Maximize Super with Carry Forward Concessional Contributions

Boost super with carry forward concessional contributions. Founders' guide: eligibility, ATO rules, & strategic tax planning for 2026 in Australia.

Ansh Malhotra

A lot of founders only notice super when cash flow finally loosens up.

You spend years keeping the business alive, paying suppliers, covering payroll, and taking whatever mix of salary, director fees, or profit distributions makes sense at the time. Then a better year lands. Margins improve, a large invoice clears, or you realise you can finally put serious money aside. That's usually when the question appears: have I missed the window to build super tax-effectively?

In many cases, no. Carry forward concessional contributions can give business owners a second chance to use contribution room they didn't have the cash flow or tax planning headspace to use earlier. For founders with uneven income, that matters more than it does for salaried employees on a fixed package. Your good years and lean years rarely line up neatly.

Before you move money, get organised. I often tell owners to map cash commitments, personal drawings, and retirement funding side by side. A simple planning worksheet like ReceiptsAI personal finance templates can help you see whether a large super contribution fits your broader liquidity plan instead of becoming another rushed EOFY decision.

Table of Contents

Unlock a Hidden Superannuation Tax Advantage

A familiar founder scenario looks like this. For several years, you keep concessional contributions modest because the business needs every available dollar. Then a stronger year arrives. Maybe the company pays you a larger salary, you invoice director fees from a separate structure, or you receive a lump-sum distribution after a profitable period. Your taxable income rises quickly, but your super settings still reflect the lean years.

That gap is where this strategy becomes useful.

Carry forward concessional contributions let you revisit missed contribution capacity from prior years and use it in a later year when cash flow and taxable income can support it. For founders, that's more than a technical rule. It's a planning lever. It can help convert an unusually profitable year into a long-term wealth move rather than a larger personal tax bill.

Practical rule: The best time to think about this isn't after your accountant has finalised everything in late June. It's when you can already see a profit spike forming.

What works is using the rule when three things line up: taxable income is meaningfully higher than usual, the business can release cash without strain, and your super position still leaves the door open. What doesn't work is treating it as a reflex EOFY transfer with no check on timing, cap usage, or liquidity.

Founders also have more moving parts than employees. Your concessional contribution strategy may need to account for employer contributions, personal deductible contributions, salary sacrifice, and the tax impact of income that arrives unevenly. That complexity is exactly why this can be powerful. It's also why careless execution creates avoidable mistakes.

Why founders should care

A standard annual cap can feel restrictive when income is lumpy. The carry-forward rules change that by rewarding years when you underused your cap and letting you apply those unused amounts later, if you qualify.

That makes the rule particularly relevant when:

A profit distribution lands late in the year and you want a lawful, tax-aware way to redirect part of that gain.

Director fees increase because the company has matured and can finally pay you properly.

A one-off business event happens, such as a sale of an asset or an unusually strong trading period.

You delayed retirement planning while reinvesting in stock, staff, marketing, or systems.

The strategic value isn't just tax. It's flexibility. Founders rarely have smooth compensation patterns, so a mechanism built around unused prior-year capacity fits real business life better than one built for a steady payslip.

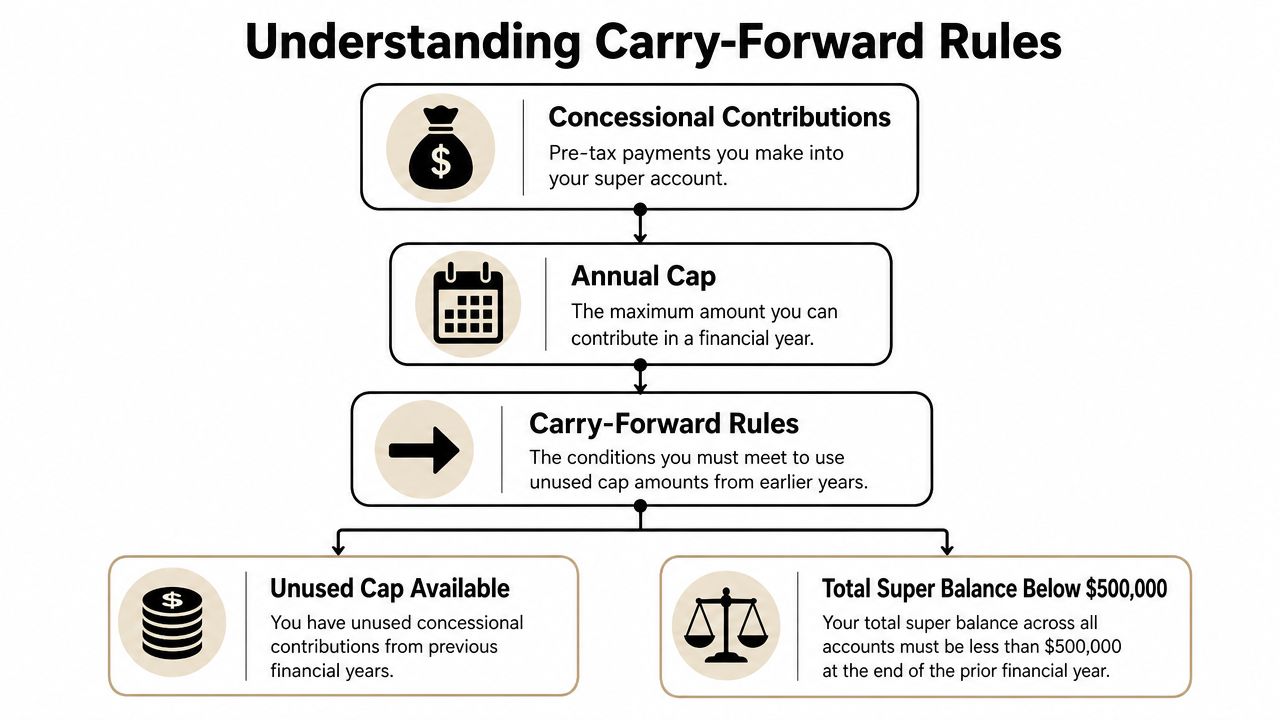

Understanding the Carry-Forward Contribution Rules

The simplest way to think about this rule is like unused mobile data rolling forward. If you didn't fully use your concessional contribution cap in earlier years, some of that unused amount can still be available later.

But this isn't casual rollover. It's tightly controlled by the ATO.

The ATO describes carry-forward concessional contributions as a five-year rolling cap release mechanism. Unused concessional cap amounts from up to the previous five financial years can be added to the current year's cap, the oldest unused amounts are applied first, and amounts expire after five years. Eligibility depends on two hard thresholds: your total super balance must be less than $500,000 at 30 June of the previous financial year, and you must have unused concessional cap amounts available from prior years. If your balance breaches that threshold at the relevant 30 June, you lose access even if the balance later falls below it, according to the ATO guidance on concessional contribution caps.

Why founders should care

A founder's income pattern often creates unused cap in weaker years, then capacity to contribute in stronger years. That's why this rule is unusually useful for owner-managers compared with people on a fixed salary.

If your earlier focus was business growth, debt reduction, inventory, or staff, you may have legitimate unused cap sitting there. The rule gives you a chance to catch up without being boxed into a single year's standard cap.

That said, the rule is binary on eligibility. A strong balance sheet in your business does not matter. A later market dip does not rescue a failed balance test. What matters is whether your personal total super balance was under the threshold on the relevant 30 June and whether unused amounts exist.

The two gates you must pass

There are only two gates, but each one matters.

Unused cap must exist. If you already used your concessional cap in prior years, there's nothing to carry forward.

Your balance must be under the threshold at the right date. The test is tied to the prior 30 June, not the day you decide to contribute.

Founders often get the timing wrong. They look at today's super balance, when the rule looks at the balance at the prior 30 June.

A practical way to approach this is to treat carry forward concessional contributions as a capacity test, not a general entitlement. Don't assume you can use it just because you had lower contributions in the past. Confirm both conditions before any money moves.

How to Check Your Eligibility and Unused Cap

This is one of the more useful parts of the system. You don't have to estimate from memory or hunt through old payroll files first. The ATO records give you a direct starting point.

Australian guidance notes that the carry-forward system uses a rolling five-year window that first became available from the 2018–19 financial year, so unused concessional amounts can expire after five financial years if not used. It also shows that myGov and ATO records display both the total unused carry-forward amount and the historical concessional contributions used to calculate it. The guidance gives a simple example: if someone contributed $25,000 in a year when the cap was $30,000, they would create a $5,000 unused amount that could be added to a future year's cap, subject to the balance test. That detail is set out in AJG's explanation of carry-forward concessional contributions.

Where to look inside myGov and ATO

Use the online records before you ask your accountant to model anything. You want the ATO's view of your data first.

Log into myGov and open the linked ATO service.

Go to the super area and look for contribution and carry-forward information.

Find the unused concessional cap view. This should show the total amount available and the historical years behind it.

Check the total super balance figure relevant to the prior 30 June.

Save a copy or screenshot before planning the contribution, especially if multiple advisers are involved.

This matters for founders because your income and contribution profile may include several moving parts. Employer contributions from one entity, salary sacrifice from another arrangement, and personal deductible contributions all need to reconcile against what the ATO has recorded.

What the figures are telling you

The screen usually gives you two different planning answers.

The first is capacity. That's the unused amount available to be added to the current year's cap if you remain eligible.

The second is urgency. Because the system works on a rolling five-year window, older unused amounts can disappear if you leave them too long. For a founder who expects a high-income year soon, that can affect whether you act now or wait.

Use the records to ask better questions:

Is there enough unused cap to make a meaningful contribution this year?

Are older amounts close to expiring?

Does my prior 30 June balance keep me eligible right now?

Have all employer contributions already been counted in the ATO view?

If the ATO record and your internal payroll or SMSF records don't line up, pause. Reconcile first, contribute second.

For business owners, that discipline matters more than speed. The rule is measurable. That's an advantage if you use the ATO data as the source of truth.

Calculating and Making Your Catch-Up Contributions

Founders usually want the same answer: how much can I put in, and what's the cleanest way to do it?

The calculation starts with the current year's concessional cap, then adds any usable unused cap from prior years. The cap was $27,500 in earlier recent years, increased to $30,000 for both 2024–25 and 2025–26, and is scheduled to rise to $32,500 from 1 July 2026, according to Grow SMSF's carry-forward concessional contributions guide. If you qualify, that means you may be able to contribute materially more than the standard annual cap by using prior unused amounts.

A founder-style worked example

Below is a planning table in the format I use when pressure-testing a catch-up strategy. It shows how to think, not your exact entitlement. Your actual figures must come from ATO records and your contribution history.

Financial Year | Annual Cap | Concessional Contributions Made | Unused Cap for the Year | Cumulative Unused Cap Available |

|---|---|---|---|---|

2022–23 | $27,500 | Lower than cap | Difference between cap and contributions made | Accumulates if still within rolling window |

2023–24 | $27,500 | Lower than cap | Difference between cap and contributions made | Adds to prior unused amount |

2024–25 | $30,000 | Lower than cap | Difference between cap and contributions made | Adds again if eligible |

2025–26 | $30,000 | Planned current-year amount | Current cap plus usable unused amounts | Depends on prior 30 June balance |

2026–27 | $32,500 scheduled from 1 July 2026 | To be determined | Depends on actual contributions | Oldest unused amounts may expire |

The mechanics matter:

Current year cap first. Start with the ordinary concessional cap for the year you're contributing in.

Then add prior unused amounts. Only include amounts still available inside the five-year window.

Oldest amounts are used first. You don't choose the order.

Eligibility is still personal. Even if the business has a strong year, your own balance test controls access.

A founder example in plain language might look like this. You under-contributed for several years because cash was tight or you preferred to keep money in the business. This year the company can finally support a larger payment to you or on your behalf. If your prior 30 June balance keeps you eligible and the ATO shows unused cap, you may be able to make a contribution well above the standard annual cap.

That can be especially valuable when a single tax year is doing too much work. Director fees rise, profits are up, and you want to move part of that taxable income into super in a controlled way.

For business owners building a broader tax and cash flow plan, this is exactly the kind of issue a virtual chief financial officer should model early, not after the year-end scramble begins.

How to actually make the contribution

There are usually two practical routes.

Personal deductible contribution. You contribute from personal funds, then claim a deduction if you meet the requirements and submit the required notice to your fund. This approach often suits founders whose income arrives unevenly or whose remuneration structure doesn't make salary sacrifice convenient.

Salary sacrifice or employer contribution pathway. This can work where payroll is stable and the business wants contributions handled through the employer side. For directors with regular pay cycles, this can simplify administration.

What works best depends on how your money moves:

Use personal deductible contributions when income is lumpy and you want to decide late in the year, based on final profitability and cash.

Use payroll-linked contributions when cash flow is stable and you want smoother execution across the year.

Avoid mixing methods carelessly if several entities or advisers are involved. It's easy to lose track of what has already counted toward the cap.

A technically valid strategy can still fail operationally if the contribution method doesn't match how the founder actually gets paid.

The arithmetic is only half the job. The other half is making sure the money arrives correctly, is classified correctly, and is documented properly.

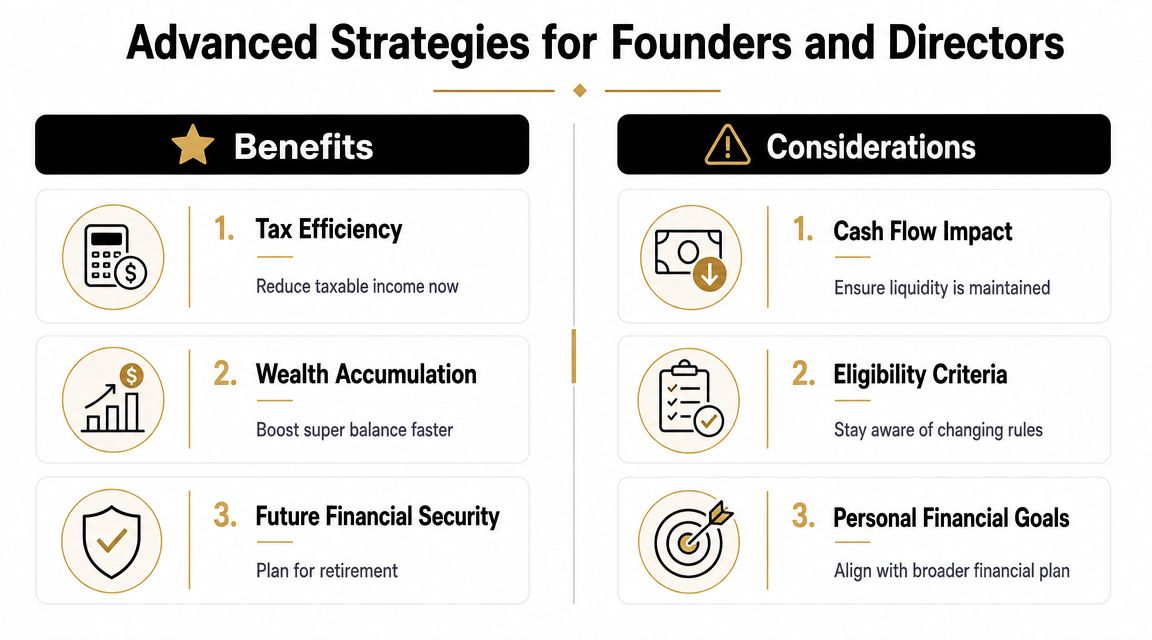

Advanced Strategies for Founders and Directors

Carry forward concessional contributions become far more valuable when you stop viewing them as a generic super top-up and start treating them as part of founder remuneration design.

A salaried employee may use the rule to tidy up retirement savings. A founder can use it to manage volatile income, convert a spike in taxable earnings into a more deliberate wealth move, and coordinate super with broader business planning.

Using carry forward in lumpy income years

Three founder scenarios show where this strategy tends to work well.

First, lump-sum profit distributions. If the business has a standout year and distributions push up personal taxable income, a catch-up concessional contribution can help reshape the personal tax outcome. The contribution won't solve a weak cash position, but in a strong year it can redirect some of the gain into a long-term structure.

Second, director fees. Some founders keep director fees modest while the business is scaling, then increase them once operations stabilise. That can create a tax spike in the year the business finally has room to pay properly. Carry-forward capacity can be useful in that first higher-income year.

Third, post-transaction or post-asset-sale planning. Founders often focus heavily on deal proceeds or business cash extraction and only later think about retirement funding. A catch-up concessional contribution can be part of the personal side of that planning if eligibility remains intact.

The key trade-off is liquidity. A contribution into super improves tax efficiency and retirement funding, but it also moves cash into a more restricted environment. That's why I rarely view this as an isolated tax move. It has to sit alongside debt, working capital, family cash needs, and business reserves.

For owners who operate across entities or are comparing payment structures in different jurisdictions, broad reading on owner remuneration can sharpen your thinking. A US-focused piece on avoiding tax messes for LLC owners is useful not because the rules are the same, but because it highlights the same strategic problem founders face everywhere: getting paid in a way that is clean, intentional, and defensible.

Where Div 293 changes the conversation

Div 293 is where many founders hesitate. Once income is high enough, the tax treatment of concessional contributions becomes less attractive than the standard super contribution tax position. But less attractive doesn't automatically mean unattractive.

The right question isn't “does Div 293 apply?” The better question is “after Div 293, is the contribution still worth making compared with taking the income personally and investing outside super?”

In many founder situations, the answer can still be yes, especially where:

Income is unusually high for one year only, which makes that year a strong candidate for catch-up contributions.

The founder wants to build concessionally taxed retirement capital rather than hold all surplus wealth outside super.

The business has enough surplus cash that the contribution won't damage operating flexibility.

What doesn't work is making the contribution purely because the cap exists. If Div 293 applies, the decision needs a proper comparison across personal cash needs, effective tax outcomes, and access to funds.

This is also where super planning starts intersecting with broader wealth-cap rules and future policy exposure. If you're modelling larger balances over time, tools that help you think through those settings, such as this Division 296 calculator resource, can be useful alongside tax advice.

A founder's best use of carry forward concessional contributions is rarely accidental. It usually sits inside a wider remuneration plan that answers four questions clearly:

Decision area | Strong approach |

|---|---|

Timing | Use high-income years, not random years |

Funding source | Match the contribution method to how you actually get paid |

Tax lens | Compare the super outcome with the personal after-tax alternative |

Cash flow | Keep business and household liquidity intact |

The founders who use this well don't chase the cap. They use the cap to support a bigger plan.

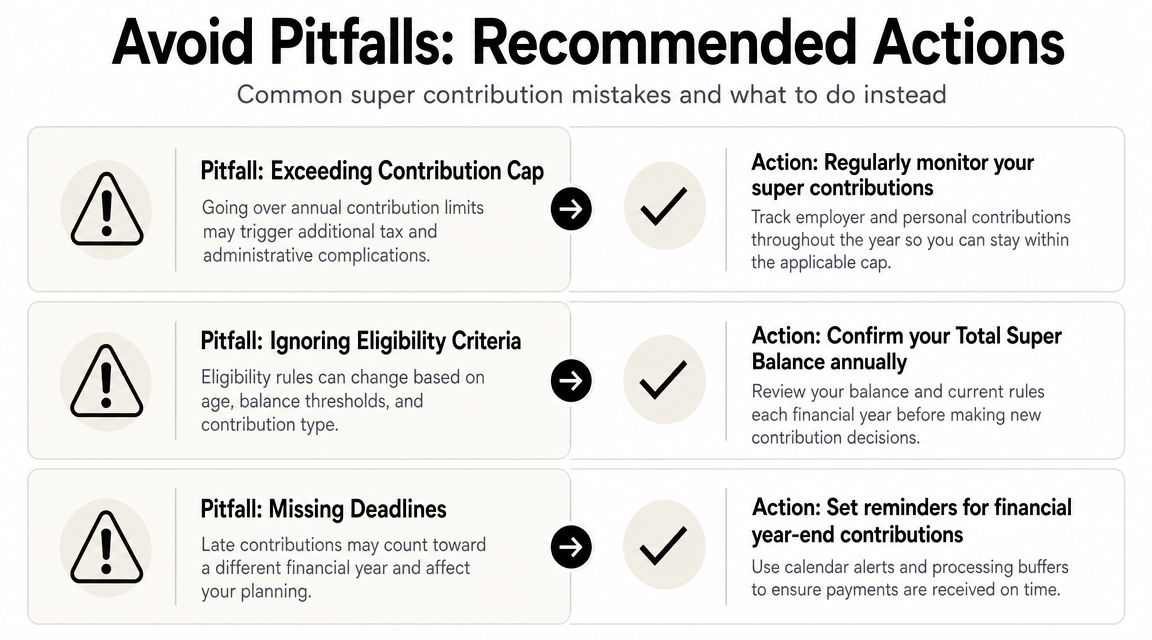

Common Pitfalls and Recommended Actions

Most mistakes with carry forward concessional contributions aren't exotic. They're ordinary execution errors made under EOFY pressure.

Mistakes that cost founders money

The first mistake is checking the wrong balance at the wrong time. Founders often look at their current super balance and assume that's enough. It isn't. The relevant eligibility date sits earlier, and getting that wrong can collapse the whole strategy.

The second is forgetting that concessional contributions are cumulative from different channels. If employer contributions, salary sacrifice, and personal deductible contributions all hit in the same year, you need one consolidated view.

The third is poor timing around payment processing. A contribution that was “intended” before year-end is not the same as one the fund receives in time. That distinction matters in practice.

Another common problem is paperwork drift. If you're using a personal deductible contribution approach, the documentation trail needs to match the strategy. A tax plan that relies on forms being lodged later can fail for completely avoidable reasons.

For founders with more complex personal structuring or larger investable wealth, it's often sensible to review super planning as one part of a bigger advisory framework rather than as a standalone tax move. That's where a broader private wealth advisor perspective can help connect super, tax, liquidity, and long-term asset decisions.

A practical action checklist

If you want to use carry forward concessional contributions properly, treat it like a short project.

Confirm the balance test early. Check the relevant prior 30 June total super balance before discussing contribution amounts.

Pull the ATO carry-forward record. Use myGov and ATO data as the baseline for unused cap availability.

Map all concessional contribution sources. Include employer amounts, payroll arrangements, and planned personal contributions.

Choose the funding path deliberately. Decide whether the contribution should come through payroll or from personal funds with a deduction strategy.

Protect liquidity. Don't fund a super contribution by weakening trading cash, supplier capacity, or household reserves.

Allow time for processing. Don't rely on last-minute transfers.

Complete the paperwork. If a notice is required, handle it properly and keep records.

The expensive mistakes usually happen when founders treat super like an afterthought. The better approach is to give it the same discipline you'd give any other capital allocation decision.

Carry forward concessional contributions can be one of the most effective super strategies available to a founder. They can also be mishandled easily. Precision matters more than enthusiasm.

If you want a sharper view of how super strategy fits into business cash flow, founder remuneration, and long-term wealth planning, Nexist can help you model the numbers before you commit capital.

carry forward concessional contributions, superannuation Australia, SME tax planning, founder finances, virtual CFO

" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="dSFdkJotL" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="wscNJE44G" transform="translate(0 0.129)" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="sTpjGo1tb" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="s7ffpmKOD" transform="translate(0 0.129)" width="24px"/><g d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.000006px" id="D0ecaHEcW" transform="translate(0 0)" width="24px"><path d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z" fill="rgb(55, 184, 218)" height="24.000006px" id="IPLFE6zXx" width="24px"/><path d="M 4.02 0 L 0 0 L 0 12.092 L 4.02 12.092 Z" fill="rgb(255, 255, 255)" height="12.09201px" id="FWhtzAyuY" transform="translate(2.863 8.375)" width="4.02px"/><path d="M 2.274 0 C 0.899 0 0 0.904 0 2.089 C 0 3.25 0.871 4.179 2.221 4.179 L 2.247 4.179 C 3.648 4.179 4.521 3.25 4.521 2.089 C 4.495 0.904 3.649 0 2.274 0 Z" fill="rgb(255, 255, 255)" height="4.17876px" id="VmOsKv4kO" transform="translate(2.625 2.545)" width="4.52095px"/><path d="M 7.641 0 C 5.509 0 4.554 1.173 4.019 1.996 L 4.019 0.284 L 0 0.284 C 0.053 1.419 0 12.376 0 12.376 L 4.019 12.376 L 4.019 5.623 C 4.019 5.262 4.045 4.9 4.151 4.642 C 4.442 3.92 5.103 3.172 6.214 3.172 C 7.667 3.172 8.25 4.282 8.25 5.907 L 8.25 12.376 L 12.269 12.376 L 12.269 5.442 C 12.269 1.728 10.286 0 7.641 0 Z" fill="rgb(255, 255, 255)" height="12.37626px" id="n1XUbhaq0" transform="translate(9.105 8.09)" width="12.268830000000001px"/></g></g></g></g></svg>)