Cash Conversion Cycle: A CFO's Guide for AU SMEs

Unlock trapped cash in your business. Learn how to calculate, benchmark, and shorten your cash conversion cycle with CFO-driven strategies for Australian SMEs.

Ansh Malhotra

Revenue is up. Sales look healthy. The P&L says the business is moving in the right direction.

But payroll is coming up, suppliers want to be paid, and the bank balance feels tight again.

That gap frustrates a lot of Australian founders because it looks like a contradiction. It isn't. In most cases, the business hasn't got a revenue problem. It has a timing problem. Cash is getting stuck between buying stock, delivering work, invoicing customers, and waiting to get paid.

The metric that exposes that timing problem is the cash conversion cycle. If you run retail, ecommerce, wholesale, manufacturing, or even a service business with WIP and debtor lag, this is one of the fastest ways to see where cash is trapped and what to fix first.

Table of Contents

Why Your Revenue Is High But Your Bank Account Is Empty

A founder launches a strong month. Orders are flowing. The team is flat out. On paper, it feels like momentum.

Then the cash crunch hits.

Stock was purchased weeks earlier. Some customer payments still haven't landed. A few large invoices are sitting in accounts receivable. Supplier terms are shorter than customer terms. The business is profitable on paper, but cash hasn't completed the journey back into the bank.

That's the core operating problem. Revenue tells you activity. Profit tells you margin. The cash conversion cycle tells you how long your money is out working before it returns.

A common founder blind spot

In practice, this usually shows up in a familiar pattern:

Stock-heavy businesses buy ahead of demand, then watch cash sit on shelves.

Project-based firms deliver work, issue invoices later, then wait again for collection.

Growing companies add more sales but create even more pressure because each sale needs funding before cash is received.

A business can grow and still feel cash-starved if operations keep stretching the time between spend and collection.

This is why experienced finance teams don't just monitor the P&L. They track the lag between outflow and inflow, then tighten the systems causing the lag.

Why systems matter more than reports

A spreadsheet can tell you you've got a problem. It won't solve late invoicing, poor stock visibility, or approval bottlenecks in payables.

Founders who want clearer visibility into cash timing inside their ERP should discover NetSuite's latest features, especially where dashboards and warehouse controls support day-to-day working capital decisions.

If your bank account feels out of sync with revenue, don't start by asking whether sales are high enough. Start by asking how long cash is taking to complete the cycle.

Understanding the Cash Conversion Cycle

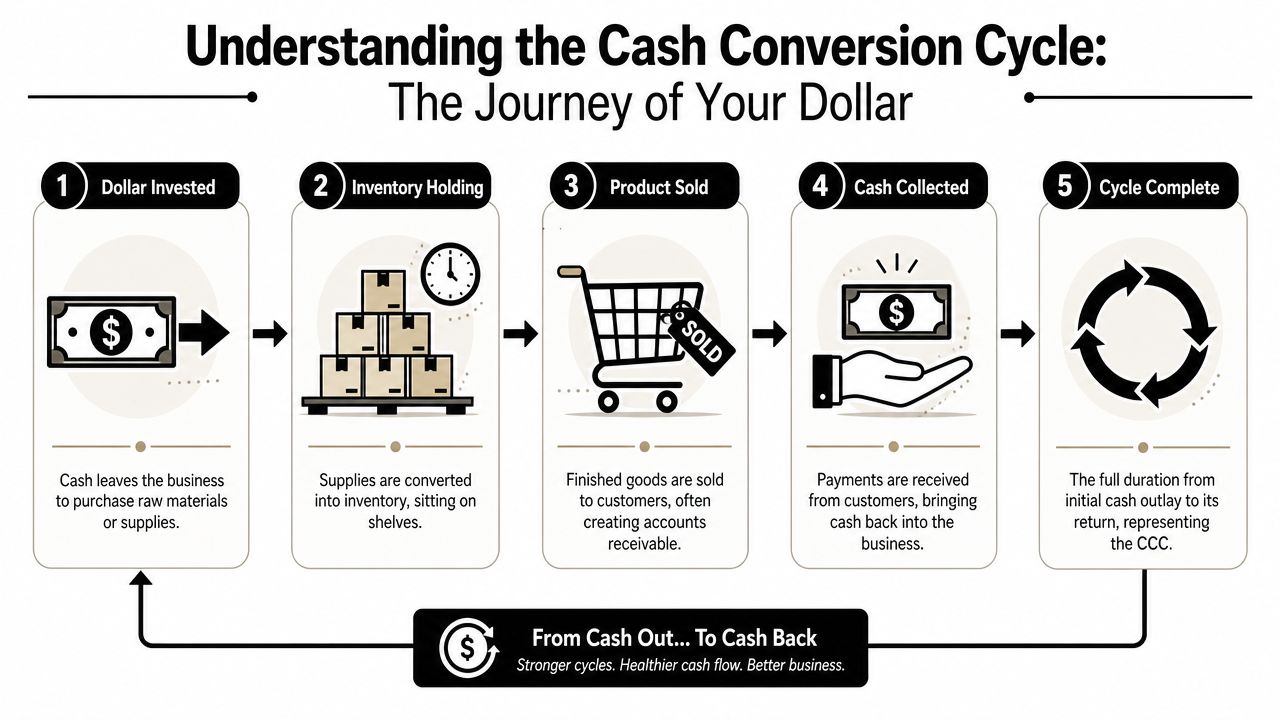

Think of the cash conversion cycle as the full journey of one dollar through your business.

You spend it first. Maybe on raw materials, finished goods, freight, labour tied to delivery, or other direct operating inputs. That dollar then sits in inventory or WIP, turns into a sale, becomes an invoice, and only later returns as cash collected.

According to Farseer's explanation of the cash conversion cycle formula, the cash conversion cycle is built from Days Inventory Outstanding (DIO) + Days Sales Outstanding (DSO) – Days Payable Outstanding (DPO), and it measures how many days cash is tied up from paying for inventory or services until the business collects cash from customers.

Where cash gets stuck

A shorter cycle means cash comes back faster. That usually gives the business more flexibility and less dependence on outside funding.

A longer cycle means money is tied up longer in operations. That can happen even when sales are strong.

Here's the intuitive version:

You pay out cash

Inventory or work sits for a period

You make the sale

You wait to collect

Supplier timing either helps or hurts along the way

The cycle isn't just a finance metric. It's an operating metric. It reflects how purchasing, stock control, invoicing, collections, and supplier management work together.

Practical rule: If you want to improve cash flow without chasing growth for growth's sake, reduce the time cash spends trapped inside operations.

The three moving parts

Each part of the formula points to a different operational reality.

DIO

Days Inventory Outstanding measures how long stock or production inputs sit before they turn into a sale. In retail and wholesale, that usually means shelves and warehouse stock. In manufacturing, it can also include raw materials and WIP.

High DIO often points to overbuying, weak forecasting, slow-moving SKUs, or poor reorder discipline.

DSO

Days Sales Outstanding measures how long it takes to collect from customers after a sale has been made and invoiced.

If DSO is drifting up, the issue is rarely just “customers are slow”. More often, invoicing goes out late, follow-up is inconsistent, dispute handling is messy, or payment methods create friction.

DPO

Days Payables Outstanding measures how long the business takes to pay suppliers.

This is the part many founders underuse. If supplier terms are too short, cash leaves the business earlier than it needs to. If terms are pushed too far, supplier trust can suffer. Strong payables management isn't about paying late. It's about paying strategically and predictably.

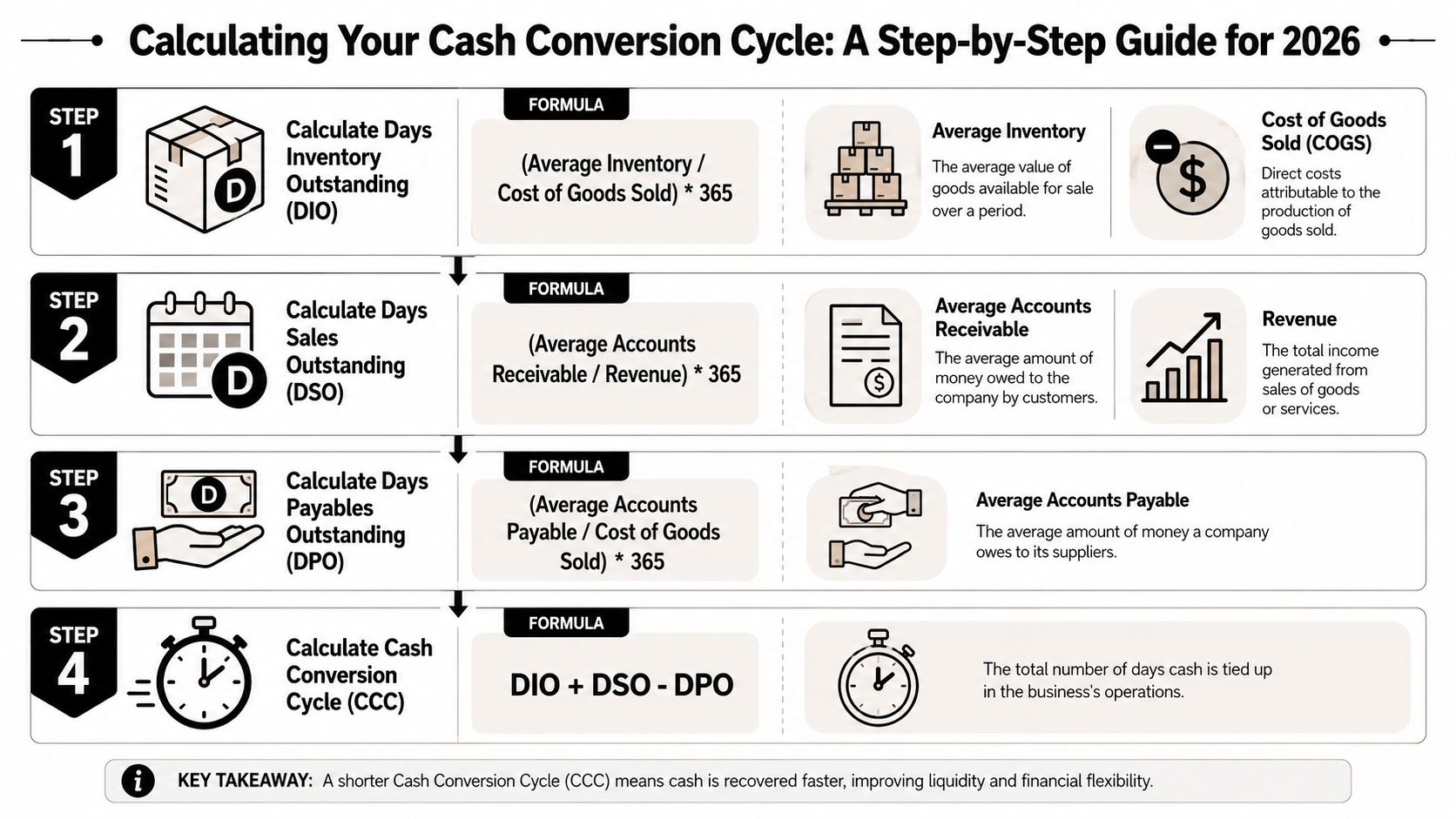

How to Calculate Your Business's CCC in 2026

Founders often assume the calculation is more complex than it is. It isn't. The harder part is pulling clean numbers from your accounting system and making sure inventory, receivables, and payables are coded consistently.

Use this visual as a quick reference before you start.

The formulas to use

The standard formulas are:

DIO = (Average Inventory / Cost of Goods Sold) × 365

DSO = (Average Accounts Receivable / Revenue) × 365

DPO = (Average Accounts Payable / Cost of Goods Sold) × 365

CCC = DIO + DSO − DPO

For most SMEs, the inputs come from the balance sheet and profit and loss:

Average Inventory means the average inventory balance over the period.

Average Accounts Receivable means the average debtor balance.

Average Accounts Payable means the average supplier balance.

Revenue is your sales income for the period.

Cost of Goods Sold is the direct cost tied to the goods sold.

For a service business with little or no inventory, DIO may be very low or not especially useful in the same way it is for stock-heavy businesses. Even then, the broader thinking still matters because cash can be trapped in WIP, delayed invoicing, and debtor collection lag.

A commonly used finance example from Wall Street Prep's CCC guide is 80 days DIO + 20 days DSO – 45 days DPO = 55 days CCC. That means the business waits 55 days on average to turn operational spending into cash.

Later in this section, use the video below if you want a quick walkthrough of the mechanics.

Example one for an ecommerce business

Take an ecommerce brand with meaningful stock on hand.

The founder should calculate:

DIO by comparing average inventory against cost of goods sold

DSO by comparing average receivables against revenue

DPO by comparing average payables against cost of goods sold

The interpretation matters more than the math.

If DIO is the largest component, cash is likely sitting in inventory too long. If DSO is creeping up, collections or payment methods need attention. If DPO is low, the business may be funding suppliers faster than necessary.

For ecommerce, this often exposes a familiar mismatch. Customers may pay quickly on some channels, but purchasing cycles, inbound lead times, and excess SKU count keep cash tied up long before the sale happens.

Example two for a service business

Now take a consulting or agency business.

There may be little physical inventory, but the founder still needs to watch the cycle through a service lens. Cash gets tied up in unbilled time, delayed project milestones, draft invoices sitting in approval, and clients paying on long terms.

In that case, DSO usually becomes the key pressure point. The practical questions are sharper than the formula:

Are invoices issued as soon as work is complete?

Are milestone invoices triggered automatically?

Does someone own collections?

Are disputes resolved quickly?

Are clients trained to pay through the easiest channel available?

A service firm can look “asset light” and still suffer from a slow cash conversion cycle because operational discipline around billing is weak.

Australian SME Benchmarks What Is a Good CCC

Once you've calculated your number, the next question is simple. Is it healthy, or is it a warning sign?

A practical benchmark from Klipfolio's CCC KPI guidance is that below 30 days is typically strong, 30–60 days is average, and above 60 days points to material working-capital strain.

A simple benchmark range

That benchmark is useful, but it's only a starting point.

A retailer with seasonal stock build-up may look worse for a period even if the business is operating normally. A manufacturer with long production cycles may never look like a lean ecommerce operator. A professional services firm should usually focus more on billing and collection discipline than stock movement.

Use the traffic-light view below as a practical starting frame.

Range | Interpretation | What it usually suggests |

|---|---|---|

Below 30 days | Strong | Cash is returning relatively quickly |

30 to 60 days | Average | Worth monitoring by component, not just as a headline number |

Above 60 days | Pressure zone | Working capital is likely getting trapped in one or more operating stages |

If your cycle is high, don't obsess over the headline first. Find out whether inventory days, debtor days, or supplier timing is doing the damage.

Typical Cash Conversion Cycle by Australian Industry

The table below gives a practical sector view for SMEs in Australia. These ranges are directional, not absolute. The point is to compare your number to a business model that looks like yours.

Industry Sector | Typical CCC Range (Days) | Key Challenge |

|---|---|---|

Retail | Often average to above average | Seasonal buying, markdown exposure, slow-moving stock |

Ecommerce | Often strong to average | Forecasting demand, SKU sprawl, stock tied up in inbound inventory |

Wholesale and Distribution | Often average to above average | Balancing stock availability with debtor collection timing |

Manufacturing | Often above average | Raw materials, WIP, production lag, customer terms |

Professional Services | Often low if billing is tight | Delayed invoicing, milestone slippage, slow debtor follow-up |

Trade and Project Services | Often average if jobs are billed late | WIP build-up, variation approval delays, retention or progress claims |

The right benchmark isn't just about industry. It also depends on seasonality, growth stage, and how much of your cash is intentionally tied up at a point in time.

Finding Your Cash Leaks from a High CCC

A high cash conversion cycle is not the problem by itself. It's the symptom.

The problem sits underneath it. Cash is being trapped somewhere operationally, and the only useful response is diagnosis. That's why broad advice like “improve cash flow” doesn't help much. You need to know exactly where the delay is happening.

Fathom's discussion of CCC interpretation for small businesses highlights a point many founders miss. The underlying issue often isn't the headline number. It's whether working capital is being trapped in stock, WIP, or debtor collections at the wrong time in the cycle.

When inventory is the problem

If DIO is carrying the weight, look at the stock layer first.

Founders usually find one of a few issues:

Too much range. The business carries too many SKUs, variations, or low-volume lines.

Weak forecasting. Purchasing follows instinct or supplier pressure instead of sales patterns.

Long replenishment cycles. Teams overbuy because they don't trust lead times.

No action on slow movers. Ageing stock stays in the system because no one owns clearance decisions.

For product businesses, operational reporting takes precedence over broad finance review. A clean aged inventory view often tells the story quickly. If you run an online store, this guide to ecommerce inventory management systems and controls is worth reviewing alongside your CCC analysis.

When receivables are the problem

If the cycle is being stretched by DSO, the issue is usually process, not just customer behaviour.

Look for friction points such as:

Invoices sent late

PO or approval requirements missed

No automated reminder workflow

Collections handled reactively

Clients paying by slow methods because nobody changed the setup

A founder might think collections are “pretty good” because bad debts are low. That misses the point. You can have low bad debt and still have cash trapped for too long.

Slow collection isn't always a credit problem. Often it's an admin problem wearing a credit mask.

When payables strategy is the problem

A low DPO can be healthy if you're taking discounts or protecting a critical supply relationship. But many SMEs pay early by accident, not strategy.

That usually happens because:

the approval chain is messy and staff pay bills as soon as they're cleared

nobody segments critical suppliers from flexible suppliers

the business hasn't renegotiated terms since it was much smaller

the owner wants peace of mind and pays everything immediately

The trade-off is simple. Every day you pay earlier than necessary reduces liquidity. But every day you push too hard without communication can damage trust. Good payables management is disciplined, not aggressive.

CFO-Driven Strategies to Shorten Your CCC

Once you know where the leak sits, the fix should be operational and repeatable. One-off cash grabs don't hold. Better systems do.

A lot of generic advice often falls short. “Chase debtors harder” isn't a strategy. “Keep less stock” isn't a strategy either. A proper working-capital response changes the workflow, the ownership, and the data the team sees every week.

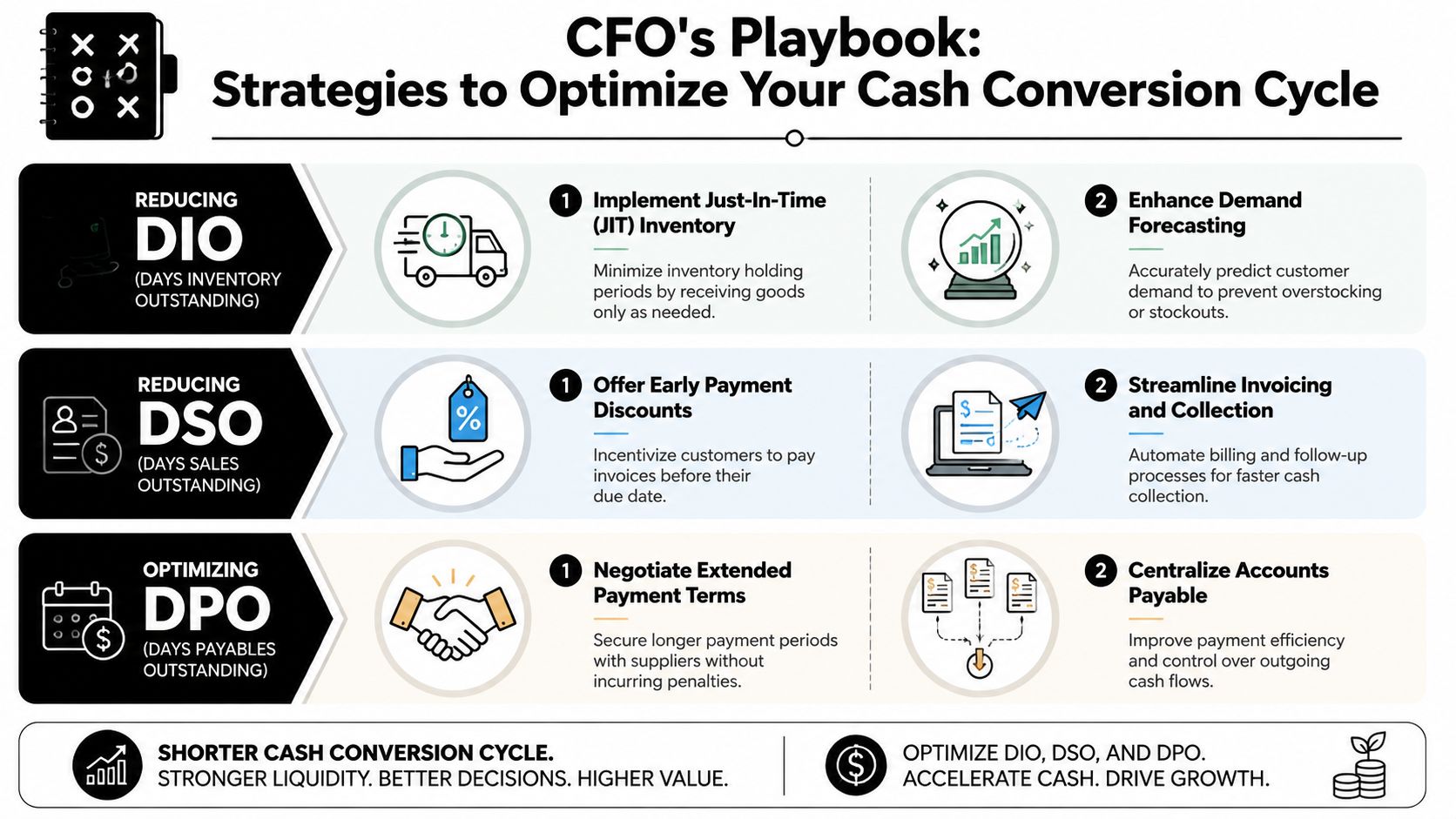

Fixing inventory drag

Inventory needs rules, not hope.

The most effective changes usually include:

Demand forecasting by SKU group rather than broad top-line planning

Minimum and maximum stock settings that reflect lead time and sales reality

Reorder discipline so buyers don't override the system without a reason

Slow-stock review meetings with a commercial decision on markdown, bundling, or exit

For businesses with stock exposure, reducing inventory days is one of the direct levers that improves the cycle. Slash's working capital article on CCC levers notes that the fastest path to releasing trapped cash is to reduce inventory days, accelerate invoice collection, or negotiate longer supplier terms.

What usually doesn't work is broad pressure to “buy less” without fixing forecasting, range complexity, and replenishment logic.

Speeding up collections

Receivables improve when the business removes excuses for delay.

That often means:

Invoice immediately when goods ship, milestones are met, or work is signed off.

Automate reminders so follow-up doesn't depend on memory.

Make payment easy with clear links, card options, or direct transfer details.

Escalate disputes fast because unresolved queries freeze collection.

Assign ownership so AR is someone's weekly responsibility, not a side task.

If your process is still manual, it helps to review how CFOs can automate AP and related finance workflows, because many of the same approval and routing principles apply when you're trying to tighten the full cash cycle. For a local operations view, this breakdown of accounts payable automation in Australia also helps frame where workflow bottlenecks tend to sit across finance teams.

Using payables without hurting suppliers

Payables strategy needs judgement.

There's a big difference between extending terms through negotiation and paying late. One protects cash while keeping supplier confidence. The other creates friction and often leads to tighter future terms.

A better approach looks like this:

Supplier type | Better move | What to avoid |

|---|---|---|

Critical supplier | Agree terms clearly and pay predictably | Surprising them with late payment |

Flexible supplier | Negotiate for more time if volume supports it | Assuming old terms are fixed forever |

Discount supplier | Compare discount value against cash needs | Paying early automatically without review |

Strong DPO comes from supplier design, not supplier damage.

The goal is to preserve optionality. Hold cash where you reasonably can, but don't create supply risk to win a few extra days.

Your 90-Day Implementation Plan

Most businesses don't need another finance theory session. They need an order of operations.

Recent working-capital commentary has pointed to a shift from pure “days management” to systems-led cash acceleration, where technology, automation, and financing reduce friction in invoicing and payables workflows, as noted in Wayflyer's discussion of ecommerce working-capital management. That's the right lens for an Australian SME. Fix the process, not just the ratio.

Days 1 to 30

Start with visibility.

Calculate your baseline for DIO, DSO, DPO, and total cash conversion cycle.

Pull aged receivables and aged inventory into one review.

Map invoice timing from delivery to issue date.

Identify supplier terms and note which ones are negotiated versus default.

For businesses with marketplace exposure or stock complexity, practical FBA inventory optimization strategies can also help sharpen the inventory side of the review.

Days 31 to 60

Fix the obvious friction.

Turn on AR automation for reminders and follow-up.

Tighten billing triggers so completed work doesn't sit unbilled.

Review slow-moving stock and decide what gets cleared, bundled, or discontinued.

Segment suppliers by importance and flexibility.

If debtor lag is a recurring issue, this guide to accounts receivable management workflows is a useful companion for tightening ownership and cadence.

Days 61 to 90

Make the changes stick.

Build a simple weekly dashboard in Xero, NetSuite, or your reporting layer that tracks:

DIO

DSO

DPO

Overall cash conversion cycle

Aged receivables

Slow-moving stock

Pair that with a small tool stack that supports discipline. For many SMEs, that means the accounting platform, document capture, approval workflows, and a proper inventory system that matches the business model. The software matters less than consistency. If the team can't see the bottleneck quickly, it usually won't get fixed quickly.

If you want a sharper view of where cash is getting trapped in your business, Nexist helps Australian founders diagnose the actual leak, fix the underlying process, and build finance systems that put more cash back in the bank.

cash conversion cycle, cash flow management, working capital, sme finance australia, virtual cfo

" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="dSFdkJotL" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="wscNJE44G" transform="translate(0 0.129)" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="sTpjGo1tb" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="s7ffpmKOD" transform="translate(0 0.129)" width="24px"/><g d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.000006px" id="D0ecaHEcW" transform="translate(0 0)" width="24px"><path d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z" fill="rgb(55, 184, 218)" height="24.000006px" id="IPLFE6zXx" width="24px"/><path d="M 4.02 0 L 0 0 L 0 12.092 L 4.02 12.092 Z" fill="rgb(255, 255, 255)" height="12.09201px" id="FWhtzAyuY" transform="translate(2.863 8.375)" width="4.02px"/><path d="M 2.274 0 C 0.899 0 0 0.904 0 2.089 C 0 3.25 0.871 4.179 2.221 4.179 L 2.247 4.179 C 3.648 4.179 4.521 3.25 4.521 2.089 C 4.495 0.904 3.649 0 2.274 0 Z" fill="rgb(255, 255, 255)" height="4.17876px" id="VmOsKv4kO" transform="translate(2.625 2.545)" width="4.52095px"/><path d="M 7.641 0 C 5.509 0 4.554 1.173 4.019 1.996 L 4.019 0.284 L 0 0.284 C 0.053 1.419 0 12.376 0 12.376 L 4.019 12.376 L 4.019 5.623 C 4.019 5.262 4.045 4.9 4.151 4.642 C 4.442 3.92 5.103 3.172 6.214 3.172 C 7.667 3.172 8.25 4.282 8.25 5.907 L 8.25 12.376 L 12.269 12.376 L 12.269 5.442 C 12.269 1.728 10.286 0 7.641 0 Z" fill="rgb(255, 255, 255)" height="12.37626px" id="n1XUbhaq0" transform="translate(9.105 8.09)" width="12.268830000000001px"/></g></g></g></g></svg>)