Strategic and Financial Planning: A Founder's Guide 2026

Master strategic and financial planning with our guide for Australian founders. Learn to link strategy to cash flow, set KPIs, and avoid common pitfalls.

Ansh Malhotra

Your strategic plan probably exists in one of three places right now. It's in a slide deck from your last planning day, in a spreadsheet no one has opened for weeks, or in your head while you spend most of your time chasing invoices, stock issues, payroll questions, and urgent decisions.

That's the problem with most advice on strategic and financial planning. It treats strategy as a quarterly workshop and finance as historical reporting. Founders don't run businesses in neat categories like that. You make decisions with whatever cash is in the bank, whatever staff capacity is left this week, and whatever surprises landed this morning.

For Australian SMEs, useful planning has to do two things at once. It has to protect the business now, and it has to create enough clarity for the next move. If it can't do both, it becomes admin. If it can do both, it becomes a management system.

Table of Contents

Why Your Business Plan Is Gathering Dust

Most business plans gather dust for a simple reason. They were written at the altitude of goals, but your business is run at the altitude of cash.

The plan says expand, hire, launch, improve margins, or enter a new market. The week says chase debtors, cover wages, approve supplier payments, answer a staff issue, and work out why sales converted but cash still feels tight. Those are not separate worlds. They're the same business viewed from different distances.

That disconnect isn't just your experience. Existing strategic financial planning material often focuses on evaluation, capital planning, scenario analysis, risk assessment, and performance metrics, but offers minimal guidance on how Australian SMEs should turn those ideas into day-to-day execution, as noted in this discussion of strategic financial capital planning gaps.

Strategy fails when it has no operating mechanism

A founder usually doesn't need more theory. You need a way to answer questions like:

Can we afford this hire now: or do we need collections to improve first?

Is growth helping: or is it trapping more cash in stock and receivables?

Are margins healthy: or are discounts, rework, freight, and wastage eating them?

What happens if sales soften: for a few weeks while fixed costs stay put?

If the plan can't answer those questions, it isn't a plan. It's a wish list.

Practical rule: A strategy only becomes real when someone can see its effect on cash, workload, and timing this week.

What works instead

Useful strategic and financial planning for SMEs has a shorter feedback loop. It connects vision to a few live numbers, assigns owners, sets a review cadence, and forces trade-offs.

That means less time spent polishing annual budgets and more time spent managing the business as it operates. Weekly cash visibility. Monthly scenario review. Clear triggers for when to slow spending, push collections, adjust pricing, or delay hiring.

The shift is small but important. Stop treating the plan as a document. Start treating it as an operating rhythm.

Connecting Your Vision to Your Bank Account

A strategic goal without a financial mechanism behind it is like planning a road trip by choosing the destination and ignoring the fuel gauge. You might still leave the driveway. You won't stay in control for long.

If your goal is market expansion, the finance questions come first. How much working capital will it absorb. What happens to debtor days. Do you need more stock on hand. Will payroll rise before revenue catches up. Which costs are fixed, and which can be staged?

The external environment makes this even sharper. The Reserve Bank of Australia lifted the cash rate target from 0.10% in April 2022 to 4.35% by November 2023, the highest level in 12 years, before holding steady through 2024 to 2025. That rise materially increased borrowing costs and made forward planning more valuable for SMEs, particularly around receivables, inventory turns, payroll timing, debt serviceability, and liquidity, according to this piece on financial data points that inform business strategy.

Your numbers are a live dashboard

Founders often look at reports as if they're a scorecard for the month that just ended. That's too late. In practice, financial data is a live feedback loop for strategic decisions already in motion.

A few examples make it obvious:

Expansion needs cash before it produces cash.

Hiring changes your fixed cost base immediately.

Discounting might help revenue and hurt liquidity if margin falls.

Buying more stock can make the P&L look promising while the bank account tightens.

That's why a founder needs both altitude and instrumentation. If you're tightening collections and payment timing, practical resources on how to improve your business cash flow can help sharpen the day-to-day side of the plan.

Good planning connects business and owner decisions

In smaller businesses, company planning and owner decision-making often bleed together. The business might support a family, personal debt commitments, or a long-term wealth objective. That overlap is one reason strategic planning gets messy.

A clearer link between business cash, personal exposure, and long-term objectives often helps founders make better trade-offs. That's where topics like private wealth advisor support can become relevant, especially when you're deciding how much risk the business should carry versus how much flexibility the owner needs.

When finance is treated as reporting, strategy drifts. When finance is used as a decision tool, strategy gets sharper.

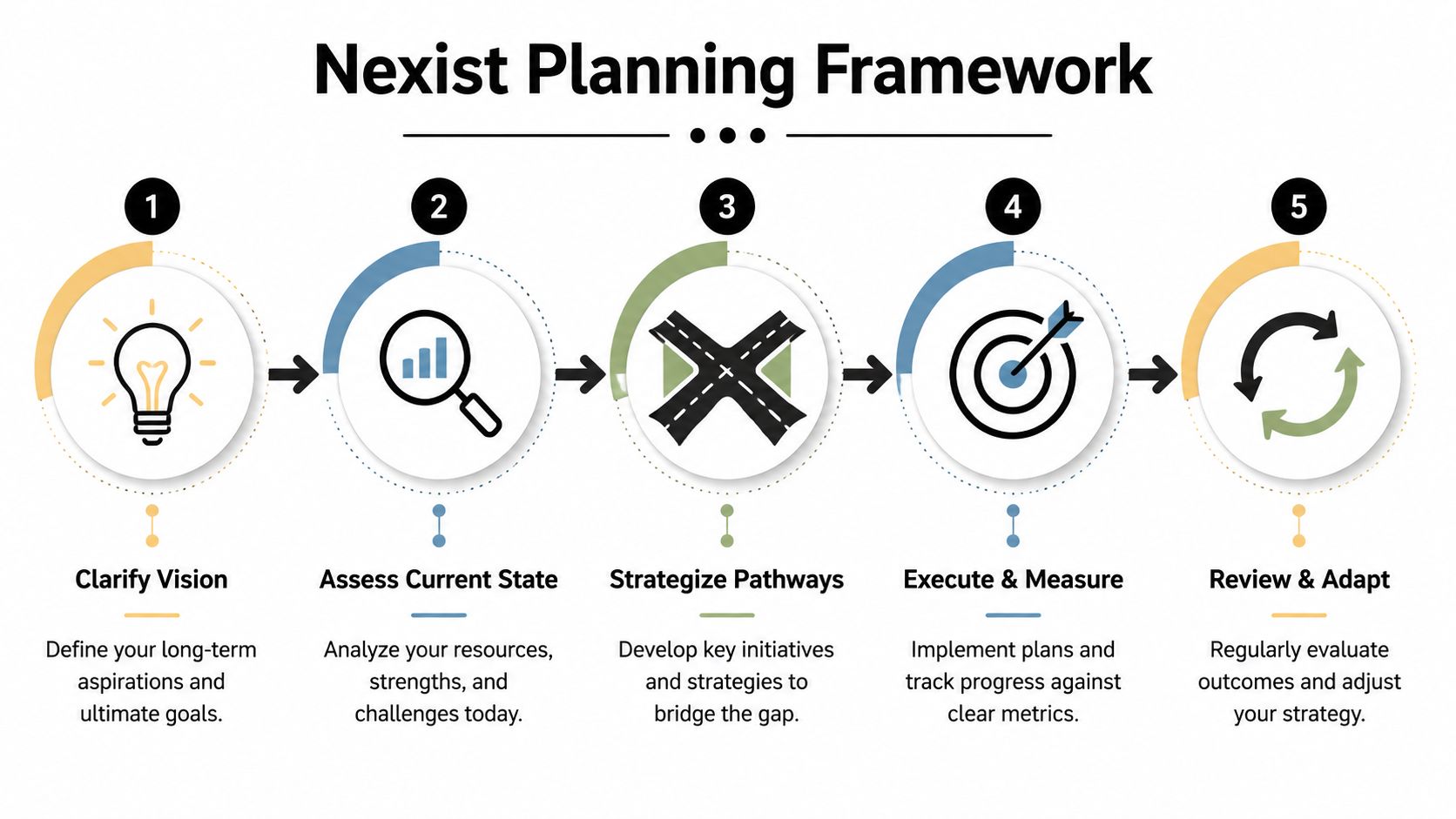

A Practical Framework for Growth and Clarity

The right framework for strategic and financial planning should be usable on a busy Wednesday, not just at an offsite. If it takes too long to update, requires too many reports, or depends on one person remembering everything, it won't last.

This is the structure that works in practice for many SMEs.

Start with decisions not documents

First, define a small number of objectives that force choices. “Grow” is vague. “Open a new channel without creating a cash squeeze” is a decision framework. “Improve margin quality before adding headcount” is another.

Then replace the static annual budget with a rolling forecast. Annual budgets tend to become fiction the moment trading conditions shift. A rolling forecast keeps the next few months visible and gives you room to react before pressure becomes a crisis.

The founder's working set usually needs five connected pieces:

Clear objectives tied to an operating outcome, not a slogan.

A rolling forecast that updates as trading changes.

A short KPI set that reflects cash, margin, and execution.

A 13-week cash view for near-term control.

Simple scenario plans for upside, base case, and pressure case.

Choose metrics that change behaviour

A good KPI should make someone act differently. If it only creates commentary, it's noise.

One of the most useful examples is operating cash flow relative to current liabilities. NetSuite describes the operating cash flow ratio as operating cash flow divided by current liabilities and notes that it measures whether the business can pay short-term liabilities from cash generated by operations. In practice, above 1.0 means operating cash generation is sufficient to cover current liabilities, while below 1.0 points to a working-capital squeeze, as outlined in this explanation of financial KPIs and metrics.

That matters because it cuts through vanity. A business can report profit and still run short of usable cash. When this ratio weakens, you don't need abstract debate. You need to inspect collections, stock, payment timing, and cost commitments.

A focused KPI set often includes:

Operating cash flow ratio: Tests whether operations are funding near-term obligations.

Gross margin by line or job: Shows where volume is disguising weak economics.

Receivables ageing: Flags where sales are not converting to cash fast enough.

Forward payroll and supplier commitments: Keeps short-term obligations visible.

Forecast versus actual cash movement: Shows whether the model is trustworthy.

Build review into the operating rhythm

Cadence matters more than ambition. If the business only reviews performance when something goes wrong, planning becomes reactive by default.

A simple rhythm is usually enough:

Meeting | Focus | Output |

|---|---|---|

Weekly cash review | Bank position, collections, payables, payroll, short-term risks | Immediate actions and owner assignments |

Monthly performance review | Margin, forecast updates, operating issues, hiring or spend decisions | Revised priorities |

Quarterly strategy review | Scenario testing, capacity, expansion timing, capital needs | Decision to push, pause, or reshape |

For teams that want structured support, Nexist is one option in the Australian market. It provides virtual CFO support, forecasting, KPI reporting, and hands-on implementation around cash flow, margins, and operating systems.

A strong plan doesn't remove pressure. It tells you where pressure is building early enough to act.

From Plan to Action A 90-Day Roadmap

The fastest way to kill strategic and financial planning is to turn it into a giant transformation project. Most founders don't need that. They need traction.

Start with control, then build consistency, then use the new visibility to make better decisions.

First month stop the bleeding

The first month is data triage. Don't try to perfect every report. Find the biggest cash leaks and decision blind spots.

Typical starting moves include:

Clean up receivables: Review overdue accounts, disputed invoices, and weak follow-up habits.

Check stock posture: Identify slow-moving items, over-ordering patterns, and purchasing driven by habit instead of demand.

Map fixed commitments: Payroll, rent, debt, software, vehicles, and supplier minimums.

Build a simple weekly cash view: Expected inflows, committed outflows, and risk items.

This is also the point where founders realise reporting quality matters. If the underlying information is messy, planning becomes guesswork. Practical guidance on variance analysis and reporting is useful here because it helps teams compare what was expected with what occurred, then act on the gap instead of just explaining it away.

Second month build the rhythm

The second month is about cadence and accountability. You don't need a finance department to do this well. You need a regular meeting, a short scorecard, and clarity on who owns what.

A workable weekly review might cover:

Topic | What to look for |

|---|---|

Cash position | What's cleared, what's expected, what's uncertain |

Debtors | Which accounts need contact now |

Payables | What must be paid, what can be timed |

Payroll and tax obligations | What's due soon and how it affects timing |

Sales and margin issues | Whether current work is profitable and collectible |

At this stage, keep the conversation tight. Founders often lose time because every finance meeting turns into a broad operational debate. Separate immediate cash actions from bigger strategic choices.

A short training video can help teams think more clearly about turning plans into execution:

Third month use the model to decide

By the third month, the model becomes useful beyond control. Now it can shape decisions on pricing, hiring, contractor use, purchasing, and growth timing.

Strategic and financial planning starts giving time back. Instead of the founder answering every question from scratch, the business has a way to test decisions against cash and capacity.

Don't ask whether an idea is good in theory. Ask whether the business can carry it without weakening cash, margin, or delivery.

Navigating Australian Compliance Tax and Cash Flow

Australian SMEs don't just manage customers, staff, and suppliers. They also manage timing. A business can be profitable on paper and still get pinched because tax, super, payroll, and BAS obligations land at the wrong moment.

That's why local detail matters. The Australian Bureau of Statistics reported that in June 2024 there were about 2.66 million actively trading businesses in Australia, and 98% were small businesses with fewer than 20 employees. The same ABS reporting also showed uneven survival, with 79.5% of businesses started in June 2022 still operating after one year and 62.5% after two years, as cited in this overview of statistics about strategic planning. In that environment, compliance timing isn't clerical. It's part of survival.

Where founders get caught

The usual issue isn't ignorance. It's timing mismatch.

Cash comes in unevenly. Obligations don't. BAS, GST-related remittances, superannuation, payroll obligations, and other recurring commitments can stack up while stock has already been purchased or labour has already been paid.

Common trouble spots include:

Using tax-related cash as operating cash: Money that looks available often isn't.

Hiring before understanding on-cost timing: Payroll decisions change more than wages alone.

Ignoring quarterly pressure points: Several obligations can bunch together.

Relying on the bank balance alone: It doesn't show what has already been spoken for.

For founders trying to make cleaner tax decisions, related guidance on claiming medical expenses on taxes can be useful in the right context, but business cash planning still needs its own separate structure.

How to plan around the calendar

The practical fix is operational, not theoretical.

Create a cash calendar that sits beside your trading forecast. Mark expected collections, supplier runs, payroll dates, super timing, BAS timing, debt payments, and any seasonal stock purchases. Then classify each outflow into one of three buckets:

Bucket | Meaning | Management approach |

|---|---|---|

Committed | Must be paid on time | Protect cash for it first |

Controllable | Timing can be managed | Schedule deliberately |

Strategic | Optional growth spend | Release only when cash supports it |

That simple separation stops founders from funding optional growth with cash already owed elsewhere. It also makes hiring decisions cleaner. Before adding labour, test the full timing effect on short-term cash, not just the expected contribution to revenue.

Example Scorecards and Templates for SMEs

A founder's scorecard should be brief enough to review in minutes and sharp enough to trigger action. If it grows into a reporting pack, it stops being useful.

Use one weekly scorecard and keep it visible. If a number doesn't change behaviour, remove it. For a deeper look at KPI selection, this guide to business performance indicators is a useful companion.

Example Founder's Scorecard Weekly

Metric | This Week | Target | Note |

|---|---|---|---|

Operating Cash Flow Ratio | [enter value] | Above 1.0 | Tests whether operations can cover current liabilities |

DSO | [enter value] | [set internal target] | Watch ageing by key customer group |

Cash Conversion Cycle | [enter value] | [set internal target] | Shows whether cash is getting trapped in stock or receivables |

Gross Profit Margin | [enter value] | [set internal target] | Review by product, service line, or job |

Collections Due This Week | [enter value] | [set internal target] | Focus on high-value follow-up first |

Payroll and Tax Commitments | [enter value] | On track | Make upcoming obligations visible |

Forecast vs Actual Cash Movement | [enter value] | Within tolerance | Tests forecast reliability |

A few rules keep this useful:

Review the same day each week: Don't let timing drift.

Add comments only where action is needed: Avoid writing essays beside every line.

Assign owners: Someone needs to chase, approve, escalate, or pause.

Keep trend context nearby: This week matters more when you can compare it with recent weeks.

Common Planning Mistakes That Burn Cash and Time

Most planning failures don't come from bad intentions. They come from habits that look sensible but create drag.

The usual failure points

The first mistake is the annual plan that never becomes operational. The document gets approved, but nobody links it to weekly decisions. Spending continues by habit. Hiring gets justified loosely. Margin problems appear late.

The second is chasing the wrong numbers. Revenue, pipeline, and booked work can all look healthy while cash tightens underneath. The issue usually isn't that founders don't care about cash. It's that the reporting system doesn't make cash friction visible early enough.

The third is poor information quality. If debtor reports are inconsistent, stock figures are stale, or costs sit in the wrong categories, the plan can't guide decisions properly. Work on mastering data quality helps because clean inputs make every forecast, KPI review, and planning conversation more reliable.

The plan doesn't fail in the boardroom. It fails in the handoff between data, decisions, and follow-through.

The founder bottleneck is a planning risk

The fourth mistake is treating the founder as the only person who understands the numbers. That feels efficient in the short term and becomes expensive fast.

Research cited in an article on financial-professional engagement notes that only 35 percent of Americans work with a financial professional, while many stressful financial tasks could be delegated or supported. For Australian SME founders, the more useful question isn't the US percentage itself. It's the practical one raised alongside it: how do you design support so the owner reclaims 20+ hours per week instead of getting trapped in forecasting, cash monitoring, and operational triage, as discussed in this piece on why people avoid engaging financial professionals despite stress.

That bottleneck shows up in familiar ways:

The founder approves everything: payments, pricing exceptions, hiring, purchasing.

No one else trusts the numbers: because the logic lives in the founder's head.

Planning gets delayed: because the owner is busy firefighting.

Good opportunities stall: because nobody can model the impact quickly.

The fix is to build a system, not heroics. Put reporting into a repeatable format. Give finance and ops a common language. Delegate follow-up. Escalate exceptions, not every transaction.

When strategic and financial planning works, the founder stops being the watchman for every cash movement and becomes the decision-maker for the few that matter most.

Nexist helps Australian founders turn strategic and financial planning into weekly control over cash, margins, and time. If you want a finance-first operating model with clearer forecasting, tighter KPI rhythms, and less owner bottleneck, explore Nexist.

strategic and financial planning, virtual cfo australia, cash flow management, business planning framework, sme financial strategy

" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="dSFdkJotL" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="wscNJE44G" transform="translate(0 0.129)" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="sTpjGo1tb" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="s7ffpmKOD" transform="translate(0 0.129)" width="24px"/><g d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.000006px" id="D0ecaHEcW" transform="translate(0 0)" width="24px"><path d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z" fill="rgb(55, 184, 218)" height="24.000006px" id="IPLFE6zXx" width="24px"/><path d="M 4.02 0 L 0 0 L 0 12.092 L 4.02 12.092 Z" fill="rgb(255, 255, 255)" height="12.09201px" id="FWhtzAyuY" transform="translate(2.863 8.375)" width="4.02px"/><path d="M 2.274 0 C 0.899 0 0 0.904 0 2.089 C 0 3.25 0.871 4.179 2.221 4.179 L 2.247 4.179 C 3.648 4.179 4.521 3.25 4.521 2.089 C 4.495 0.904 3.649 0 2.274 0 Z" fill="rgb(255, 255, 255)" height="4.17876px" id="VmOsKv4kO" transform="translate(2.625 2.545)" width="4.52095px"/><path d="M 7.641 0 C 5.509 0 4.554 1.173 4.019 1.996 L 4.019 0.284 L 0 0.284 C 0.053 1.419 0 12.376 0 12.376 L 4.019 12.376 L 4.019 5.623 C 4.019 5.262 4.045 4.9 4.151 4.642 C 4.442 3.92 5.103 3.172 6.214 3.172 C 7.667 3.172 8.25 4.282 8.25 5.907 L 8.25 12.376 L 12.269 12.376 L 12.269 5.442 C 12.269 1.728 10.286 0 7.641 0 Z" fill="rgb(255, 255, 255)" height="12.37626px" id="n1XUbhaq0" transform="translate(9.105 8.09)" width="12.268830000000001px"/></g></g></g></g></svg>)