Cash Reserves for Business: 2026 Guide for Founders

Master cash reserves for business with our 2026 guide. Learn to calculate, build, and protect your company's financial buffer effectively for growth.

Ansh Malhotra

You can be having your best sales month in ages and still feel sick opening the bank app.

That usually happens when the numbers look fine in the P&L, but the cash is spoken for. A BAS payment is due soon. Super is coming. A supplier wants payment before releasing stock. Two large customers are late. Then a vehicle, machine, or fridge decides this is the perfect week to fail. On paper, the business is profitable. In real life, you're scrambling.

That's why cash reserves for business can't be treated as a vague “rainy day” idea. For Australian SMEs, especially those carrying stock or waiting on debtors, reserves are part of the operating system. They buy time, reduce panic, and let you make decisions without reaching for expensive short-term funding every time timing turns against you.

Table of Contents

Why Cash Is More Than King It Is Your Moat

A lot of founders learn this the hard way. Revenue grows, the team gets bigger, stock turns faster, and everyone assumes the business is stronger than ever. Then one delayed payment or one ugly quarter exposes how little room there really is.

That gap between “busy” and “liquid” is where stress lives.

A widely cited benchmark from JPMorganChase found that half of small businesses have 27 days or fewer of cash buffer, which means many firms are operating with less than one month of liquidity, a useful warning sign for Australian operators thinking about reserves as a working-capital control problem rather than just a savings habit (JPMorganChase Institute small business report).

Cash doesn't just protect the business from disaster. It protects the owner from bad decisions made under pressure.

That's the shift. Cash reserves for business are not dead money. They are decision-making power. They let you hold your pricing when a customer pushes back. They let you buy stock when a supplier offers favourable terms. They let you survive a slow patch without cutting the muscle out of the business.

What cash reserves actually change

For a founder, a real reserve changes behaviour in practical ways:

You stop using tax money as operating cash. That false comfort disappears.

You stop confusing a full sales pipeline with liquidity. Work in progress and stock don't pay wages.

You negotiate better. Suppliers, lenders, and landlords all respond differently when you're not desperate.

You gain time. Time to chase debtors properly, reduce costs carefully, and solve the right problem.

The businesses that stay calm during shocks usually aren't lucky. They've built a buffer on purpose.

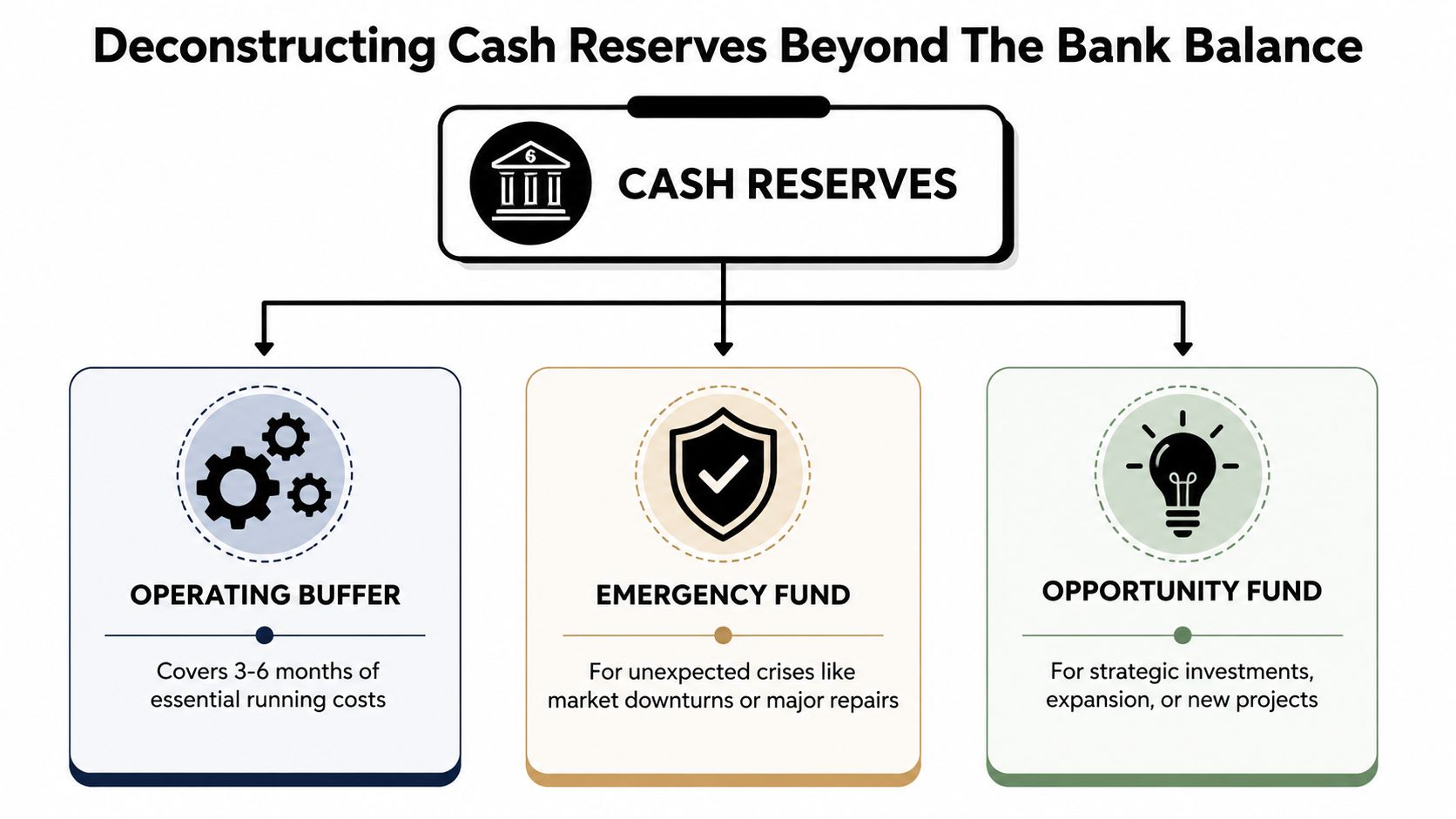

Deconstructing Cash Reserves Beyond The Bank Balance

Friday afternoon looks healthy. The bank account is full, invoices are still going out, and sales have held up. By Monday, payroll is due, a BAS payment is sitting there, two supplier accounts need clearing before the next stock release, and that “healthy” balance has already been spent three times on paper.

That is why a single bank balance is a poor measure of financial safety. It shows cash in one place, but it does not show purpose, timing, or restrictions. For inventory-heavy businesses, that distinction matters more because cash gets pulled in several directions at once. Stock buys, freight, GST, wages, and debtor delays can all hit before the sales cash comes back.

A better structure is to split cash by job, then manage each pool against your forecast rather than treating reserves as a static emergency pile.

The three buckets founders need

Most SMEs need three distinct cash buckets.

Bucket | Job | Typical use |

|---|---|---|

Operating buffer | Covers normal timing gaps | Payroll, rent, suppliers, routine shortfalls |

Emergency fund | Absorbs non-routine shocks | Equipment failure, delayed major receipts, sudden sales dip |

Opportunity fund | Gives you controlled flexibility | Stock buy-ins, growth projects, strategic hires |

Operating buffer supports the daily cash conversion cycle. It covers the gap between paying suppliers and collecting from customers. If you carry inventory, this bucket does more work than founders expect because cash often leaves the business weeks or months before the related sale is converted to cash.

Emergency fund protects the business when one event throws off the plan. A late customer payment, a damaged shipment, an ATO payment you underestimated, or a short trading month should not force you to draw on supplier terms or miss wages.

Opportunity fund is separate for a reason. Growth often needs upfront cash at inconvenient times. A supplier offers a bulk buy discount. A competitor exits and stock becomes available. A strong hire comes onto the market. If you fund those decisions out of operating cash, you create stress elsewhere.

If every dollar has the same label, you'll eventually spend strategic cash on operational noise.

Where each bucket should live

The account structure matters almost as much as the reserve total.

In practice, I want founders to be able to answer four questions quickly. How much cash is free for operations this week? How much is already committed to tax? How much is held for true disruption? How much is available for a planned growth move? If the answer to all four is “it's all in the main account,” control is weaker than it looks.

A practical setup is simple:

Keep operating cash accessible. This is the trading account that handles normal inflows and outflows.

Keep reserve cash separate. It should be easy to transfer, but not so visible that it gets used to cover every small shortfall.

Keep tax cash ringfenced. BAS, PAYG, super, and income tax are liabilities, not spare cash.

Keep opportunity cash deliberate. Use a separate account or sub-account with a clear rule for when it can be used.

For Australian SMEs, this works best when the buckets sit inside an active cash management rhythm. Review debtor collections weekly. Set supplier payment terms with intent. Map tax dates into the forecast. Check debt repayments against trading volatility. Founders dealing with cross-border operations or expansion planning can see a similar budgeting discipline in this piece on navigating the UAE financial landscape.

The point is clarity. A reserve is not just money you happen to have. It is money assigned to a job, protected from the wrong uses, and reviewed often enough to stay aligned with how the business trades.

How Much Cash Is Enough Calculating Your Needs

A founder looks at the bank balance on Friday and sees enough cash to feel safe. Then payroll lands, a supplier wants a deposit on the next stock order, BAS is due next week, and two large customer invoices slip by another 14 days. The problem was never the balance. The problem was timing.

That is why a flat “3 to 6 months” rule only gets you part of the way. For an Australian SME, the right reserve target depends on how cash behaves between sale, collection, tax, debt, and restocking. The more cash you tie up in inventory, the less useful a static rule becomes on its own.

Three ways to set a reserve target

Use these models for different jobs, not as competing answers.

Model | How it Works | Best For | Potential Pitfall |

|---|---|---|---|

Months of operating expenses | Set a reserve based on core monthly costs | Service businesses and firms with stable overheads | Can understate needs if stock or debtor timing is the real issue |

Percentage of annual revenue | Hold a share of annual revenue as liquidity | High-level planning and board-level target setting | Revenue can look strong while cash conversion is weak |

Cash flow forecast model | Build reserves around expected inflows, outflows, and timing gaps | Inventory-heavy, seasonal, fast-growing, or volatile businesses | Requires discipline and regular updates |

The expense model answers a survival question. How long can the business keep paying wages, rent, software, insurance, and loan repayments if trading slows or collections blow out?

The revenue model is a scaling question. It helps owners and boards sense-check whether liquidity is broadly in line with the size and risk of the business, but it can give false comfort if margins are thin or receivables are slow.

For product businesses, I treat both as reference points. The working number should come from a rolling cash forecast.

Choosing the right model for your business

If you run a service business with steady monthly billing, low stock, and short collection cycles, an expense-based reserve target is often enough to start. It is easy to explain, easy to measure, and usually close enough to support good decisions.

If you run a wholesaler, retailer, manufacturer, or ecommerce business, reserves need to reflect the cash conversion cycle. Stock is usually the biggest distortion. Cash leaves early, often through deposits, freight, customs, or bulk buys. It returns later, and not always on the timetable your forecast assumed.

That changes how I set the buffer. I want to see four pressure points in one view:

stock purchases and supplier terms

debtor collection timing

tax dates and super obligations

debt repayments and other fixed commitments

A reserve target that ignores any of those is incomplete.

For example, a business may show two months of overhead in the bank and still be under-reserved if it must commit heavily to inventory six weeks before peak season. Another may hold less cash than the textbook rule suggests and still be well covered because collections are tight, supplier terms are strong, and tax has been ringfenced properly.

This is why receivables discipline belongs inside the reserve calculation, not beside it. Founders who tighten invoicing, follow-up, and dispute resolution usually need less dead cash sitting idle because the timing risk is lower. A stronger accounts receivable management process directly improves the quality of your reserve, not just the quantity.

The practical framework is simple. Start with a minimum floor based on core monthly costs. Then stress-test it against your next 13 weeks of cash flow, including stock commitments, BAS, PAYG, super, debt servicing, and expected collection delays. If the forecast trough falls below your comfort line, your reserve target is too low, even if the rule of thumb says you are covered.

Founders operating across regions often benefit from comparing how other markets approach forecasting discipline. This guide to navigating the UAE financial landscape is a useful example of budgeting and forecasting used as management tools rather than compliance tasks.

You do not need a perfect model. You need one that reflects how your business trades. If your reserve target cannot explain inventory, debtors, tax, and debt in the same sentence, it is too simplistic for the decisions you are making.

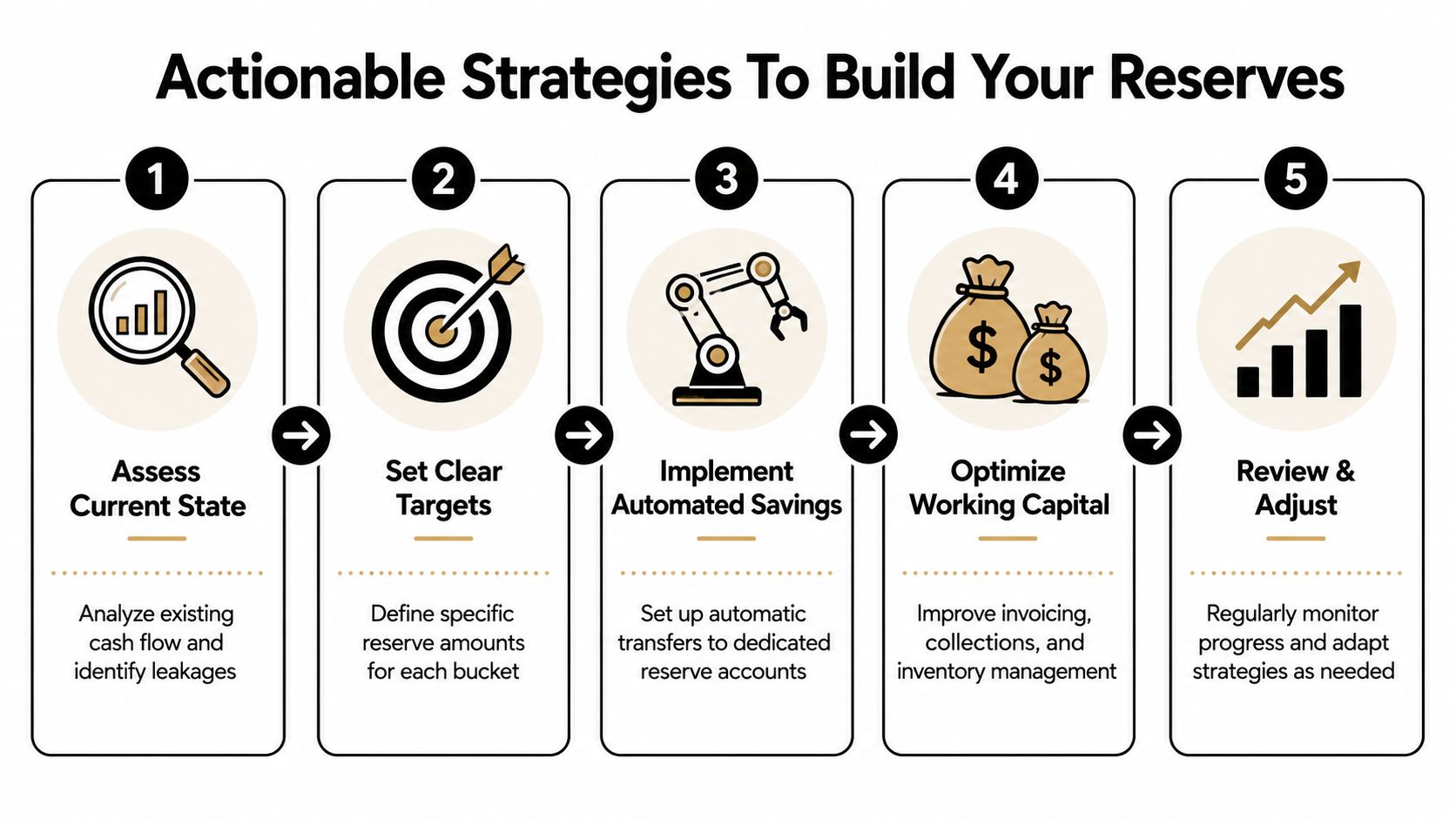

Actionable Strategies To Build Your Reserves

A founder sees $180,000 in the bank after a strong sales month and assumes the business is finally breathing easier. Two weeks later, a supplier deposit for inbound stock goes out, BAS is due, several large invoices are still unpaid, and the balance is back under pressure. The problem was never the month. It was the timing.

Reserves are built by redesigning that timing, not by hoping discipline improves under stress. For Australian SMEs, especially wholesale, retail, trade supply, and ecommerce businesses, reserve building works best when it sits inside day-to-day cash flow management. Inventory buying, debtor collections, tax set-asides, supplier terms, and debt repayments all shape how much cash can stay in the business.

Build reserves from operating decisions

Start with the points where cash gets trapped or disappears.

If margin is too thin, reserve building turns into a constant uphill fight. Price reviews matter. So does enforcing minimum order values, checking freight recovery, and cutting work that consumes cash without leaving enough behind. I see founders chase savings targets while ignoring the fact that one underpriced product line can undo months of effort.

Then look at the cash conversion cycle. Faster invoicing and tighter follow-up reduce the amount of buffer you need because fewer dollars are stuck in debtors at the wrong time. If collections are slipping, tighten your accounts receivable management process before you decide the answer is a bigger reserve target.

Inventory-heavy businesses need a harder conversation. Stock can protect sales, but it also swallows liquidity. Review reorder points, supplier minimums, aged inventory, and the actual cash cost of buying too early. Dead stock is not a reserve. It is cash with a label on it.

Supplier terms deserve the same scrutiny. Extending payment timing by even a modest amount can create room to build reserves without cutting growth. The trade-off is relationship risk. Good operators ask for terms with a clear payment plan behind them, not as a last-minute reaction when the account is already tight.

For operators who want more practical collection and liquidity tactics, you can also get HireAccountants' cash flow guide for ideas on speeding up receivables and tightening spending controls.

Ask, “What stops cash from staying in the business?”

Put reserve building on rails

Good intentions do not survive a busy month. Systems do.

Set up the process so reserves grow in the background while you run the business:

Split cash by purpose. Keep separate targets for operating buffer, tax, and true contingency cash.

Automate transfers. Sweep a fixed amount or percentage out of trading cash each week, not just when the account looks healthy.

Use stock triggers. Tie larger purchase orders to forecasted cash position, upcoming tax dates, and expected collections.

Review payments weekly. Challenge discretionary spend, early supplier payments, and owner drawings that erode the buffer.

Match debt decisions to liquidity pressure. Paying debt down can be smart, but not if it leaves the business exposed before payroll, BAS, or a major stock buy.

Get support where the process is weak. Nexist's cash flow support includes forecasting and identifying profit leaks across pricing, inventory, and receivables.

The goal is not to park a static pile of cash and hope it is enough. The goal is to create a business that keeps producing surplus cash, protects it from timing shocks, and builds reserves without starving the parts of the operation that generate profit.

Reserve building is the outcome of better pricing, cleaner stock decisions, faster collections, controlled tax timing, and fewer reactive payments.

Protecting And Managing Your Cash Buffer

Once reserves exist, the next risk is treating them like spare cash.

That usually happens because the money sits in the same account as daily trading funds, or because no one has agreed when reserves may be used. Then a strong month arrives, the balance looks healthy, and the business ends up spending buffer cash on routine operating noise.

Hold cash with intent

A lot of reserve advice ignores one uncomfortable question. Should every extra dollar stay in cash?

Not always. In Australia, the trade-off is sharper because many founders are weighing liquidity against debt costs and available interest on cash. Guidance aimed at Australian businesses has pointed out that many articles tell owners to keep cash in reserve without properly comparing that choice against the cost of debt or rising interest income, and that with the RBA cash rate at restrictive levels, the opportunity cost of idle cash is more visible (Finance Fight Club on cash reserves).

That means founders should decide where reserve cash sits based on purpose:

Operating buffer should stay highly accessible.

Emergency cash should be separate and low-friction to access.

Excess liquidity above target might be better used to reduce expensive debt or sit in a structure that preserves access while improving return.

If you run ecommerce, reserve protection also includes reducing avoidable cash erosion after the sale. Chargebacks can subtly damage liquidity, so this guide to ChargePay's chargeback management is worth a look if disputes are eating into collected revenue.

Manage reserves like a live control system

Strong reserves need light governance, not complexity.

A monthly review should answer five plain questions:

Did the reserve balance move up or down?

Was any reserve cash used, and why?

Are debtors stretching beyond normal?

Is stock growing faster than sales?

Are we holding too much idle cash relative to debt cost?

If the business is under pressure, broaden that review into a simple cash dashboard. This piece on small business cash flow problems can help founders identify whether the issue sits in collections, margins, timing, or spending discipline.

The point isn't to admire the reserve. It's to use it as a signal. A falling buffer tells you something operational is changing, often before the P&L makes it obvious.

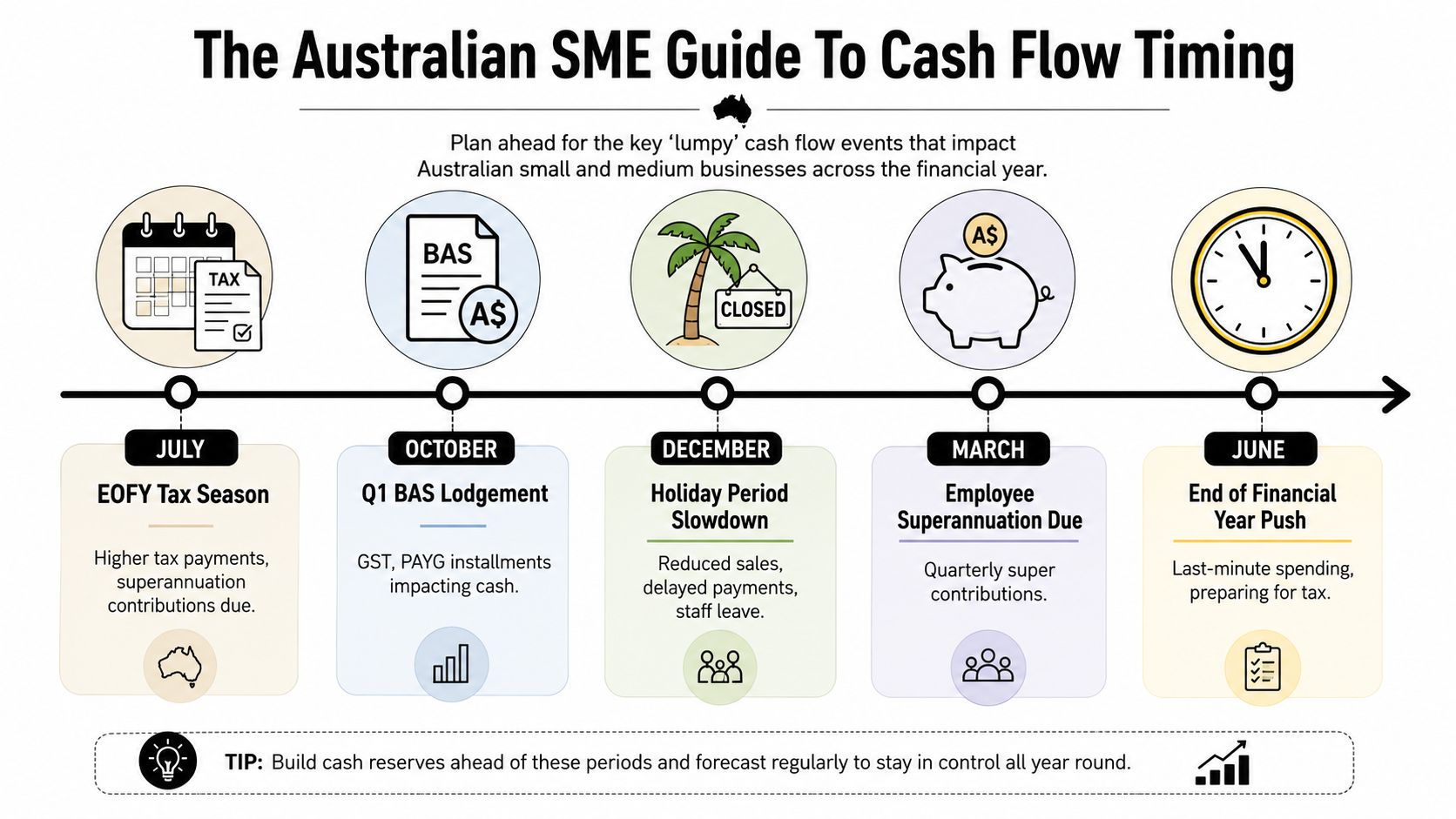

The Australian SME Guide To Cash Flow Timing

Generic reserve advice falls apart when it ignores the rhythm of Australian business payments.

For many SMEs, the biggest cash hits are not random. They're predictable, lumpy, and easy to underestimate when you only look at monthly averages. BAS, super, payroll obligations, supplier terms, annual renewals, holiday slowdowns, and year-end clean-up all create cliffs in the calendar.

Why timing hurts more than averages

A business can look profitable across the year and still fail on timing.

That's especially true when cash is tied up in inventory or debtors. Public discussion aimed at Australian SMEs has also highlighted that ASIC has warned small-business insolvency risk remains high, which is why reserve sizing is less about a generic month count and more about how long the business can survive without debtor inflows or stock conversion (small-business cash reserves discussion referencing ASIC warning).

That's the critical point for stock-heavy businesses. You may be asset-rich on paper and cash-poor in practice.

What founders should map across the year

A useful reserve plan in Australia should map at least these recurring cash events:

Tax timing. BAS and other tax obligations need their own cash rhythm.

Super obligations. Don't let these build into an ugly quarter-end hit.

Seasonal dips. December, January, school holiday periods, or weather-driven slowdowns matter in many sectors.

Supplier buy-ins. Retail, wholesale, manufacturing, and hospitality often commit cash before revenue arrives.

Debtor lag. If customer payments drift during quieter periods, pressure compounds quickly.

If you want to get sharper on the mechanics behind this, understanding the cash conversion cycle helps connect stock days, debtor days, and creditor timing into one practical operating measure.

Average monthly cash needs can mislead you. The business feels the peaks and troughs, not the average.

Founders who plan by annual profit alone tend to get surprised. Founders who plan by timing usually see trouble earlier and need fewer emergency fixes.

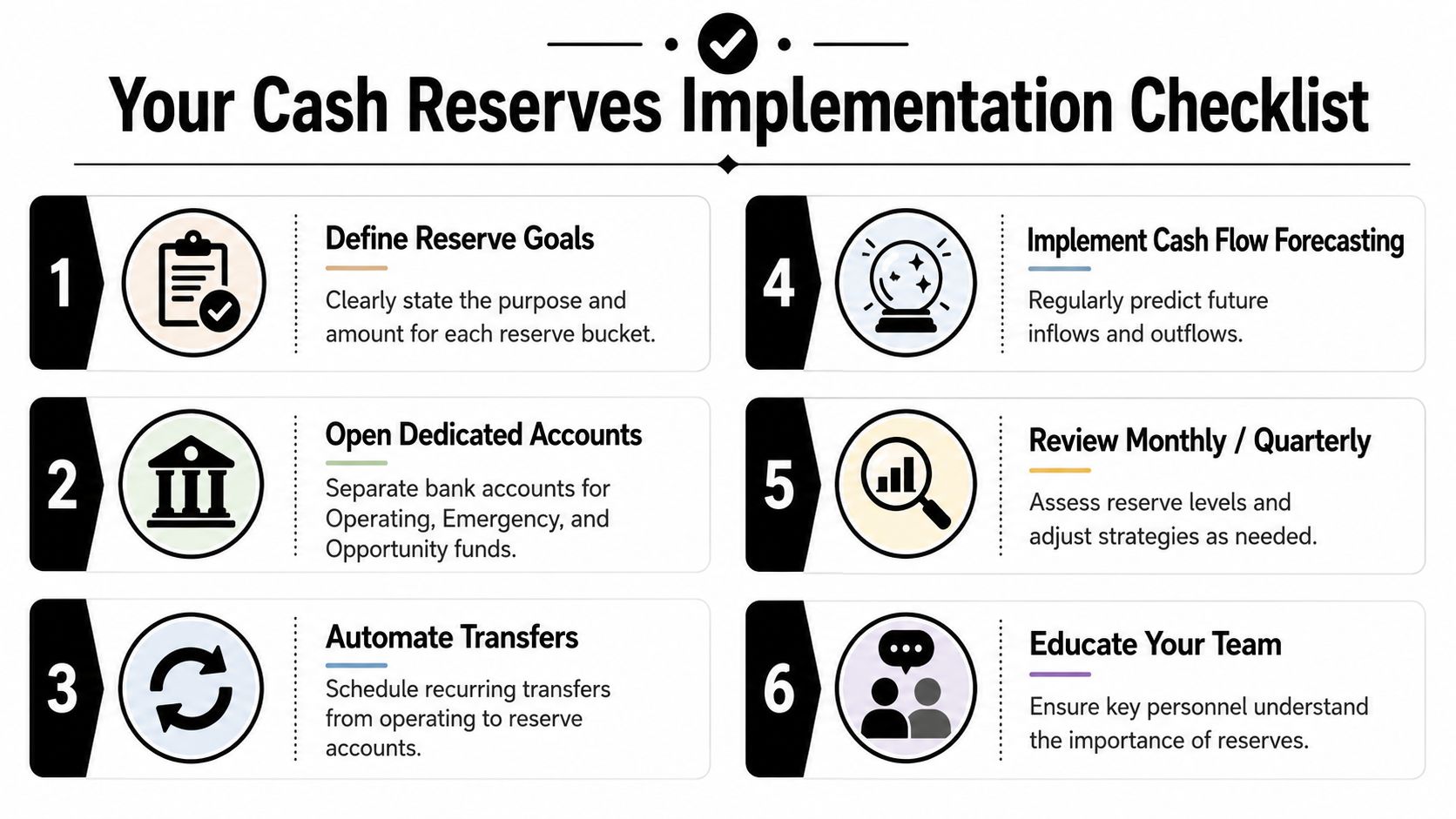

Your Cash Reserves Implementation Checklist

Cash reserves for business become real when they move from idea to routine. The first win isn't hitting the perfect number. It's creating structure so cash stops disappearing into the general account.

Use this as a practical first pass over the next quarter:

Define your reserve buckets. Split cash into operating, emergency, strategic, and tax categories.

Choose your calculation method. Use the expense model, revenue model, or preferably a live forecast if cash timing is uneven.

Open separate accounts. Don't leave reserve and tax cash mixed with trading funds.

Automate transfers. Remove willpower from the process.

Fix one working-capital constraint first. That might be overdue debtors, excess stock, weak invoicing, or poor supplier terms.

Review monthly. Check whether reserves are growing, shrinking, or being raided for routine costs.

Stress-test your timing. Ask how long the business could trade if major receipts slowed or stock took longer to convert.

Set rules for release. Decide in advance what qualifies as an emergency, what counts as an investment, and what should be funded from normal operations.

Most founders don't need more theory. They need a reserve framework they'll use when the pressure is on.

If you want a clearer view of how much cash your business should hold, where it's getting trapped, and how to build a reserve without starving growth, Nexist helps Australian founders put forecasting, working-capital control, and practical finance systems around the business so the cash position stops being a guessing game.

cash reserves for business, cash flow management, business finance Australia, sme financial health, virtual cfo

" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="dSFdkJotL" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="wscNJE44G" transform="translate(0 0.129)" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="sTpjGo1tb" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="s7ffpmKOD" transform="translate(0 0.129)" width="24px"/><g d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.000006px" id="D0ecaHEcW" transform="translate(0 0)" width="24px"><path d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z" fill="rgb(55, 184, 218)" height="24.000006px" id="IPLFE6zXx" width="24px"/><path d="M 4.02 0 L 0 0 L 0 12.092 L 4.02 12.092 Z" fill="rgb(255, 255, 255)" height="12.09201px" id="FWhtzAyuY" transform="translate(2.863 8.375)" width="4.02px"/><path d="M 2.274 0 C 0.899 0 0 0.904 0 2.089 C 0 3.25 0.871 4.179 2.221 4.179 L 2.247 4.179 C 3.648 4.179 4.521 3.25 4.521 2.089 C 4.495 0.904 3.649 0 2.274 0 Z" fill="rgb(255, 255, 255)" height="4.17876px" id="VmOsKv4kO" transform="translate(2.625 2.545)" width="4.52095px"/><path d="M 7.641 0 C 5.509 0 4.554 1.173 4.019 1.996 L 4.019 0.284 L 0 0.284 C 0.053 1.419 0 12.376 0 12.376 L 4.019 12.376 L 4.019 5.623 C 4.019 5.262 4.045 4.9 4.151 4.642 C 4.442 3.92 5.103 3.172 6.214 3.172 C 7.667 3.172 8.25 4.282 8.25 5.907 L 8.25 12.376 L 12.269 12.376 L 12.269 5.442 C 12.269 1.728 10.286 0 7.641 0 Z" fill="rgb(255, 255, 255)" height="12.37626px" id="n1XUbhaq0" transform="translate(9.105 8.09)" width="12.268830000000001px"/></g></g></g></g></svg>)