glamorous but far more useful. Find where cash is leaking, fix that first, then scale what's left.

Table of Contents

Beyond More Sales A New Mindset for Growth

The old advice says if you want to grow, sell more. That works in a spreadsheet fantasy. It often fails in a real SME.

For 97.2% of Australian businesses that are SMEs, the primary growth constraint is often cash trapped in receivables and stock, not lack of demand. Recent ASIC reporting also points to cash-flow pressure as a primary driver of insolvency, which is why a stronger business growth strategy starts with improving profit per dollar of working capital, not pushing top-line sales at any cost, as discussed in Bain's analysis of the small business market.

When growth makes the owner poorer

A founder can double the number of jobs quoted and still feel worse off. I see it most often in trades, ecommerce, wholesale, hospitality, and service firms with long payment cycles. More work arrives, but cash leaves first.

A few familiar patterns show up:

Stock goes up before sales are banked. You buy deeper to avoid stockouts, then cash sits on shelves.

Debtors stretch. Customers pay later than expected while wages and supplier payments stay fixed.

Discounting masks weak pricing. Revenue rises, but each sale carries less contribution.

Admin expands with volume. More orders create more rework, more follow-up, and more founder time.

More revenue doesn't fix a weak cash engine. It often exposes it.

That's why a practical business growth strategy for Australian SMEs starts with a different question. Not “How do we sell more?” but “What type of growth leaves more cash in the business after delivery, tax, stock, and labour?”

Marketing only works when operations can absorb demand

This doesn't mean demand generation doesn't matter. It does. But demand without financial control creates chaos faster.

If you're reviewing channel mix or campaign structure, your guide to push and pull marketing is useful because it frames when to actively drive demand and when to build demand that compounds over time. The missing piece for many founders is that either approach only works if the back end of the business can price correctly, fulfil consistently, invoice quickly, and collect cash on time.

A stronger growth mindset looks more like this:

Old growth thinking | Cash-flow-led growth thinking |

|---|---|

More sales fixes everything | Better cash conversion funds growth |

Revenue is the scorecard | Cash, margin, and capacity are the scorecard |

Add staff to handle growth | Fix process before adding headcount |

Discount to win volume | Price for contribution and operational reality |

Founders don't need another motivational growth framework. They need a way to stop being busy and underpaid at the same time. That starts by defining what the business must produce in profit and cash.

Set Your Financial North Star Profit and Cash Targets

A founder looks at the P&L, sees a decent month, then checks the bank balance and delays drawings again. That gap is the problem. Growth only helps if it turns into cash you can keep after stock, wages, BAS, debt repayments, and the usual surprises that hit Australian SMEs.

The starting point is a financial target with two parts. How much profit the business must produce, and how much cash it must hold. If you only set a sales target, you miss the pressure points that decide whether growth feels manageable or exhausting. In practice, the businesses that grow cleanly usually know their margin floor, their minimum cash buffer, and the cash leaks that would break both.

Start with owner reality

I'd start from the owner's life and obligations, then work back into the numbers.

What does the business need to fund over the next 12 months? Personal drawings. Company tax. BAS. Loan repayments. Equipment replacement. A safer wage bill. Some breathing room for late-paying customers or seasonal dips. Once those items are visible, the business has a clear financial job.

A practical working method looks like this:

Set the owner requirement. Be specific about what you need the business to deliver in drawings and retained cash.

List fixed financial commitments. Include tax, debt, software, rent, planned hires, and known capital spending.

Set a profit target. This needs to cover both return and reinvestment, not just make the accounts look tidy.

Set a cash target. Decide the minimum bank balance or reserve that keeps the business stable through normal volatility.

For a broader planning framework, Nexist's article on strategic and financial planning is a useful reference because it ties commercial decisions back to financial discipline.

Turn annual goals into weekly control points

Annual targets are too slow on their own. By the time the year-end accounts confirm a problem, the cash is already gone.

Translate the North Star into a handful of operating numbers the team can influence every week:

Gross margin target. Protects profit from underquoting, input cost creep, and low-value custom work.

Minimum cash buffer. Sets the level of liquidity required before adding headcount, increasing stock, or taking on fixed costs.

Receivables target. Keeps sales from turning into owner-funded credit.

Inventory limit. Stops cash from sitting on shelves when it should be available for payroll, tax, or marketing that pays back quickly.

Capacity threshold. Shows when the current team can absorb more work and when process fixes need to come first.

That mix matters because trade-offs are real. A business can hit revenue and still starve itself if debtors blow out or stock turns slow down. Another can post modest sales growth and finish the quarter stronger because pricing improved, collections tightened, and unnecessary process steps were removed.

Practical rule: If you can't review a target weekly from your accounting file, cash-flow forecast, or AI-powered financial insights, it is too vague to manage properly.

The point of a North Star is not motivation. It is decision control. It tells you whether to push sales, hold pricing, buy less stock, chase overdue invoices harder, or postpone a hire until the business can fund it without strain.

Find the Leaks Diagnosing Your Margins and Cash Flow

Most cash problems don't arrive as one dramatic event. They show up as dozens of small decisions that nobody notices because the business is busy. A quote goes out with a stale price. Stock gets reordered too early. Invoices sit in draft. A team member does a task manually because nobody documented the better way.

The ATO's SME guidance aligns with a cash-flow-first growth strategy. It recommends cash-flow forecasting, timely invoicing, and diligent debt follow-up to avoid liquidity pressure. A common pitfall is showing an accounting profit while still struggling to meet payroll or tax obligations because cash is tied up in slow-paying debtors or excess stock. That's a useful lens to apply when reviewing where your own business is leaking cash.

Pricing leaks

Pricing problems rarely announce themselves. The business can look busy, customers may not complain, and yet margin keeps thinning.

Check for these warning signs:

Are you quoting based on habit instead of current input costs, labour time, and delivery complexity?

Discount creep. Small discounts become normal because nobody approves them properly.

Custom work with standard pricing. Bespoke jobs often consume more time than the quote allowed for.

No margin by customer or product. If you don't know where profit comes from, you'll keep feeding low-return work.

Freight or handling under-recovery. This is common in ecommerce, wholesale, and project businesses.

A useful test is simple. Review recent sales and ask which customers, products, or job types left cash behind after delivery. That answer is often different from which ones drove revenue.

Inventory and work in progress leaks

For product businesses, stock is one of the easiest places to lose cash. For service and project firms, the equivalent is work in progress that drifts, expands, or invoices late.

Watch for operational drift like this:

Overbuying for confidence. Owners carry too much stock because it feels safer than planning properly.

Slow-moving items. Cash gets parked in products that no longer turn cleanly.

No reorder logic tied to demand reality. Purchasing happens on instinct or supplier pressure.

Messy WIP handovers. Jobs move between team members without tight scope or billing controls.

Stock should serve demand. It shouldn't become a storage place for uncertainty.

Receivables, payables and process leaks

Receivables are where a lot of founders accidentally become a bank for their customers. Process leaks sit right beside them. If quoting, invoicing, collections, and approvals are inconsistent, cash timing becomes guesswork.

Use this diagnostic checklist:

Area | Questions worth asking |

|---|---|

Receivables | Are invoices going out immediately? Who follows up overdue accounts? Is there a clear escalation path? |

Payables | Are supplier terms aligned with your collection cycle? Are early payments being made without a reason? |

Admin process | How many handoffs occur from sale to invoice? Where do approvals stall? |

Reporting | Can you see overdue debt, stock position, and margin by line without spreadsheet hunting? |

If the reporting layer is fragmented, tools that surface AI-powered financial insights can help owners spot patterns faster, especially when management information sits across multiple systems. The point isn't to add another dashboard for the sake of it. The point is to make hidden cash leaks visible enough to act on.

For overdue collections specifically, a tighter receivables process matters more than most growth tactics. This guide to accounts receivable management is useful if debtor follow-up is still ad hoc inside your business.

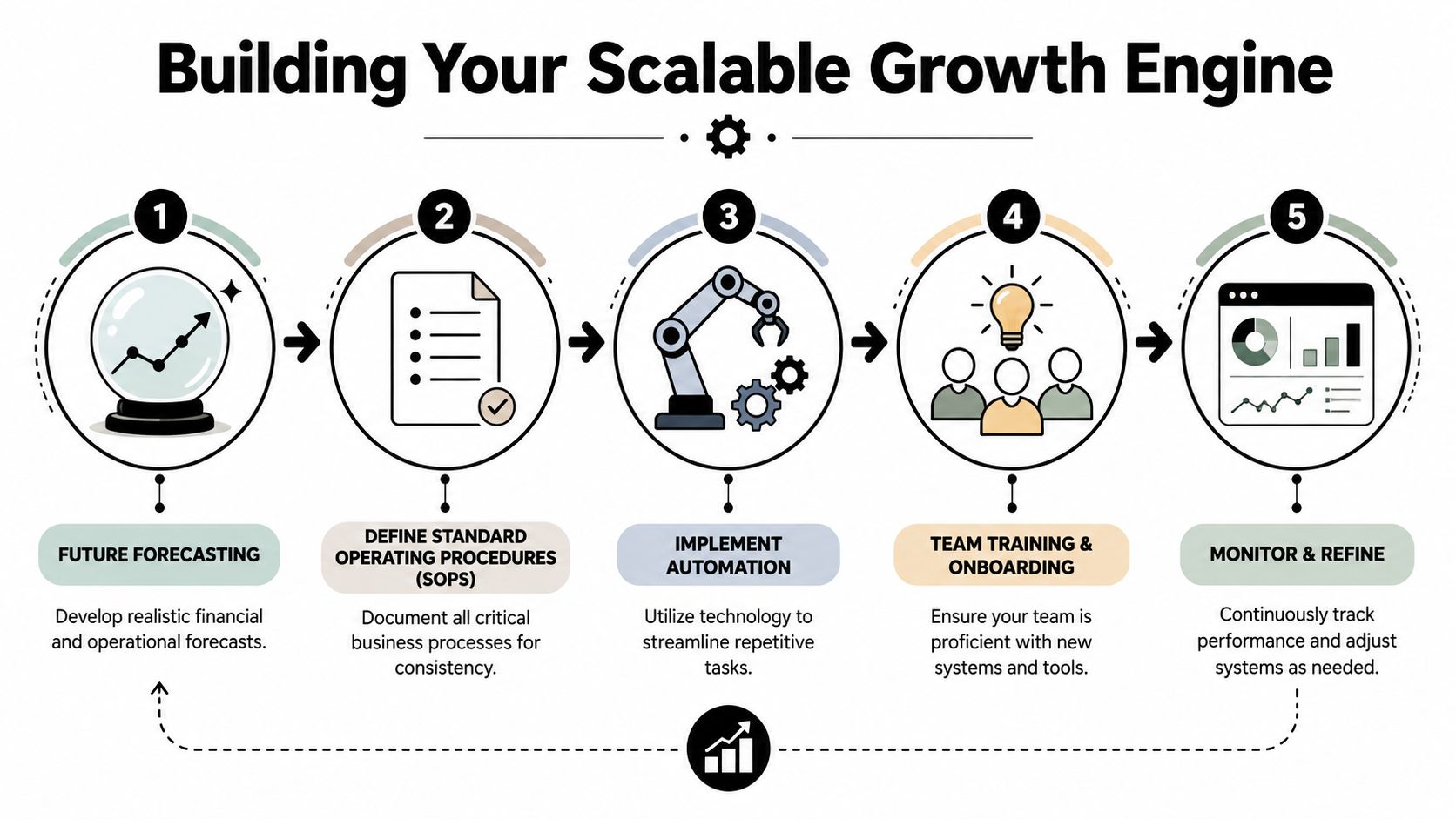

Build Your Growth Engine Forecasting, SOPs, and Automation

A founder sees sales climbing, the bank balance still feels tight, and every week brings another surprise bill, delayed payment, or stock order that landed at the wrong time. That pattern usually points to an operating system problem. Growth is being funded badly.

Once the cash leaks are visible, the next job is to stop them returning. That takes three things working together. A live forecast, clear SOPs around the moments that move cash, and automation applied to the right tasks.

Analysts and advisers have made this point for years. Businesses scale more reliably when they build repeatable processes around delivery, reporting, and decision-making, not just demand generation, as discussed in this overview of effective growth strategy execution.

Build a forward view before you need one

A weekly rolling cash forecast is one of the fastest ways to reduce stress in a growing SME. It gives owners time to act before pressure turns into a payroll squeeze, a tax problem, or a rushed funding decision.

Keep the forecast simple and current. The point is not precision for its own sake. The point is to see what will likely happen over the next 8 to 13 weeks and decide early.

Track the items that shift cash in actual operations:

Cash in. Expected collections by customer, based on actual payment behaviour rather than invoice due dates.

Cash out. Payroll, super, BAS, rent, supplier payments, debt repayments, and upcoming one-off costs.

Timing risks. Slower debtor receipts, project overruns, early stock buys, warranty claims, or seasonal dips.

Trigger points. The actions you will take if cash drops below a set buffer.

That last point matters. A forecast only helps if it changes decisions. It should tell you when to slow hiring, push collections harder, reorder later, tighten credit, or pause discretionary spend.

Here's a short explainer worth watching if you want a practical lens on building systems that support growth:

Write SOPs for the moments that affect cash

Founders often resist SOPs because they picture paperwork that slows everyone down. In practice, the right SOPs protect margin and reduce founder dependency.

Start with the workflows where inconsistency costs real money:

Quoting and pricing. Who approves discounts, variations, and non-standard terms?

Job or order handover. What must be confirmed before work starts or stock is committed?

Invoicing cadence. When is the invoice raised, what evidence is required, and who checks accuracy?

Collections workflow. Who follows up overdue accounts, on what schedule, and when does escalation happen?

Purchasing controls. Who can commit spend, at what level, and against which budget or stock threshold?

These do not need to be long. A one-page SOP that gets followed beats a ten-page document nobody reads.

The test is simple. A capable team member should be able to run the process the same way each time without waiting for the owner to step in. That is how a business gets consistent cash conversion instead of relying on memory and goodwill.

If the business depends on the owner remembering every critical step, it isn't scalable yet.

Use automation carefully

Automation can support a business growth strategy. It can also speed up bad habits if the underlying process is messy.

Use the sequence below:

Fix the process first. If the workflow is unclear, automation will repeat the confusion.

Assign ownership next. Each workflow needs one person accountable for the result.

Automate the repeatable steps. Invoice reminders, approval requests, low-stock alerts, recurring reports, and onboarding admin are common wins.

Review exceptions manually. Edge cases are often where margin slips and customer issues start.

I see this mistake often. A business automates purchasing before setting reorder rules, or automates invoicing before tightening job completion sign-off. The result is faster admin, but not better cash flow.

Used properly, automation frees up attention for the decisions that still need judgement. Firms such as Nexist work in this space by combining forecasting, process design, KPI reporting, receivables discipline, and automation into one operating model for founders who need tighter control without adding internal finance headcount.

Execute and Adapt Your Tactical Roadmap and KPIs

Monday starts with a healthy sales pipeline. By Thursday, payroll is due, two large invoices are still unpaid, and stock has arrived earlier than expected. Revenue is up on paper, but cash is tight. That is the gap this part of a growth strategy needs to close.

Execution works when the roadmap starts with cash movement, not a long wish list. For most Australian SMEs, the next ninety days should focus on a small number of actions that improve collection speed, protect margin, and reduce waste in day-to-day operations. If the plan does not change cash in the bank, it is too loose.

A practical ninety day operating rhythm

The best tactical plans are narrow enough to finish. Three priorities are usually enough.

Set one priority around cash leakage. That could mean overdue receivables, poor progress invoicing, loose discounting, or stock sitting too long on the shelf. Set the second around margin. Reprice low-return work, tighten freight recovery, or stop custom exceptions that chew up labour without paying for it. Set the third around execution discipline. Put in a weekly cash review, a tighter approval step, or a cleaner reporting pack.

That mix gives the business a fair trade-off. It improves today's cash position while building better habits for the next quarter.

A trade business might spend ninety days tightening quote approvals, invoicing at each project stage, and following up debtors every week. An ecommerce operator might focus on clearing dead stock, fixing pricing that misses fulfilment costs, and setting better reorder points. Neither plan sounds exciting. Both can release cash faster than chasing more top-line sales.

Track the KPIs that force action

Founders do not need twenty metrics. They need a short set that leads to decisions.

KPI | Why it matters |

|---|---|

Gross margin | Shows whether the work sold is producing enough contribution after direct costs |

Debtor days | Shows how long customers are holding your cash |

Cash runway | Shows how many weeks or months the business can operate if receipts slow |

Inventory turnover or stock cover | Shows whether cash is tied up in stock for too long |

Labour utilisation | Shows whether paid team capacity is converting into billable or productive output |

Review these numbers on a fixed rhythm. Weekly for cash, receivables, and stock exceptions. Monthly for the broader operating review.

Each KPI needs an owner, a target, and a response when it moves the wrong way. If debtor days blow out, someone follows up, changes payment terms, or stops work on chronic late payers. If margin drops, the team checks pricing, input costs, and job mix before the month disappears.

Adapt without losing focus

A roadmap should be stable for a quarter, but not rigid. Conditions change. Suppliers increase prices. A customer segment slows down. A new sales push creates more work than the team can deliver profitably.

Adjust the tactic, not the discipline.

If a pricing change improves margin but slows conversion, review the offer structure before cutting price across the board. If stock levels come down but service levels slip, refine reorder rules rather than buying heavy again. If marketing is producing leads but reporting is messy, fix attribution before increasing spend. Clean reporting matters here, especially when you are solving marketing data discrepancies and trying to work out which channels are producing profitable customers rather than noisy activity.

This is also the point where better financial leadership starts paying for itself. A founder can keep the cadence running, but the process gets stronger when someone is accountable for turning numbers into decisions, pressure-testing trade-offs, and keeping the plan tied to cash outcomes. That is the practical value of a virtual chief financial officer for growing SMEs.

From Watchman to Visionary When to Engage a Virtual CFO

At a certain point, founder-led finance stops being lean and starts being expensive. Not because the salary line is wrong, but because the owner's time is going into the wrong work.

What usually changes first

The first sign isn't always a financial crisis. It's often decision fatigue.

The owner is still reviewing quotes, checking overdue invoices, second-guessing stock buys, approving payroll questions, and trying to interpret reports late at night. Strategy gets reduced to reaction. The founder becomes the watchman for every moving part.

That's usually when growth stalls in a subtle way. Opportunities are there, but the business can't absorb them cleanly because the financial and operational core still depends on founder attention.

When founder-led finance stops being efficient

A virtual CFO makes sense when the business needs sharper decision support without hiring a full internal finance team. The role is less about bookkeeping and more about building the commercial operating system around cash, margin, and accountability.

Typical triggers include:

Cash flow feels unpredictable. You're still surprised by upcoming shortfalls.

Reporting exists but doesn't guide action. You get numbers, not decisions.

Growth is creating complexity. More staff, locations, stock lines, or customer segments are exposing weak controls.

The founder is carrying too much finance admin. Time is being spent on follow-up, interpretation, and firefighting rather than leadership.

Marketing and sales data don't line up with financial outcomes. If attribution, reporting, and commercial performance are telling different stories, resources get allocated badly. In that case, this piece on solving marketing data discrepancies is useful because bad data can distort both customer acquisition decisions and cash planning.

A good virtual CFO should help the owner move out of the watchman role. That means building the forecast, tightening KPI review, improving collections discipline, setting profit targets, and making sure growth decisions are tested against cash consequences.

If you're weighing whether that support is the right next step, Nexist's overview of a virtual chief financial officer gives a practical picture of what the role should do inside an SME.

If your business is growing but cash still feels tight, Nexist helps Australian founders plug profit leaks, build cash-flow forecasts, tighten receivables, and put simple systems around pricing, stock, reporting, and operations. The result isn't abstract strategy. It's clearer decisions, more time back, and more cash staying in the business.

business growth strategy, sme growth australia, virtual cfo, cash flow management, profitability strategy

" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="dSFdkJotL" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="wscNJE44G" transform="translate(0 0.129)" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="sTpjGo1tb" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="s7ffpmKOD" transform="translate(0 0.129)" width="24px"/><g d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.000006px" id="D0ecaHEcW" transform="translate(0 0)" width="24px"><path d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z" fill="rgb(55, 184, 218)" height="24.000006px" id="IPLFE6zXx" width="24px"/><path d="M 4.02 0 L 0 0 L 0 12.092 L 4.02 12.092 Z" fill="rgb(255, 255, 255)" height="12.09201px" id="FWhtzAyuY" transform="translate(2.863 8.375)" width="4.02px"/><path d="M 2.274 0 C 0.899 0 0 0.904 0 2.089 C 0 3.25 0.871 4.179 2.221 4.179 L 2.247 4.179 C 3.648 4.179 4.521 3.25 4.521 2.089 C 4.495 0.904 3.649 0 2.274 0 Z" fill="rgb(255, 255, 255)" height="4.17876px" id="VmOsKv4kO" transform="translate(2.625 2.545)" width="4.52095px"/><path d="M 7.641 0 C 5.509 0 4.554 1.173 4.019 1.996 L 4.019 0.284 L 0 0.284 C 0.053 1.419 0 12.376 0 12.376 L 4.019 12.376 L 4.019 5.623 C 4.019 5.262 4.045 4.9 4.151 4.642 C 4.442 3.92 5.103 3.172 6.214 3.172 C 7.667 3.172 8.25 4.282 8.25 5.907 L 8.25 12.376 L 12.269 12.376 L 12.269 5.442 C 12.269 1.728 10.286 0 7.641 0 Z" fill="rgb(255, 255, 255)" height="12.37626px" id="n1XUbhaq0" transform="translate(9.105 8.09)" width="12.268830000000001px"/></g></g></g></g></svg>)