Funding the Business: An AU Founder's Playbook for 2026

Struggling with funding the business in Australia? Our step-by-step playbook covers quantifying needs, comparing sources, and negotiating terms. Get funded.

Ansh Malhotra

Your bank balance is tighter than it should be. Stock is sitting too long, invoices are ageing, payroll is due, and someone has told you the answer is to “go raise capital”.

That advice is often backward.

For most Australian founders, funding the business isn't a pitch problem first. It's an operational finance problem first. If your margins are unclear, your cash conversion is sloppy, and your forecast changes every time someone opens Xero, external money won't fix much. It usually just gives the same problems more runway.

That's why strong businesses become fundable from the inside out. In Australia, approximately 60% of SMEs initiate operations using founders' personal savings, while 43% of AU SMEs under $10M revenue cite access to finance as their top barrier, with women-led firms facing 30% higher rejection rates. That combination tells you something important. Most founders start by backing themselves, then hit a wall when formal capital asks for cleaner numbers than they can produce.

Table of Contents

Funding Starts Before Your First Pitch

A founder usually starts fundraising when the pressure is already high. The cash account looks thin. Suppliers want payment. A large order is coming, but the working capital to fulfil it isn't there. In a service business, the same feeling shows up when wages and contractor costs run ahead of client receipts.

That's the worst moment to begin acting like funding is a separate project.

If you walk into a bank, lender, investor, or grant assessor with unresolved cash leaks, they'll see the same thing. They may not call it that. They'll call it weak forecasting, poor working capital management, inconsistent KPIs, or lack of visibility. It all means the same thing. You don't yet control the engine you want them to finance.

What funders actually respond to

Funders back clarity. They back discipline. They back businesses that understand where cash goes and why.

That means you need clean answers to questions like these:

Margin control: Which products, jobs, or customers produce profit after freight, rework, discounts, and owner time?

Cash timing: When does cash leave, when does it come back, and where does it get stuck?

Operational leakage: Are stockouts, over-ordering, slow debtors, or underquoted jobs creating the actual funding need?

Decision quality: Can you explain your numbers confidently without asking the bookkeeper to “pull a report later”?

Practical rule: If you can't explain why you need the money, you're not ready to ask for it.

This is why founders who focus only on “getting funded” often miss the easier win. They don't first reduce the amount of funding required. Better pricing, faster collections, tighter stock control, and cleaner purchasing discipline can shrink the hole before you ever submit an application.

For owners navigating this alongside personal financial pressure, it also helps to understand how business decisions interact with personal wealth settings. A good primer is this guide on when a private wealth advisor makes sense.

Fundable businesses are organised businesses

A fundable business has a rhythm. The accounts reconcile on time. Reporting is current. Revenue assumptions are grounded. Stock data matches reality. Debtors are actively managed. Creditors are planned, not avoided.

That doesn't make the business perfect. It makes it credible.

And credibility matters in a market where capital is available, but not casually. The founders who secure good funding terms usually aren't the ones with the flashiest deck. They're the ones who can prove that new money will go into a business already capable of turning it into profit and cash.

How Much Funding Do You Actually Need

Most founders start with a round number. “We need $200k.” “We need half a million.” “We need enough to get through the next year.”

That's not a funding requirement. That's a guess.

A proper funding number comes from a cash flow model that shows when money goes out, when it comes in, and how much headroom you need when things take longer than expected. That matters because cashflow volatility is linked to a 35% failure rate for some businesses, and the Reserve Bank of Australia notes a 28% denial rate for regional loan applications, which is why precise forecasting matters when you're asking for capital.

Start with the operating reality

Build your forecast from drivers, not hope.

For an ecommerce, wholesale, or manufacturing business, your key drivers usually include sales volume, average order value, gross margin, stock purchasing lead times, freight, merchant fees, payroll, rent, GST obligations, and debtor timing if you sell on terms. For a trade or service business, replace stock with labour utilisation, contractor costs, job pipeline, WIP conversion, and invoice collection speed.

Use an 18 to 24 month view if you're seeking material funding. Shorter models often hide the repayment reality.

Build it in layers

A practical founder model usually needs these steps:

Map revenue by month

Don't enter one annual figure and divide by twelve. Use seasonality, signed jobs, sales pipeline, repeat client behaviour, and realistic ramp-up assumptions.Map direct delivery costs

For product businesses, include stock purchases and freight timing. For services, include wages, contractors, software tied to delivery, and project-specific costs.Map fixed overheads

Payroll, rent, software, insurance, tax obligations, debt repayments, and owner drawings all belong here.Model timing, not just totals

Cash doesn't care when a sale is booked in the P&L. It cares when the customer pays.Add the capital use case

Show exactly what funding pays for. Inventory build, equipment, marketing test, hiring, debt refinance, or working capital support.

The strongest forecast is usually the boring one. It uses assumptions you can defend and survive, not assumptions designed to impress.

Separate need from ambition

Founders often blend two different goals into one raise. One is survival capital. The other is growth capital.

Keep them separate in your model. Survival capital keeps the lights on and smooths timing gaps. Growth capital should tie to a defined return path, such as stock for confirmed demand, a salesperson with a clear pipeline target, or equipment that lifts capacity.

A surprising number of weak applications fail because the owner can't distinguish between “I'm short on cash” and “this investment creates future cash”.

For businesses that need help thinking through supporting records and tax implications while building forecasts, even unrelated finance admin can sharpen discipline. Something as simple as understanding documentation standards in a piece like can you claim medical expenses on taxes shows the same underlying principle. Claims and applications stand up when records do.

Include a buffer without making it fluffy

You do need a contingency. But don't call it “miscellaneous”.

Define the buffer around known uncertainty. For example:

Inventory businesses: supplier delays, landed cost movement, slower sell-through

Trade businesses: project timing slippage, debtor delays, labour overruns

Service firms: churn, slower onboarding, utilisation dips

Then state your final number clearly. “We require funding to cover working capital troughs, support planned operating costs, and preserve a prudent buffer against timing delays.” That reads like management. It doesn't read like panic.

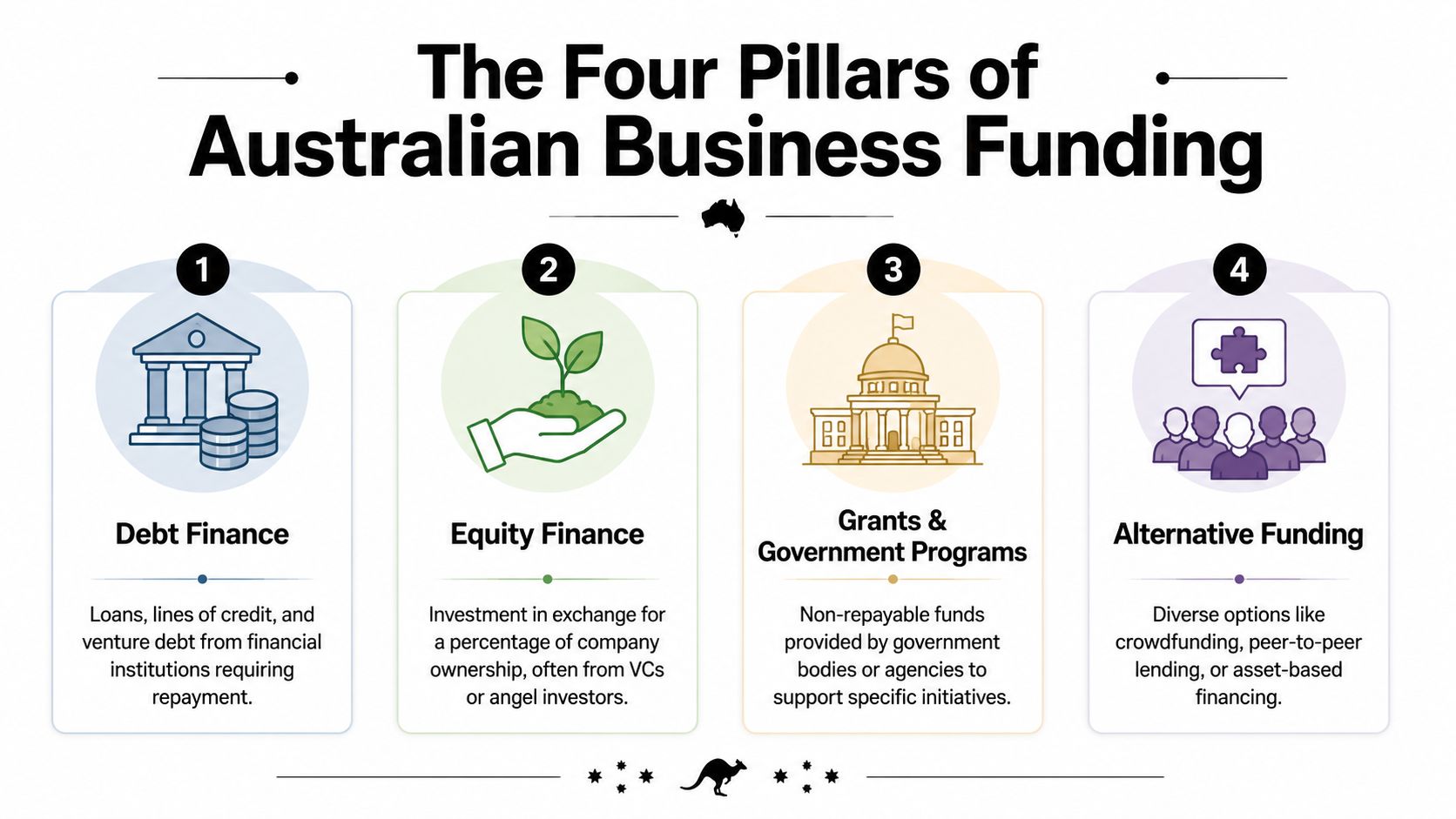

The Four Pillars of Australian Business Funding

Australian founders usually end up choosing between four broad paths. The right one depends less on what sounds attractive and more on your business model, cash profile, and tolerance for outside control.

Debt finance

Debt works best when the business can repay predictably. That usually means stable revenue, visible gross margin, and a credible forecast.

The attraction is obvious. You keep ownership. The trade-off is just as obvious. Repayments start whether conditions are easy or not. In Australia, average small business loans from major banks stand at $250,000, approval rates hover at 28% for businesses under 5 years old, and 50% of rejections are tied to inadequate forecasting or KPIs.

That tells you debt isn't only about credit appetite. It's about reporting quality.

Debt can suit trade, freight, hospitality, manufacturing, wholesale, and established service firms if the owner knows their working capital cycle cold. It's a poor fit for businesses still guessing at margins.

Equity finance

Equity is expensive in a different way. You don't make monthly repayments, but you do give up ownership, influence, and future upside.

For businesses with outsized growth potential, that can still be the right deal. But founders should be realistic about where equity money is flowing. In Australia, venture capital funding for startups totalled AUD 8.5 billion in 2023, but just 4% went to SMEs outside tech. If you run a solid service business, retail operation, or trade company, traditional VC may not be your market.

If you are venture-scale, a curated starting point can help. This list from Gritt can help you search for startup investors in Australia by investor profile rather than wasting time on broad outreach.

Equity is best when speed matters more than ownership retention, and when the business can grow into the dilution.

Grants and government programs

Grants look appealing because they don't dilute ownership and often don't require repayment. But they're not free money in the practical sense. They require eligibility, evidence, compliance, and a clean financial story.

Some founders overestimate their grant readiness. Others waste time applying for programs that never matched their business in the first place. Grants are strongest when the project clearly fits the scheme, the records are organised, and management can prove the business will execute what it proposes.

Alternative funding

This category covers invoice finance, asset-backed lending, revenue-based products, and specialist non-bank facilities. These can be useful where banks are too rigid or too slow.

The benefit is fit. A wholesaler with strong receivables may obtain funding against invoices. An equipment-heavy operator may use assets. A founder with uneven monthly cash may use a facility better matched to timing gaps.

The risk is that alternative products can hide expensive economics or restrictive terms behind speed and convenience. Read the structure, not just the headline.

Australian Funding Options at a Glance

Funding Type | Best For | Cost of Capital | Impact on Control | Key AU Example |

|---|---|---|---|---|

Debt Finance | Established businesses with reliable cash flow | Interest and fees | Low ownership impact, but lender oversight can be high | Bank term loan |

Equity Finance | High-growth businesses with strong scale potential | Dilution and future upside given away | High impact on founder control | Angel or VC round |

Grants & Government Programs | Eligible projects with clear compliance and reporting | Low direct capital cost, high preparation burden | No equity dilution | business.gov.au program |

Alternative Funding | Businesses with specific working capital or asset needs | Varies widely by structure | Usually limited ownership impact, but terms matter | Invoice finance facility |

How to choose without overcomplicating it

A simple decision filter works well:

Choose debt if cash flow is stable enough to service repayments.

Choose equity if growth potential is large and speed matters more than ownership.

Choose grants if your project clearly fits a program and your paperwork is tight.

Choose alternative funding if the need is tied to receivables, assets, or timing gaps that standard loans don't handle well.

The mistake isn't choosing one pillar over another. The mistake is choosing funding that fights your operating model.

Building Your Unforgettable Financial Pack

A good financial pack does two jobs at once. It helps a funder assess risk, and it forces you to run the business with sharper discipline.

If your pack is patchy, most conversations stall early. The lender asks for more information. The investor loses confidence. The grant application starts feeling like admin punishment.

The three documents that matter most

Start with the three-way forecast. That means profit and loss, balance sheet, and cash flow, all connected. If sales grow in the P&L, debtors, stock, tax, and cash should move accordingly. If they don't, the model isn't decision-grade.

Then build a KPI dashboard. Keep it short and commercial. For product businesses, include gross margin, stock turn, aged stock, debtor days, creditor days, and operating cash movement. For service firms, focus on utilisation, pipeline conversion, WIP, average project margin, debtor ageing, and forecast labour coverage.

The third piece is a concise business summary. Not a fluffy deck. A plain-English explanation of what the business does, who it serves, what problem it solves, how it makes money, where the cash gets stuck, and what the funding changes operationally.

A financial pack should answer questions before the funder asks them.

What lenders and investors look for

For venture debt in particular, lenders look for ARR over $2M and a DSCR above 1.25x, but 62% of ventures fail due to covenant breaches, often because businesses didn't model cash leaks like receivables ageing beyond 90 days. That's why dashboards and forecasting aren't decorative. They protect you after the money lands, not just before approval.

A practical pack usually includes:

Historical financials: Clean monthly data, not rough annual totals

Current management accounts: Recent and reconciled

Aged receivables and payables: Because timing matters

Forecast assumptions: Written down, not held in your head

Funding use schedule: Where every dollar goes

Sensitivity view: What happens if revenue lands later or costs rise sooner

A short explainer can also help your team align around the numbers before meetings start:

What weak packs usually get wrong

Weak packs tend to fail in familiar ways:

They confuse revenue with cash. The business may be “profitable” on paper while starving operationally.

They ignore working capital. Growth often increases the cash gap before it improves anything.

They bury risk. Experienced funders assume hidden issues when they can't see downside planning.

They lack ownership. If only the accountant understands the numbers, confidence drops fast.

A strong pack feels calm. The assumptions are visible. The trade-offs are stated. The owner can explain the model in a conversation, not just send a spreadsheet attachment and hope.

Approaching Funders and Negotiating Terms

Plenty of founders spend weeks polishing numbers and then sabotage the process with poor targeting. They approach the wrong funder, with the wrong ask, in the wrong format.

Start by matching your business to the funding style. Don't send an equity-style growth story to a commercial lender who only cares about serviceability. Don't send a bank-style file to an investor who wants market narrative and expansion logic. And don't apply for grants unless the project clearly fits the scheme.

How to approach the right funder

Your first contact should be brief and specific. A good introductory note covers:

Who you are: Industry, scale, and business model

What you need: Facility type or funding range

Why now: The commercial reason, not the emotional reason

Why it's supportable: Brief note on trading history, margins, or contract base

What you have ready: Forecast, management accounts, KPI pack, and use of funds

Don't write a novel. Write a clear commercial summary.

Grant applications require even more precision. Only 22% of Australian SMEs secure grants, and a CPA-certified practice can boost odds by 40%. Common pitfalls include inadequate cashflow forecasts, which drive 45% of rejections, and weak KPIs, which drive 32% of rejections. Most of those failures are preventable before submission.

Terms worth negotiating hard

A term sheet is not a formality. It's where many “successful” funding deals become painful later.

For debt, pay close attention to repayment structure, reporting obligations, covenants, security, personal guarantees, review clauses, and what constitutes default. For equity, focus on valuation, board rights, liquidation preferences, anti-dilution language, founder vesting, and reserved matters.

Red flag: If a lender's reporting covenant requires numbers you don't currently produce reliably, you may be agreeing to future stress rather than present funding.

Don't negotiate only on price. Negotiate on flexibility, timing, reporting burden, and what happens when trading is merely okay instead of perfect.

Questions founders should ask before signing

Use questions that flush out operational reality:

What information must we deliver each month or quarter?

What happens if performance dips temporarily?

Can covenants be reset if business conditions change?

What approvals are needed for major decisions?

What are the practical triggers for review or default?

Good funders answer these plainly. Poor ones hide behind broad wording and urgency.

The best negotiations are calm because the founder has options. Even if you prefer one funder, keep another conversation alive long enough to test terms. Desperation weakens negotiation. Preparation strengthens it.

Steward Your Funds for Sustainable Growth

The funding event gets attention. The months after it decide whether the capital helps.

A business that receives new money without stronger governance usually gets busier, not better. More stock arrives. More people are hired. More software is added. The founder feels relief for a moment, then discovers the cash still moves unpredictably because the underlying controls never improved.

Set a reporting rhythm immediately

As soon as funds land, lock in a cadence for management reporting. Monthly is the minimum for most growing businesses. You need current P&L, balance sheet, cash flow, aged debtors, aged creditors, and a small KPI set tied to the original funding case.

That reporting rhythm is not for the funder alone. It's for management. It tells you whether the capital is doing the job it was meant to do.

For a useful framework, this guide to business performance indicators is a strong reference point for what to track consistently.

Use capital for throughput not noise

Capital should remove bottlenecks that improve cash generation. It shouldn't subsidize poor habits.

That means asking operational questions every month:

Did the stock purchase improve sell-through or just increase holdings?

Did the hire lift capacity or create management drag?

Did the marketing spend convert into profitable customers or vanity activity?

Did collections improve after process changes, or are debtors still carrying the business?

The best use of funding is to make the business less dependent on future funding.

Keep funders informed before they need to ask. When results are on track, share them. When conditions shift, explain the cause, the response, and the revised forecast early. That builds trust. Trust lowers friction in future conversations, whether you need covenant flexibility, a top-up facility, or a later round.

Funding works best when it supports a disciplined operating machine. If the business learns to convert capital into margin, cash, and management clarity, future funding gets easier. If not, every raise becomes harder than the last.

If you want help getting your business fundable before you approach lenders, investors, or grant programs, Nexist helps Australian founders tighten cash flow, build decision-grade forecasts, and turn messy operations into a finance engine that supports growth.

funding the business, business finance australia, sme funding, startup funding, cash flow management

" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="dSFdkJotL" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="wscNJE44G" transform="translate(0 0.129)" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="sTpjGo1tb" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="s7ffpmKOD" transform="translate(0 0.129)" width="24px"/><g d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.000006px" id="D0ecaHEcW" transform="translate(0 0)" width="24px"><path d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z" fill="rgb(55, 184, 218)" height="24.000006px" id="IPLFE6zXx" width="24px"/><path d="M 4.02 0 L 0 0 L 0 12.092 L 4.02 12.092 Z" fill="rgb(255, 255, 255)" height="12.09201px" id="FWhtzAyuY" transform="translate(2.863 8.375)" width="4.02px"/><path d="M 2.274 0 C 0.899 0 0 0.904 0 2.089 C 0 3.25 0.871 4.179 2.221 4.179 L 2.247 4.179 C 3.648 4.179 4.521 3.25 4.521 2.089 C 4.495 0.904 3.649 0 2.274 0 Z" fill="rgb(255, 255, 255)" height="4.17876px" id="VmOsKv4kO" transform="translate(2.625 2.545)" width="4.52095px"/><path d="M 7.641 0 C 5.509 0 4.554 1.173 4.019 1.996 L 4.019 0.284 L 0 0.284 C 0.053 1.419 0 12.376 0 12.376 L 4.019 12.376 L 4.019 5.623 C 4.019 5.262 4.045 4.9 4.151 4.642 C 4.442 3.92 5.103 3.172 6.214 3.172 C 7.667 3.172 8.25 4.282 8.25 5.907 L 8.25 12.376 L 12.269 12.376 L 12.269 5.442 C 12.269 1.728 10.286 0 7.641 0 Z" fill="rgb(255, 255, 255)" height="12.37626px" id="n1XUbhaq0" transform="translate(9.105 8.09)" width="12.268830000000001px"/></g></g></g></g></svg>)