Master Australian SME Tax and Compliance

Master Australian SME tax and compliance. Reduce risk, stop cash leaks, & reclaim time with our guide on deadlines, penalties, & systems. Essential for

Ansh Malhotra

You know the feeling. BAS is due tomorrow, payroll has already gone through, a supplier invoice is missing, your bookkeeping file doesn't agree to the bank, and someone on the team swears the super was “sorted last week”. The old cliché was a shoebox of receipts. The modern version is worse. It's receipts in email, payroll in one app, invoices in another, card spend in a feed that hasn't been reviewed, and a founder trying to reconcile all of it between sales calls.

That's where tax and compliance stops being an admin task and starts acting like an operating risk. It takes cash out of the business when GST is coded badly. It burns hours when someone has to fix old transactions under deadline. It narrows your choices when ATO debt starts building and every reporting cycle becomes a scramble.

Most SME owners don't need another article that provides only a list of obligations. They already know they have obligations. What they need is a way to turn compliance into a cleaner financial system, one that protects cash flow, reduces rework, and gives them more freedom to focus on customers, staff, and growth.

The shift starts when you stop treating compliance as a year-end event. It belongs inside the monthly operating rhythm, alongside margin review, debtor follow-up, and stock control. That's the same logic behind a disciplined quarterly business review process. If the numbers drive decisions, the underlying data has to be accurate enough to trust.

Table of Contents

Introduction Beyond the Shoebox of Receipts

A lot of businesses look fine from the outside while their compliance process is held together by memory, goodwill, and late nights. Sales are coming in. The team is busy. Customers are being served. Then one due date exposes the whole setup. The BAS can't be finalised because wages were coded inconsistently. Input tax credits are uncertain because documents weren't collected properly. A contractor has been treated one way in payroll and another way in accounts.

That mess creates two costs at once. The visible cost is the lodgment risk. The hidden cost is operational drag. Someone has to stop productive work and go hunting for answers. Usually that someone is the owner, the office manager, or the same finance person who's already overloaded.

Practical rule: If compliance only gets attention near a deadline, the business is paying for that delay somewhere else through rework, slower decisions, and poorer cash visibility.

The answer usually isn't “work harder” or “be more organised”. It's to build a system that makes the right action easier than the wrong one. That means cleaner coding rules, a reliable month-end process, documented responsibilities, and fewer manual handoffs.

Founders often assume tax and compliance belongs purely to the accountant. It doesn't. The accountant helps with lodgment and advice. The business still has to produce clean inputs, on time, every cycle. If the internal process is weak, every external adviser is working around noise.

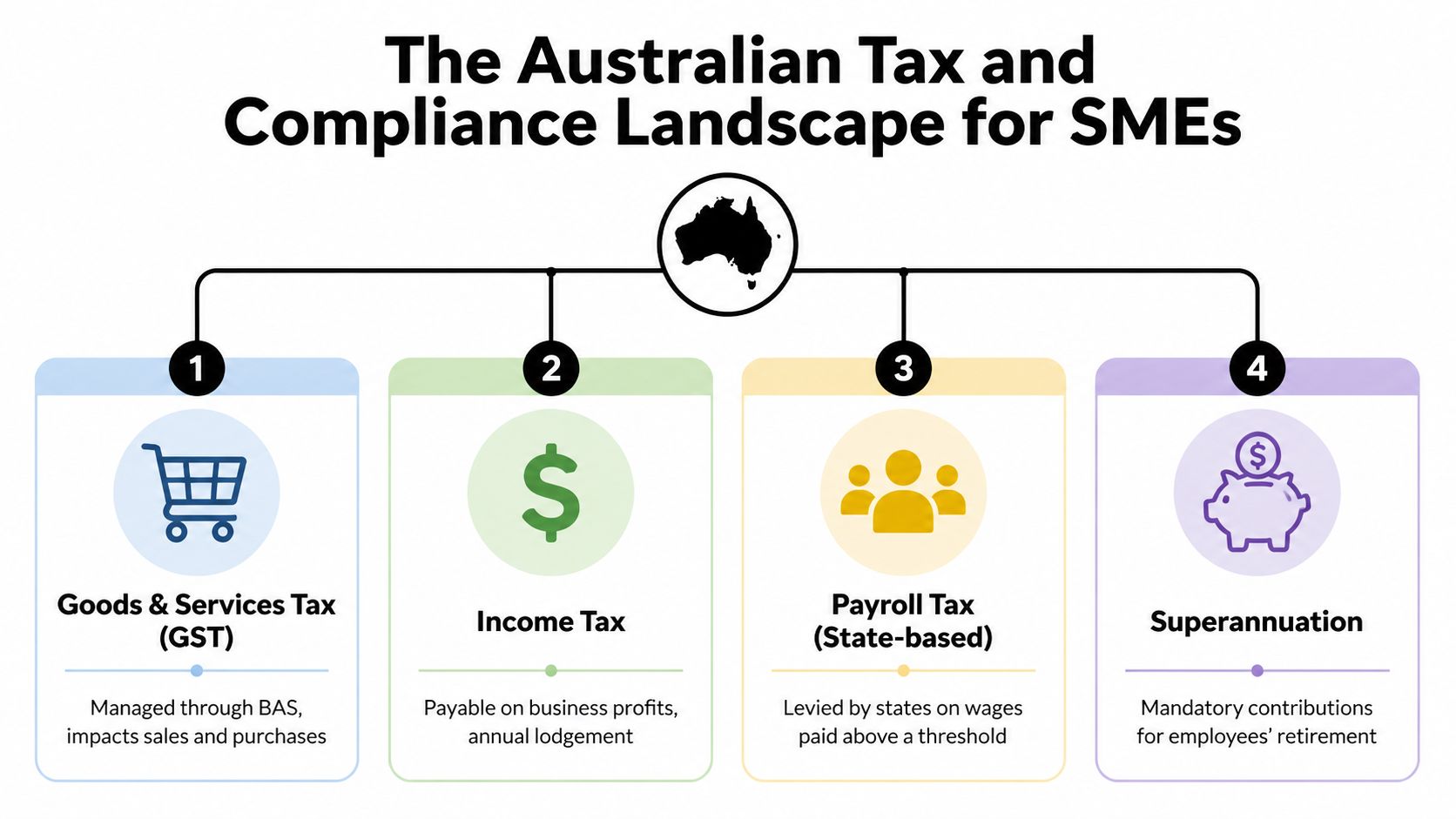

The Australian Tax and Compliance Landscape for SMEs

Most Australian SMEs don't have one compliance job. They have a stack of related ones. The easiest way to make sense of it is to treat the system like a building supported by four core pillars. If one pillar is weak, pressure shows up somewhere else.

The four moving parts founders need to track

GST and BAS sit closest to day-to-day trading. Every sale, purchase, adjustment, and tax code decision can affect what flows into the BAS. If the bookkeeping is messy, BAS becomes guesswork instead of reporting.

PAYG withholding is different. This isn't your business's money to use as working capital. It's money withheld from wages that must be tracked and remitted properly. Businesses get into trouble when they treat payroll outputs as if they can be tidied up later.

Superannuation adds another layer. It depends on payroll accuracy, timing, and consistent treatment of workers. Even when wages are processed on time, super can still become a weak point if approvals, fund details, or payment workflows are sloppy.

Income tax is the annual picture. It depends on the integrity of everything underneath it. If the profit and loss, balance sheet, payroll records, and GST treatment have been inconsistent all year, annual tax becomes an expensive exercise in reconstruction.

Why scale matters

The system you're operating inside is enormous. The ATO reported collecting A$641.1 billion in net tax and other revenue in 2023–24, while administering 2.5 million businesses, 15.7 million individual taxpayers and 12.8 million GST-registered entities, and processing around 36 million tax returns and other forms in the same year, which shows the scale of the environment SMEs operate within (ATO scale and lodgment volume).

That scale matters because the system can't rely on informal explanations and memory. It relies on records, digital lodgment, structured reporting, and consistency.

A practical way to think about your obligations is this:

Trading layer. Sales, purchases, bills, receipts, and bank feeds.

People layer. Employees, wages, withholding, and super.

Entity layer. Profit, drawings, loans, and annual tax position.

Control layer. Review, approvals, records, and lodgment discipline.

A founder doesn't need to become a tax specialist. They do need a reliable map of where each obligation starts, who owns it, and what data feeds it.

When businesses struggle with tax and compliance, the issue usually isn't that the rules exist. It's that the business has never clearly linked its daily operations to those rules.

Key Deadlines and Penalties You Cannot Afford to Miss

The fastest way to lose control of compliance is to treat due dates as admin reminders instead of cash events. A missed obligation rarely stays isolated. It creates follow-up work, can trigger penalties or interest exposure, and often forces rushed decisions with incomplete information.

The threshold that changes everything

One of the sharpest lines in the system is GST registration. Entities must register once GST turnover reaches AU$75,000. For non-profits, the threshold is AU$150,000 (GST registration threshold and risk).

That sounds simple until a business has seasonal sales, mixed supply types, marketplace revenue, or a growth spike. GST turnover isn't just a casual glance at cash received. Once registration applies, the business moves into a more disciplined environment where tax coding, tax invoice validation, retained records, and BAS reporting need to line up properly.

A lot of founders wait too long because they think they'll “sort GST out once sales settle down”. That approach creates backdated clean-up work and can push avoidable liabilities into future cash flow.

A practical deadline view

The exact dates depend on your reporting cycle and structure, but the pattern is predictable. Here's the table I use when discussing risk with founders.

Obligation | Typical Deadline | Primary Risk of Non-Compliance |

|---|---|---|

BAS and GST reporting | Periodic lodgment cycle set for the business | Incorrect GST, late lodgment, rushed adjustments, weak records |

PAYG withholding | Regular reporting and payment cycle through payroll and activity statement obligations | Under-remittance, payroll mismatch, director exposure if arrears build |

Superannuation contributions | Quarterly payment discipline for eligible employees | Employee underpayment issues, remediation work, cash strain from catch-up payments |

Annual income tax lodgment | Annual cycle after year-end | Reconstruction work, poor tax planning, delayed visibility on actual liability |

Some owners find it helpful to review overseas tax training material when they want a clearer feel for how company tax returns are assembled and why supporting records matter. A resource like practical CT 600 training can be useful for understanding the discipline behind company tax preparation, even though Australian obligations are different.

What missed deadlines do to cash flow

Missing a due date is rarely just a filing issue. It usually points to one of three underlying problems:

The data wasn't ready

Transactions weren't reconciled, payroll wasn't reviewed, or source documents were incomplete.The owner was the bottleneck

Nothing moved until the founder had time to approve, explain, or find missing information.The business was already short on cash

The due date was missed because the business couldn't comfortably fund the payment.

That's why penalties and interest are only part of the story. The larger issue is that deadline stress exposes weak operating discipline.

If you're already carrying complexity around tax settings in retirement, contributions, or broader tax decisions, it also helps to keep your planning tools current. A founder reviewing super-related exposure might find Nexist's Division 296 calculator guide useful as part of a wider tax planning discussion.

A simple internal rule works well here. Don't aim to finish compliance on the due date. Aim to have the numbers manager-ready well before that date, so review happens before pressure distorts judgment.

Uncovering Hidden Cash Leaks Tied to Poor Compliance

Most owners think compliance costs them money only when the ATO issues a penalty or interest charge. In practice, the bigger losses usually happen unnoticed inside normal operations.

Where the money actually leaks

The first leak is bad coding. If purchases are coded inconsistently for GST, BAS reporting becomes less reliable and internal profit reporting gets weaker too. In retail, wholesale, manufacturing, and hospitality, that often means purchasing decisions are being made off numbers that aren't clean.

The second leak is lost evidence. A valid transaction without proper supporting records can create friction later when someone tries to confirm treatment. Even before any regulator asks questions, the business spends time re-checking, searching inboxes, and redoing work.

The third leak is people time. Founders rarely cost out the hours spent cleaning historical errors, following up missing payroll details, or fixing transaction allocations after the month should have closed. Those are real costs. They pull attention away from pricing, sales, stock turns, customer service, and hiring.

Compliance problems don't stay in the finance lane. They spread into operations because someone has to interrupt useful work to repair preventable errors.

Tax debt is a cash flow problem first

The discussion intensifies with the ATO's report of around $50.2 billion in collectable tax debt in 2023–24, and small businesses accounted for about $35.7 billion of that amount (small business tax debt and arrears pressure).

That matters because once debt accumulates, compliance changes character. You're no longer just dealing with lodgment. You're managing arrears, repayment pressure, and enforcement risk while still trying to run the business.

A typical pattern looks like this:

Step one. BAS is delayed because the books aren't clean.

Step two. Lodgment happens late, and the payment can't be met comfortably.

Step three. The next cycle arrives before the previous amount is resolved.

Step four. Tax debt starts competing with wages, stock purchases, and supplier payments.

That's why good tax and compliance is a cash discipline tool. It protects optionality. It gives the owner earlier visibility, cleaner numbers, and more time to act before a problem hardens into debt.

If a business is already in arrears, the conversation should shift quickly from “How do we lodge?” to “How do we stop the debt from controlling the business?” Those are different questions, and they need different decisions.

Your Practical SME Compliance Checklist and SOP

Most compliance pain comes from complexity, not laziness. That's especially true in businesses juggling payroll, contractors, inventory, and multi-channel sales. Research on the broader tax gap points to underreporting dominating where income is less withheld and less directly reported, which is why founder-led teams need stronger automation and internal controls rather than more last-minute heroics (complexity and compliance burden in small business).

Monthly controls that keep you out of trouble

A useful compliance routine starts monthly, not quarterly.

Close the bank properly

Reconcile every operating account, credit card, loan account, and payment platform. Don't leave “I'll check that later” items sitting unreconciled unless someone owns the follow-up.Review the profit and loss with intent

Scan for unusual expense categories, duplicate suppliers, negative balances, and revenue posted to the wrong accounts. If gross margin looks odd, don't move on until you know why.Check GST-sensitive coding

Review accounts where GST errors commonly sit, such as software, freight, subscriptions, owner-paid expenses, and mixed-use purchases. The earlier you fix coding, the less rework lands in BAS prep.Run payroll exception checks

Confirm wages, withholding, leave balances, and any contractor payments that may need review. Payroll errors age badly. They're much easier to fix in the current period than in a year-end clean-up.Verify document capture

Make sure bills, receipts, and adjustment notes are recorded against transactions in the system. A clean ledger with poor evidence is only half-finished work.

Owner test: If you disappeared for two weeks, could someone else tell what was finalised, what was pending, and what needed review?

Quarterly SOP for BAS and payroll compliance

A standard operating procedure doesn't need to be long. It needs to be usable. If your current process lives in one person's head, it isn't a process.

A practical quarterly SOP can be as simple as this:

Lock the bookkeeping cut-off

Set the date after which prior-period edits need approval.Complete reconciliations

Finalise bank, card, loan, payroll clearing, and key balance sheet accounts.Review GST treatment

Check sales, purchases, adjustments, and any unusual items before BAS preparation.Review payroll and super outputs

Confirm withholding, wages, and contribution records align to payroll reports.Prepare management review pack

Include BAS draft, profit and loss, balance sheet, and issue list.Approve and lodge

Record who approved, when it was lodged, and where supporting records are stored.Archive evidence

Save reports, workpapers, and correspondence in one consistent location.

If you need a reference point for documenting repeatable processes clearly, this modern SOP writing guide is a sensible resource. The principle is simple. Write the process so a competent person can follow it without chasing tribal knowledge.

The businesses that handle tax and compliance well don't usually have more talented people. They have fewer mysteries. Everyone knows what must happen, when it must happen, who owns it, and what “done” looks like.

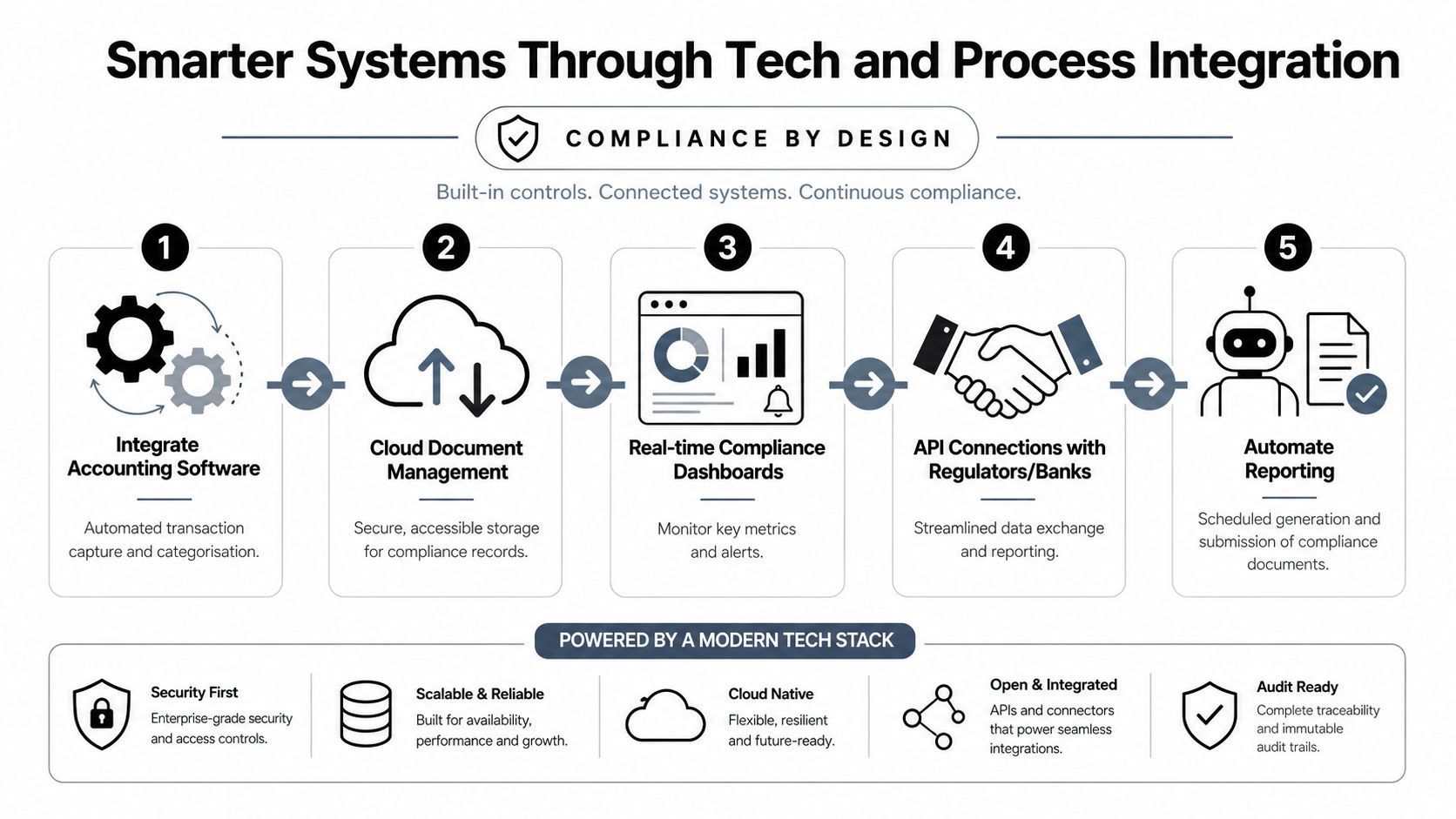

Smarter Systems Through Tech and Process Integration

Checklists help, but they won't solve a broken data flow. If your team captures transactions one way, processes payroll another way, stores documents somewhere else, and reviews numbers in a spreadsheet that doesn't tie back to the ledger, you're creating compliance friction by design.

Compliance by design starts at transaction capture

The ATO increasingly relies on pre-fill, digital reporting, and cross-entity matching, so errors in source data such as chart of accounts mapping, GST coding, and PAYG withholding classification can propagate into BAS, income tax, and payroll reporting. The practical control is to implement a tax data model with clear ownership for each data element, then test for consistency before lodgment (digital reporting and source data control).

That's the point of a modern stack. It isn't just speed. It's data integrity at the start of the workflow.

If a bill enters Xero or MYOB with the wrong tax code, if Dext or Hubdoc pushes through poor metadata, or if payroll settings in Employment Hero or KeyPay don't match the chart of accounts, the error doesn't stay local. It flows downstream into reports, BAS, and year-end tax work.

What a connected stack looks like

A practical SME setup often includes:

Cloud accounting such as Xero or MYOB as the ledger of record.

Receipt and bill capture such as Dext or Hubdoc to standardise source documents.

Payroll software with clear pay item mapping and review controls.

Approval workflows for supplier bills, payroll sign-off, and period lock dates.

Reporting dashboards that surface exceptions rather than just totals.

The trick is to define ownership. Someone owns supplier setup. Someone owns payroll mappings. Someone reviews GST exceptions. Someone approves lodgment-ready numbers. Without ownership, software just helps people make faster mistakes.

A connected system also changes behaviour. Staff stop asking, “Can we fix it later?” because the process makes correct capture part of the daily routine.

That's where firms such as Xero partners, ERP implementers, specialist bookkeepers, and virtual CFO providers can all play a role. Nexist, for example, works across cash flow, reporting, process design, payroll, BAS support, and SOP implementation as part of a broader finance operating model. The point isn't the label on the provider. The point is whether your systems, people, and controls connect.

How a Virtual CFO Builds Your Automated Compliance Engine

Founders can build this themselves. Most shouldn't.

Not because they can't understand it, but because they usually become the exception handler for every broken process. They approve payroll when they should be selling. They chase missing receipts when they should be reviewing pricing. They try to interpret tax exposure from half-clean reports when they should be making strategic decisions.

What founders should own and what they should delegate

The founder should own:

Risk appetite

Cash priorities

Approval authority

Commercial decisions

The operating finance function should own:

Calendar discipline

Reconciliations

Data quality checks

Lodgment workflow

Issue escalation

That division matters. When owners hold both strategic and clerical responsibility, the business slows down and control becomes personality-dependent.

A virtual CFO steps in at the design layer. They don't just ask whether BAS was lodged. They ask whether the workflow, data model, reporting cadence, and controls reduce the chance of error in the first place. They also connect compliance to decision-making. If GST treatment keeps breaking in one revenue line, that may reveal a product, pricing, or systems issue. If payroll errors repeat, the root cause may sit in rostering, onboarding, or poor delegation.

Good oversight doesn't remove responsibility from the owner. It removes avoidable noise from the owner's week.

The payoff is control, not just lodgment

A mature finance setup gives you cleaner reporting, fewer deadline shocks, and better decisions under pressure. It also helps you know when a specialist should be brought in for a narrower tax matter. For example, businesses dealing with innovation claims may need separate support from R&D incentive consultants, while the core finance lead keeps the broader reporting and control environment stable.

If you're weighing whether this should sit internally or with an external strategic partner, it helps to understand what a virtual chief financial officer does in practice. The primary value isn't extra commentary on the numbers. It's building a finance engine that turns tax and compliance from reactive admin into operational control.

If tax and compliance is absorbing too much time, creating cash stress, or forcing last-minute clean-up every quarter, Nexist can help you build a finance system that's structured, delegated, and useful. The focus is practical: cleaner data, stronger controls, better cash visibility, and fewer founder hours lost to financial admin.

tax and compliance, sme tax australia, bas lodgement, virtual cfo, ato compliance

" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="dSFdkJotL" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="wscNJE44G" transform="translate(0 0.129)" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="sTpjGo1tb" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="s7ffpmKOD" transform="translate(0 0.129)" width="24px"/><g d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.000006px" id="D0ecaHEcW" transform="translate(0 0)" width="24px"><path d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z" fill="rgb(55, 184, 218)" height="24.000006px" id="IPLFE6zXx" width="24px"/><path d="M 4.02 0 L 0 0 L 0 12.092 L 4.02 12.092 Z" fill="rgb(255, 255, 255)" height="12.09201px" id="FWhtzAyuY" transform="translate(2.863 8.375)" width="4.02px"/><path d="M 2.274 0 C 0.899 0 0 0.904 0 2.089 C 0 3.25 0.871 4.179 2.221 4.179 L 2.247 4.179 C 3.648 4.179 4.521 3.25 4.521 2.089 C 4.495 0.904 3.649 0 2.274 0 Z" fill="rgb(255, 255, 255)" height="4.17876px" id="VmOsKv4kO" transform="translate(2.625 2.545)" width="4.52095px"/><path d="M 7.641 0 C 5.509 0 4.554 1.173 4.019 1.996 L 4.019 0.284 L 0 0.284 C 0.053 1.419 0 12.376 0 12.376 L 4.019 12.376 L 4.019 5.623 C 4.019 5.262 4.045 4.9 4.151 4.642 C 4.442 3.92 5.103 3.172 6.214 3.172 C 7.667 3.172 8.25 4.282 8.25 5.907 L 8.25 12.376 L 12.269 12.376 L 12.269 5.442 C 12.269 1.728 10.286 0 7.641 0 Z" fill="rgb(255, 255, 255)" height="12.37626px" id="n1XUbhaq0" transform="translate(9.105 8.09)" width="12.268830000000001px"/></g></g></g></g></svg>)