Tax Planning Strategies for AU SMEs in 2026

Unlock powerful tax planning strategies for your Australian SME. Our 2026 guide covers entity structures, depreciation, and cash flow to boost your bottom line.

Ansh Malhotra

Revenue is up. The bank balance isn't.

That's the situation many Australian founders hit around year-end. Sales looked strong, the P&L said the business was profitable, and then the tax estimate landed with perfect timing, right when stock had to be reordered, wages were due, and debtors were taking too long to pay. On paper, the business was doing well. In cash terms, it felt tight.

That disconnect usually isn't a tax problem alone. It's a planning problem. Most owners still treat tax as something to deal with after the year is effectively over, when the only remaining conversation is how much is owed and when it has to be paid. By then, the useful decisions have already passed.

Good tax planning strategies change that. They don't rely on gimmicks or aggressive positions. They align structure, timing, profit extraction, and compliance so the business keeps more usable cash at the moments it matters most. That's what founders practically need. Not a theoretical tax saving, but more room to fund inventory, cover payroll, invest in equipment, and avoid the panic that comes from a profitable business running short on liquidity.

If you want a broader perspective on how business owners can build wealth through tax strategies, it helps to think beyond deductions and look at how every tax choice affects retained cash, personal income, and future flexibility.

Table of Contents

Your Introduction to Strategic Tax Planning

A founder can finish June feeling successful and still start July under pressure. The reason is simple. Revenue doesn't pay tax. Cash does.

Strategic tax planning starts when you stop asking, “How do I reduce tax at the end of the year?” and start asking, “How do I run the business so tax, profit, and cash move together?” That shift changes the quality of decisions. It affects when you buy equipment, how you take money out of the business, whether your structure still fits, and how much working capital stays available.

Many owners only see tax through the compliance lens. BAS gets lodged. payroll gets processed. accounts go to the accountant. return gets filed. Those jobs matter, but they don't create strategy by themselves. Compliance records what happened. Planning influences what happens next.

Practical rule: If a tax move improves the return but leaves the business short of cash for wages, stock, or supplier payments, it isn't a strong strategy.

The strongest tax planning strategies are usually boring in the best way. They involve cleaner entity design, better forecasting, disciplined timing of purchases, and a deliberate approach to salary, dividends, and retained earnings. None of that sounds glamorous. All of it improves control.

Founders who get this right usually become less reactive around year-end. They're not scrambling for extra deductions in the final week. They've already mapped profit, expected tax, planned distributions, and major spending decisions well before the deadline pressure arrives.

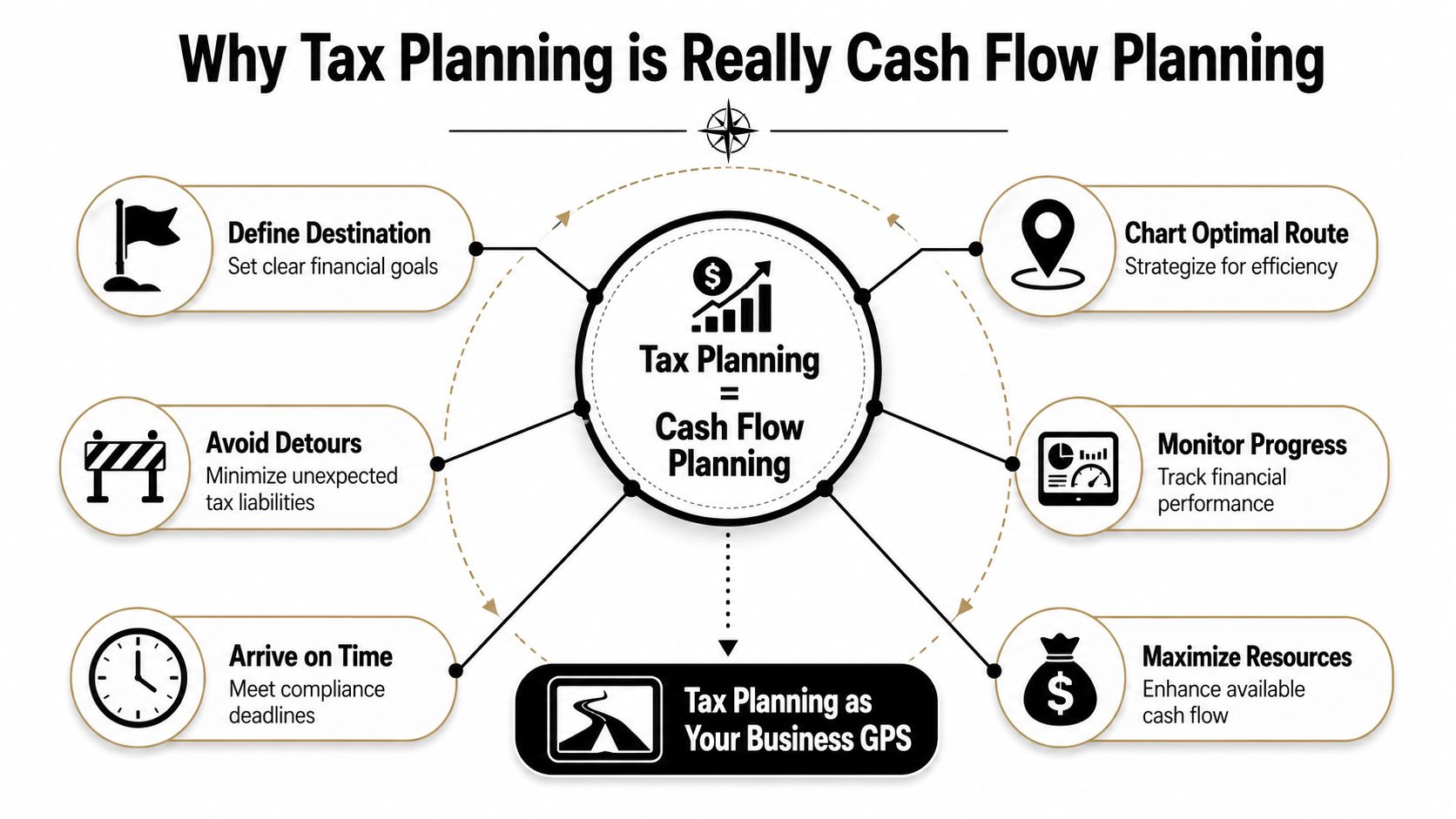

Why Tax Planning is Really Cash Flow Planning

Tax planning is often described as a way to reduce tax. That's too narrow. In practice, it's a way to decide when cash leaves the business, how much stays inside it, and whether financial pressure shows up at the worst possible moment.

Tax compliance looks backwards

Think of tax compliance as the rear-view mirror. It tells you what already happened. Tax planning is the GPS. It helps you choose the route before you're stuck in traffic.

That distinction matters because the ATO's 2024–25 focus on small-business compliance and rising quarterly obligations means many SMEs face liquidity stress even when they are “tax effective”. The practical issue isn't just tax owed. It's that tax timing decisions can affect near-term cash availability, especially when BAS, PAYG instalments, and super obligations stack up at the same time, as noted in this ATO small-business cash pressure discussion.

A founder can be fully compliant and still run a cash-starved business. That happens when tax gets treated as an annual event instead of an operating variable.

Cash in the bank is the better scorecard

The better question is not “Did this save tax?” It's “Did this preserve useful cash without creating a bigger problem later?”

That changes how you assess common decisions:

Bring forward a deduction: This may lower current-year taxable income and keep more cash in the business now.

Defer a purchase: This can protect liquidity if working capital is tighter than expected.

Change owner drawings: This may reduce pressure on the operating account if personal withdrawals are out of sync with business performance.

Review reporting cadence: Monthly visibility often exposes tax issues earlier than quarterly review does.

A business with a long debtor cycle or heavy stock holding needs this mindset even more. Tax may be calculated on profit, but suppliers, wages, and rent are paid from cash. If you want a practical lens for that operating pressure, it helps to understand the cash conversion cycle in a growing business.

Legal tax planning works within the rules. Tax evasion ignores them. Good advisers help you choose timing, structure, and documentation properly. They don't invent deductions or hide income.

The founders who handle tax best usually aren't obsessed with paying the least possible amount this year. They're focused on paying the right amount, at the right time, in a way the business can afford.

Foundational Strategy Your Business Structure

The biggest tax planning decision in many SMEs isn't a deduction. It's the structure the business operates through.

Structure affects tax treatment, access to profits, asset protection, compliance burden, and how cleanly you can move money between the business and the owner. If the structure is wrong, every later planning move becomes harder.

The structure decision shapes everything after it

For companies, one of the most important tax settings is the difference between the standard company tax rate of 30% and the base rate entity company tax rate of 25% for eligible smaller companies, with eligibility tied to the base rate entity rules including aggregated turnover below the legislated threshold and limits around passive income, as outlined in this discussion of Australian company tax rate planning.

That gap matters because it can materially affect after-tax profit. It also shows why structure isn't just legal packaging. It directly changes outcomes.

But tax rate alone doesn't decide the right setup. Founders also need to weigh:

Access to profits Can the owner draw money easily, or does every movement trigger salary, dividend, trust, or loan consequences?

Asset protection If the business trades in a risky environment, the separation between business liabilities and personal assets matters.

Future flexibility Will the structure still work if profits rise unevenly, new owners come in, or retained earnings build?

Australian business structure comparison

Feature | Sole Trader | Partnership | Company | Trust |

|---|---|---|---|---|

Legal separation from owner | No | No separate entity from partners in practical risk terms | Yes | Depends on trustee arrangement |

Profit extraction | Owner drawings | Partner distributions/drawings | Salary, dividends, retained earnings | Trust distributions |

Tax planning flexibility | Low | Moderate | High | High, but administration is heavier |

Asset protection | Limited | Limited | Stronger than individual ownership | Can be useful when designed well |

Best fit | Simple early-stage activity | Shared ownership with simple operations | Growth, retained profit, formal operations | Family wealth, distribution flexibility, asset planning |

The table looks neat. Reality usually isn't.

A sole trader setup can work early when revenue is modest and operations are simple. The problem comes later, when profits grow, personal risk grows with them, and the owner still treats the business account like an extension of their wallet. That makes forecasting, tax provisioning, and lender conversations harder than they need to be.

Partnerships can be workable when roles and economics are clear. They become painful when partners contribute unevenly, withdraw cash differently, or expect distributions that the business can't support.

Companies suit many operating businesses because they create cleaner separation and more options around retained earnings and owner remuneration. Trusts can offer flexibility, but only when they're administered properly. A poorly run trust creates confusion, not strategy.

What usually works and what usually does not

What works is choosing structure based on operating reality. That means looking at margins, risk, ownership, reinvestment plans, and how the owner needs to live from the business.

What doesn't work is copying another founder's setup because “their accountant said it was tax effective.” A freight operator, ecommerce brand, consultancy, and family investment vehicle don't need the same answer.

A structure should help the business hold profit, move cash legally, and protect the owner when things go wrong. If it only solves one of those, it's usually incomplete.

A useful review asks a few blunt questions:

Where does profit need to sit Inside the business for growth, or in the owner's hands for living costs?

How lumpy are earnings Stable monthly revenue needs a different extraction strategy from seasonal or project-based income.

What risks exist Trading risk, staff risk, contract risk, and debt exposure all affect the value of separation.

How often does the owner take money ad hoc Frequent informal withdrawals usually point to a structure or discipline problem.

Good tax planning strategies start here because structure is the platform. If the platform is wrong, every deduction, dividend, and distribution sits on unstable ground.

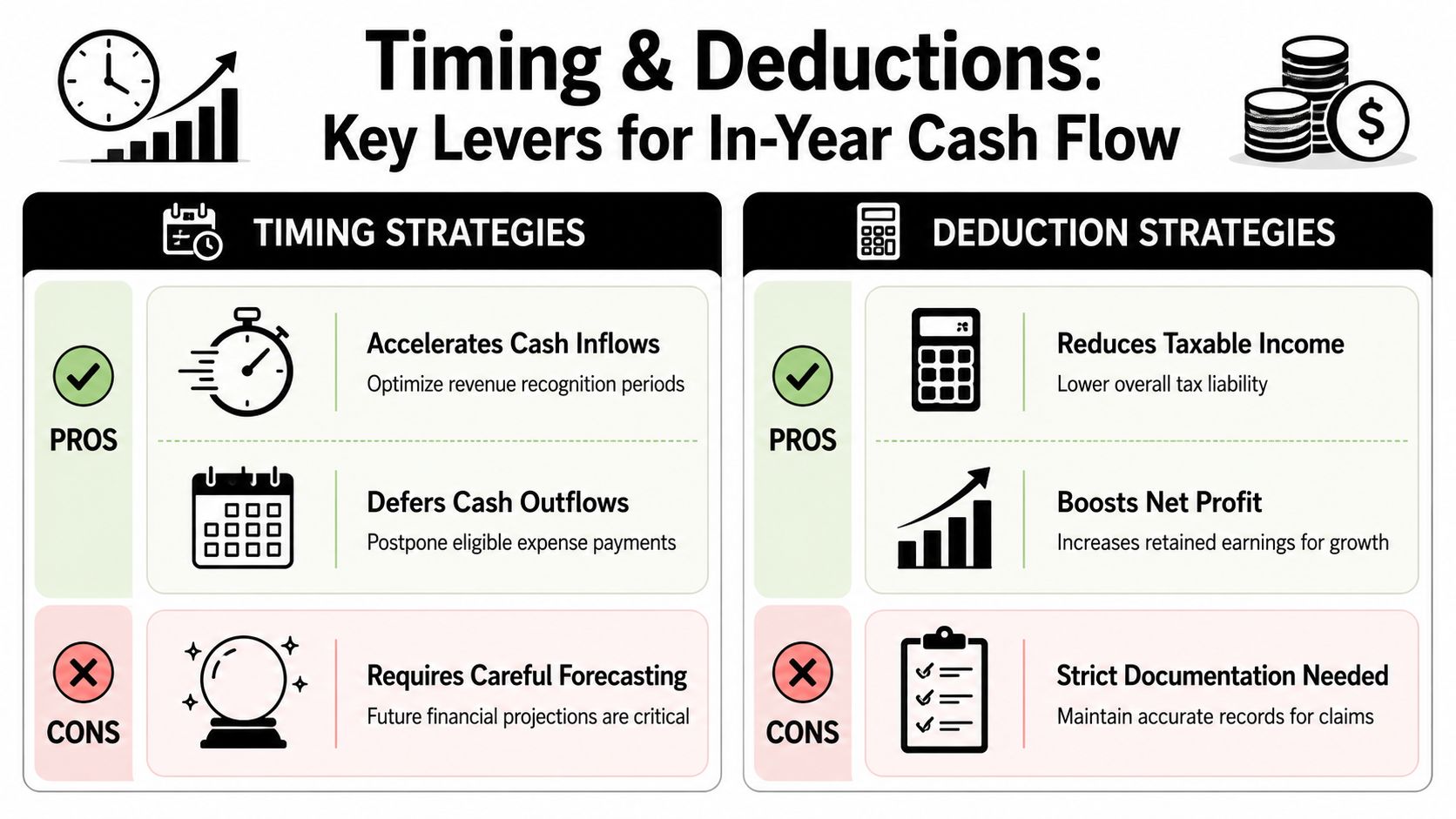

Timing and Deductions Key Levers for In-Year Cash Flow

Most practical tax planning happens through timing. Not because timing changes economics forever, but because it changes when cash leaves the business. For an SME, that can be the difference between smooth operations and an avoidable cash squeeze.

Timing changes outcomes

Founders often underestimate how much control they already have over taxable outcomes inside a normal year. The simplest levers are income timing and expense timing.

If the business expects a stronger result in one year than the next, there may be value in bringing forward legitimate expenses or delaying some income recognition where the rules allow and commercial reality supports it. If the opposite is true, preserving deductions for a later period may be smarter.

The key point is that timing decisions should follow cash logic, not just tax logic.

A few practical examples:

Prepaying necessary business costs If the expense is commercially sensible and properly documented, bringing it forward can reduce current-year taxable income.

Delaying a discretionary spend If the business needs liquidity more than it needs the deduction, waiting can be the better move.

Managing invoicing dates carefully Pushing work into the next period just to chase a tax effect can create collection risk or operational confusion. It only works when it fits the contract and the delivery schedule.

Matching stock and purchasing cycles Retailers and wholesalers often focus on margin and miss the tax effect of poorly timed buying decisions.

What doesn't work is making artificial moves with no commercial substance. If the purchase wasn't needed, the deduction doesn't make it a good decision. Spending cash to save part of that cash in tax is still spending cash.

Where the instant asset write-off matters most

Depreciation timing becomes powerful. Following the COVID-era stimulus, eligible businesses with aggregated turnover below $500 million could immediately deduct the cost of eligible depreciating assets, which reinforced how timing capital purchases can bring forward significant tax benefits and improve liquidity, as noted in this overview of instant asset write-off timing for eligible businesses.

For asset-heavy businesses, that changed behaviour for good. Founders stopped viewing equipment purchases purely as operational events and started treating them as timing decisions as well.

Under later budget measures, the instant asset write-off continued to matter because eligible businesses could deduct qualifying depreciating assets up to the legislated cap rather than spreading deductions over several years, which can lower current-year taxable income and improve cash flow. The practical lesson is simple. Capex timing matters. If you want a broader explanation of that principle, this discussion of advanced timing around depreciating assets and capex is directionally useful.

For a trades business, that might mean bringing forward a vehicle, tools, or workshop equipment when the current year is strong and the asset is needed. For ecommerce or warehousing, it could mean scanners, shelving systems, packing equipment, or other operating assets.

Key takeaway: Buy the asset because the business needs it. Then use the tax timing properly. Don't reverse that order.

A sensible capex review should ask:

Is the asset necessary now

Will it improve throughput, service, or labour efficiency

Can the business fund it without stressing working capital

Is the current year the best time to claim the deduction

Losses are only useful if you plan around them

Losses get discussed as if they're a strategy on their own. They're not. A loss is only useful when the business understands how it will use that position in future planning and how long it can carry the cash burden that created it.

For founders, the more practical issue is what a loss says about operations. Was it caused by deliberate investment, poor pricing, overstaffing, dead stock, debtor issues, or owner withdrawals that outpaced reality? Tax treatment matters, but diagnosis matters first.

A few good habits improve the quality of loss planning:

Separate one-off costs from recurring weakness Don't assume the business is fine if the loss came from a single bad decision. Fix the underlying process.

Forecast the recovery path If profit is expected to return, model how future taxable income might interact with the carried position.

Protect records early Once a business is under pressure, documentation quality often gets worse. That's the wrong time to get loose.

Keep strategy tied to cash A carried tax benefit in the future doesn't solve today's supplier pressure.

Strong tax planning strategies don't treat deductions and losses as trophies. They use them as tools inside a wider cash plan.

Advanced Strategies for Growth and Investment

Once the basics are working, tax planning shifts from defence to allocation. The question becomes how to move profit in ways that support growth, owner wealth, and staff retention without creating avoidable leakage.

Owner remuneration is a planning decision

In founder-led SMEs, choosing when to draw salary, franked dividends, or trust distributions is a key tax-planning lever because the structure of those payments can affect the timing and amount of tax paid by both the company and the owner, as explained in this guide to salary, franked dividends, and trust distribution strategy.

Many owners create problems for themselves. They mix personal spending with business cash, then ask the accountant to “sort it out later”. That usually leads to rougher outcomes than a planned remuneration approach would have delivered.

In practice, each method does a different job:

Salary Useful when the owner needs regular personal cash flow and wants discipline around PAYG and super.

Franked dividends More suitable when profits have been earned and the company is in a position to distribute them deliberately rather than casually.

Trust distributions Potentially useful where the wider ownership or family structure supports them and administration is handled properly.

What works is setting a baseline remuneration plan early, then reviewing it when profitability changes. What doesn't work is taking irregular drawings all year and hoping the legal and tax character can be fixed after the fact.

Super and reinvestment can support growth

For many owners, superannuation is underused because it feels disconnected from the operating business. That's a mistake. Used properly, it can be part of a broader remuneration and long-term wealth strategy.

The value isn't just tax treatment. It's discipline. Super contributions force owners to separate current consumption from long-term wealth building.

For those with uneven income histories, it can also be worth reviewing carry-forward concessional contribution rules and planning options before making year-end decisions. The technical rules still need confirmation with your adviser, but the broader planning principle is clear. Don't leave retirement funding as an afterthought once the business becomes profitable.

A second growth decision is whether to retain profit in the business or extract it. Retaining earnings can fund stock, systems, recruitment, and new capability. Extracting too much too early can leave the business dependent on debt or owner top-ups later.

Founders often ask how to pay less tax. The better question is how to place each dollar of profit where it creates the most long-term value.

Later in the planning cycle, some owners also use educational content to sharpen their thinking around profit extraction and reinvestment. This overview is a reasonable starting point:

Innovation needs clean records before it needs ambition

Businesses that invest in product development, process improvement, or technical experimentation often hear about the R&D Tax Incentive long before they're ready to claim anything properly.

The common failure isn't lack of innovation. It's weak evidence. Founders remember the project, but they don't maintain a clean trail of intent, activity, cost allocation, and commercial context. That makes later review difficult.

A practical approach is to treat innovation work like a governed project from day one:

Define the project clearly What problem is being solved, and what uncertainty exists?

Separate the costs Don't bury development spending inside broad overhead lines.

Keep contemporaneous records Meeting notes, test logs, design changes, and project milestones matter more than hindsight summaries.

The broader lesson is that advanced tax planning strategies only work when the underlying finance function is organised. Advanced opportunities collapse quickly if the records are weak.

Managing Compliance and Monitoring Your Plan

A tax plan that isn't monitored becomes fiction. It may look sensible in a spreadsheet, but if reporting is late, owner withdrawals are loose, or the accounting file is unreliable, the plan won't survive contact with business operations.

A plan fails when reporting is late or messy

Compliance isn't separate from strategy. It's what gives strategy traction.

For founders and owner-operated SMEs, entity structure affects not just tax outcomes but also Division 7A risk and the owner's ability to extract cash efficiently, which has become more important with recent ATO focus on compliance and trust reporting, as noted in this article on structure, cash extraction, and Division 7A considerations.

That matters because many tax problems begin as admin problems. A loan account isn't reconciled. Trust records lag. Personal expenses move through the business with weak coding. Drawings are treated casually. Months later, the business has a tax issue that looked invisible at the time.

Good monitoring usually includes:

Monthly close discipline Get the numbers finalised quickly enough that decisions still matter.

A live tax provision Don't wait until year-end to estimate exposure.

Clean separation of owner transactions If money moves between owner and entity, document why and how.

Regular compliance review BAS, super, payroll, and year-end obligations should line up with the actual operating reality.

If your team handles a heavy volume of statements, notices, and supporting files, tools that streamline tax document analysis can help reduce admin drag before information reaches your adviser.

Track tax with operating KPIs

The businesses that stay calm around tax usually monitor it the same way they monitor margin or debtors. They treat it as part of operating performance.

Useful KPI views include:

KPI | What it tells you |

|---|---|

Effective tax rate trend | Whether tax outcomes are moving as expected relative to profit |

Cash flow to taxable profit ratio | Whether accounting profit is converting into usable cash |

Owner withdrawals versus plan | Whether personal cash extraction is aligned with capacity |

BAS and PAYG forecast variance | Whether quarterly obligations are staying inside expectation |

These don't need to be complex. They need to be visible. A founder should be able to look at the dashboard and know whether the business is heading toward a controlled tax outcome or a nasty surprise.

For a broader operating checklist around reporting and obligations, this guide on tax and compliance for growing businesses is a useful reference point.

Watch the known risk areas

Some issues show up repeatedly in SME reviews:

Informal owner drawings These often create confusion around loans, wages, and distributions.

Late trust decisions Flexibility disappears when documentation lags the financial reality.

Poor evidence for deductions A legitimate expense with weak support becomes harder to defend.

Mismatch between GST, profit, and cash Businesses can report acceptable profit while still struggling with remittance pressure.

The cleaner the records, the more options you keep. Messy books don't just increase risk. They reduce strategic flexibility.

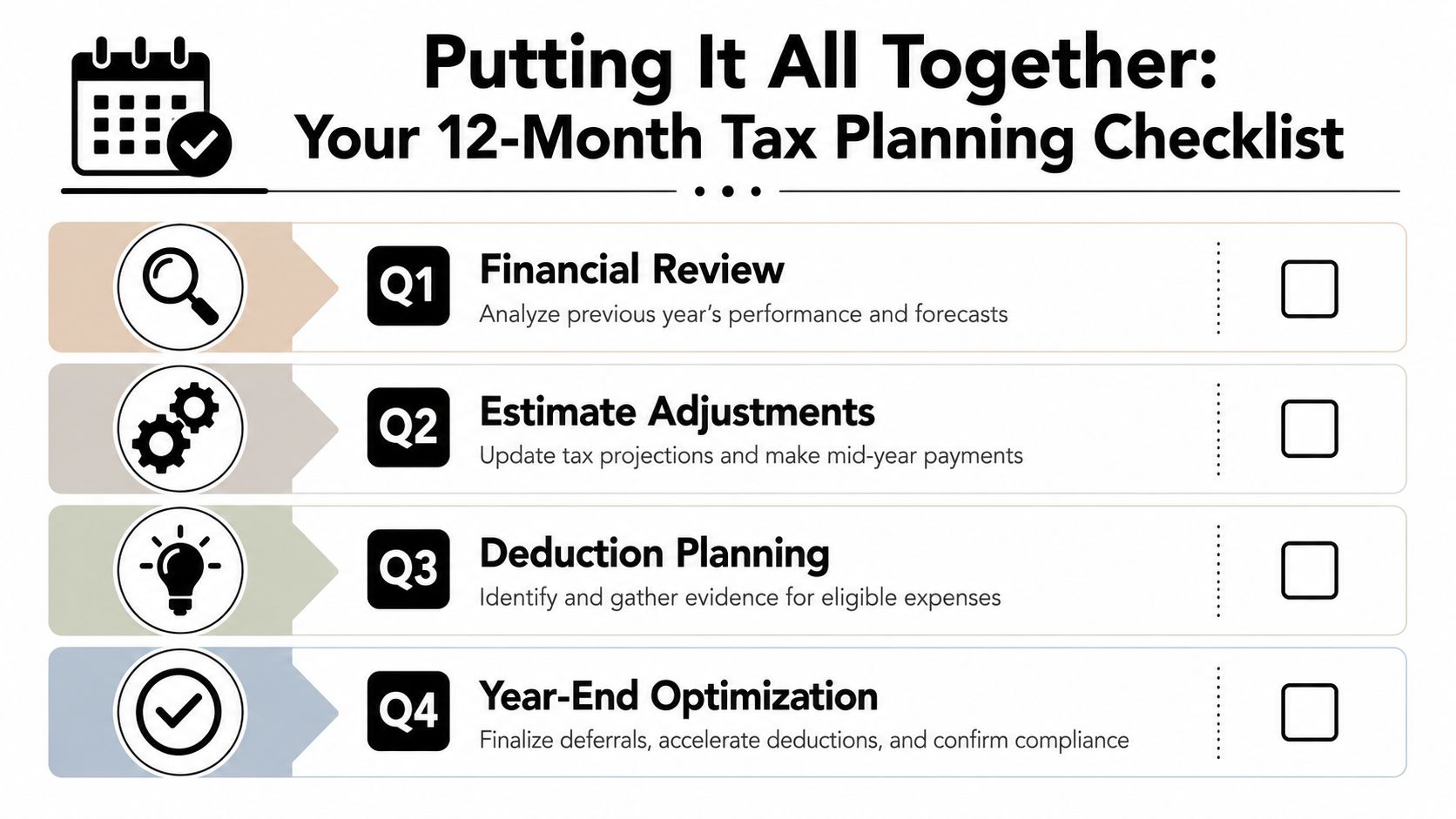

Putting It All Together A Checklist and Case Studies

The best tax planning strategies don't live in a June sprint. They sit inside a rhythm. Founders who build that rhythm usually make calmer decisions because they aren't trying to solve a full year of problems in the final days.

A practical annual checklist

A simple annual cycle often works better than an elaborate plan no one follows.

First quarter Review the prior year properly. Compare actual profit, taxable position, and cash conversion. Rebuild the forecast using current trading conditions, not last year's assumptions.

Second quarter Revisit tax provisioning and owner remuneration. If the year is tracking above or below plan, adjust early rather than preserving a false baseline.

Third quarter Review deductible spending, capital needs, and record quality. This is the time to identify weak documentation while there's still time to fix it.

Fourth quarter Finalise timing decisions, confirm any planned profit extraction, and make sure compliance paperwork supports the strategy already chosen.

Founders running cloud accounting stacks often find it easier to keep this cycle moving when their software environment is stable and accessible, especially across advisers and internal staff. For firms using specialist tax applications, Cloudvara's tax software hosting is one option to evaluate.

Case study one inventory pressure and capex timing

An ecommerce operator enters the final quarter with solid sales but strained working capital. Inventory is moving, yet cash is trapped in stock and receivables. The owner had planned to buy warehouse equipment but hadn't decided when.

Instead of waiting until after year-end, the business reviews current profitability, confirms the equipment is needed, and aligns the purchase with the stronger trading period. The deduction timing improves the current-year tax position, but the primary benefit is operational. The new equipment supports fulfilment efficiency and helps the team process volume with less friction.

The wrong move in that situation would have been buying several discretionary items at once exclusively to chase deductions. That would have weakened liquidity further.

Case study two service income and structure cleanup

A service business owner has been taking money from the business inconsistently for years. Personal expenses have passed through the trading entity, and the owner still thinks in terms of “drawings” even though the business has outgrown that mindset.

The review finds two issues. First, cash extraction has no plan. Second, the structure no longer matches the size and risk of the operation. The solution isn't a magic deduction. It's a cleanup. The owner shifts to a more deliberate remuneration approach, separates personal spending from business activity, and formalises how profit can be retained or distributed.

The tax benefit matters, but the larger gain is control. Forecasting improves. Compliance risk falls. The owner stops treating tax as a surprise and starts treating it as part of financial management.

What both examples have in common is this: the win didn't come from obscure tax knowledge. It came from timing, structure, discipline, and better cash awareness.

If you want a clearer view of where cash is leaking, how your current tax settings affect working capital, and which changes would move the needle, Nexist offers a practical starting point. A Business Scorecard can help you identify pressure points across tax, margins, inventory, receivables, and owner withdrawals so you can make sharper decisions before year-end forces them on you.

tax planning strategies, sme tax australia, business tax, cash flow management, virtual cfo

" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="dSFdkJotL" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="wscNJE44G" transform="translate(0 0.129)" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="sTpjGo1tb" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="s7ffpmKOD" transform="translate(0 0.129)" width="24px"/><g d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.000006px" id="D0ecaHEcW" transform="translate(0 0)" width="24px"><path d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z" fill="rgb(55, 184, 218)" height="24.000006px" id="IPLFE6zXx" width="24px"/><path d="M 4.02 0 L 0 0 L 0 12.092 L 4.02 12.092 Z" fill="rgb(255, 255, 255)" height="12.09201px" id="FWhtzAyuY" transform="translate(2.863 8.375)" width="4.02px"/><path d="M 2.274 0 C 0.899 0 0 0.904 0 2.089 C 0 3.25 0.871 4.179 2.221 4.179 L 2.247 4.179 C 3.648 4.179 4.521 3.25 4.521 2.089 C 4.495 0.904 3.649 0 2.274 0 Z" fill="rgb(255, 255, 255)" height="4.17876px" id="VmOsKv4kO" transform="translate(2.625 2.545)" width="4.52095px"/><path d="M 7.641 0 C 5.509 0 4.554 1.173 4.019 1.996 L 4.019 0.284 L 0 0.284 C 0.053 1.419 0 12.376 0 12.376 L 4.019 12.376 L 4.019 5.623 C 4.019 5.262 4.045 4.9 4.151 4.642 C 4.442 3.92 5.103 3.172 6.214 3.172 C 7.667 3.172 8.25 4.282 8.25 5.907 L 8.25 12.376 L 12.269 12.376 L 12.269 5.442 C 12.269 1.728 10.286 0 7.641 0 Z" fill="rgb(255, 255, 255)" height="12.37626px" id="n1XUbhaq0" transform="translate(9.105 8.09)" width="12.268830000000001px"/></g></g></g></g></svg>)