Quarterly Business Review: A Guide for Australian SMEs

Run a quarterly business review that drives growth. Our guide for Australian SMEs covers planning, agendas, KPIs, and follow-up for real cash-flow impact.

Ansh Malhotra

Your quarter ended. Revenue looked acceptable on paper, yet the bank balance feels tighter than it should. Stock is sitting too long, a few clients are stretching payment terms, the owner is still approving everything, and the so-called quarterly review is about to become another slide-reading exercise that changes nothing.

That's where most Australian SMEs go wrong with a quarterly business review. They treat it like a reporting ritual instead of a control system. A useful QBR doesn't just tell you what happened. It shows where cash is getting trapped, which operational bottlenecks are causing the leak, and what has to change over the next 90 days.

Table of Contents

Why Your Quarterly Review Meetings Are Failing

Most quarterly review meetings fail for a simple reason. They're built like corporate presentations, not operating reviews for lean businesses.

The pattern is familiar. Someone exports reports from Xero, MYOB, Cin7, Shopify, Deputy, Simpro, or a CRM. A deck gets stitched together the night before. People sit in a room, numbers get read aloud, everyone agrees there are “a few issues”, and the meeting ends without a clear list of decisions.

That isn't a quarterly business review. It's a retrospective with no control mechanism.

Australian SMEs usually need something sharper. Generic QBR advice often treats the meeting like an account review, but many local businesses need a cash-flow-first review that asks what's changing in working capital and how much cash is trapped. That matters because slow payment remains a major pressure on small business, as noted in guidance referencing the concerns repeatedly raised by the Australian Small Business and Family Enterprise Ombudsman through the cash-flow-first QBR discussion.

The real problem isn't lack of data

Most founders already have the numbers. What they don't have is a meeting structure that forces trade-offs.

A revenue-only review can miss the actual issue. Sales may be up while stock is ageing. Margin may look stable while labour inefficiency is eating delivery capacity. EBITDA may appear fine while debtor collections are slipping and the business is leaning harder on overdraft or owner stress to stay liquid.

Practical rule: If your quarterly review doesn't end with named owners, deadlines, and cash consequences, it was only a discussion.

The strongest QBRs I've seen in Australian SMEs are run as operating meetings with financial discipline. They focus on the handful of constraints that will affect the next quarter, not every metric someone can export.

If you want a useful reference point for the finance-first mindset behind that approach, Nexist's virtual CFO leadership background aligns closely with how experienced operators think about control, not just reporting.

What works instead

A useful QBR for an SME asks:

Where is cash tightening: Receivables, stock, payroll timing, supplier pressure, or weak conversion.

What is causing it: Process failure, pricing issue, owner bottleneck, forecasting miss, or team capacity.

What changes next quarter: One owner, one due date, one measurable operational shift per action.

That's the shift. Stop running a quarterly catch-up. Start running a 90-day control system.

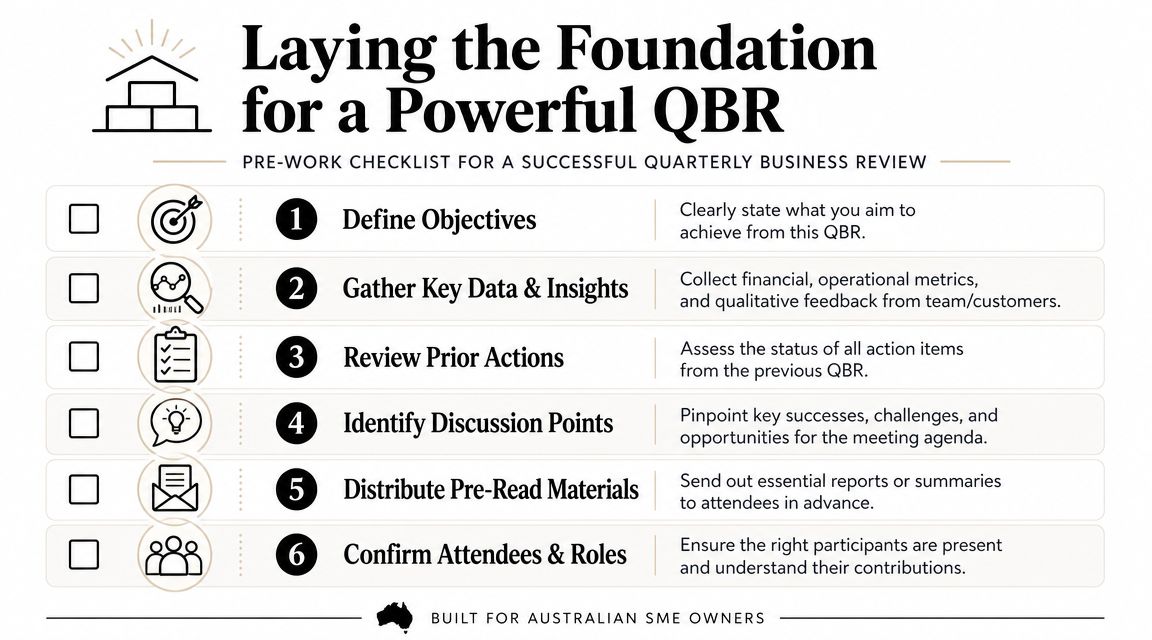

Laying the Foundation for a Powerful QBR

A strong quarterly business review is usually decided before the meeting starts. If the pre-work is weak, the discussion drifts. If the inputs are clean and the purpose is clear, decisions happen faster.

In Australia, the modern QBR is best understood as a 90-day management cadence, with a structured meeting each quarter to review prior-period results, compare trends, and set next-quarter priorities, as described in Australian QBR guidance. That cadence matters because founders need a fixed rhythm for review, reset, and accountability.

Set the purpose before you open a spreadsheet

Most businesses prepare the numbers first and ask questions later. Reverse that.

Decide what the meeting must resolve. For an inventory-heavy business, that may be excess stock, poor sell-through, and margin compression. For an agency, it may be utilisation, scope creep, and overdue invoices. For a trade business, it may be scheduling friction, rework, and WIP turning into delayed cash.

Use three pre-QBR questions:

What changed last quarter that affected cash or profit?

Which bottlenecks will hurt the next quarter if left alone?

What decisions must be made in the room, not after it?

That framing stops the session becoming a discovery meeting.

Bring the right people and give them pre-work

Too many attendees slows the room. Too few creates excuses later.

A founder-led SME usually needs the owner or GM, finance lead, operations lead, and whoever owns the main commercial lever for the quarter. That could be sales, delivery, procurement, or warehouse. If someone can't make a decision or doesn't own a key process, they probably don't need to be there for the full meeting.

The pre-read should be short and useful. Send it early enough that people can think, not just skim. Include:

A one-page executive summary: The headline result, the main misses, the major risks, and the few decisions required.

Core financial and operational data: Actual versus forecast, P&L summary, cash position, receivables ageing, stock position if relevant, and any key service or delivery metrics.

Status of last quarter's actions: Open, complete, blocked, or abandoned, with a reason.

Discussion points: The few issues that require judgement, not reporting.

The meeting should never be the first time people are seeing the numbers. It should be the first time they're making decisions from the numbers.

A practical way to improve attendance quality is to assign each participant a role in advance. One person owns the cash summary. Another explains operational variances. Another confirms whether previous actions were completed. That changes behaviour quickly because people arrive prepared to defend or explain.

If you're thinking more broadly about who should be in strategic financial conversations as the business grows, the lens used by a private wealth adviser is useful. It's the same principle. The right people in the room shape better decisions than a larger room full of observers.

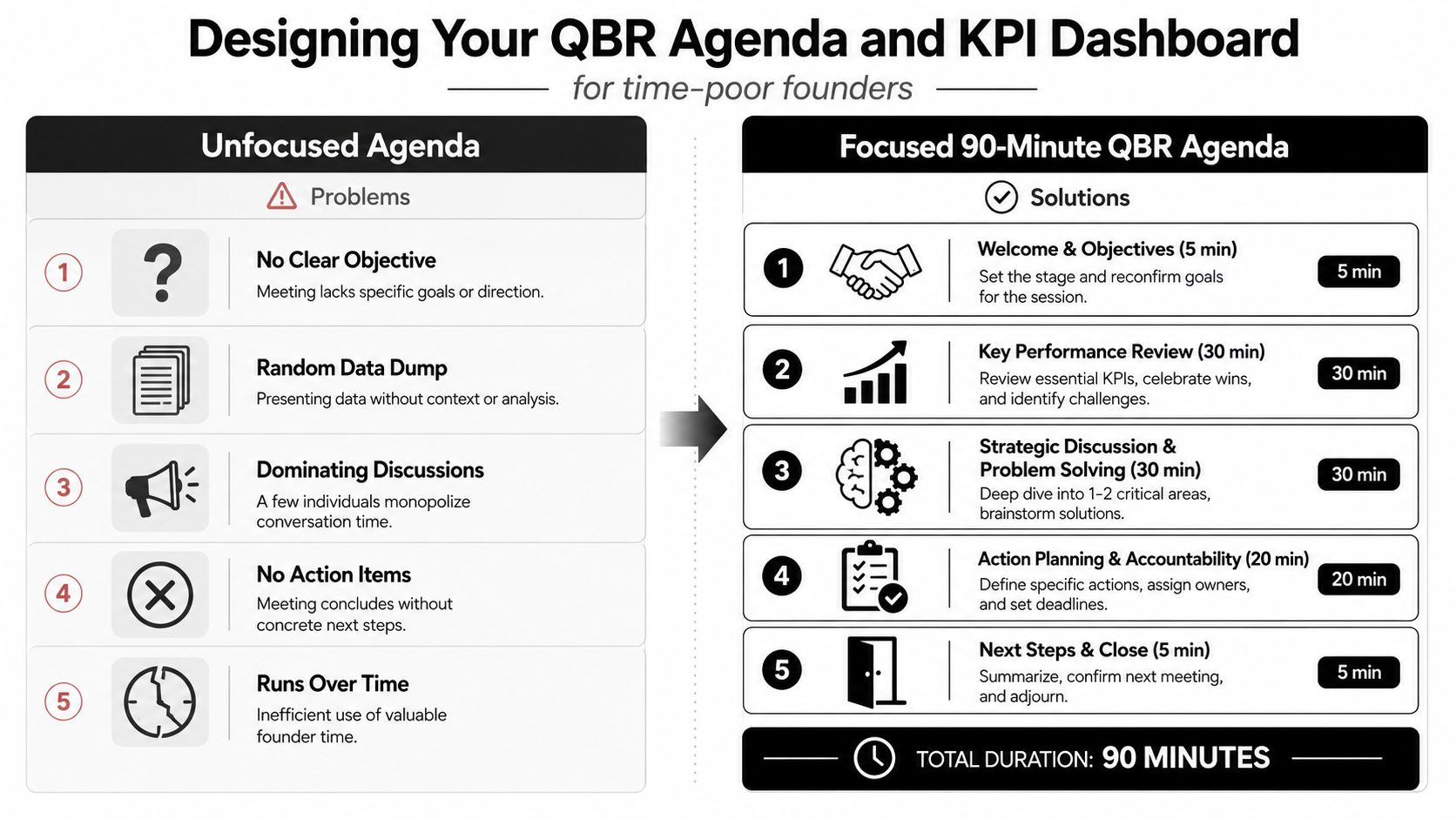

Designing Your QBR Agenda and KPI Dashboard

Founders don't need a long meeting. They need a meeting with sequencing. The wrong agenda creates noise. The right agenda creates decisions.

Australian-facing QBR guidance increasingly ties the review to measurable outcomes, including revenue performance, operational efficiency, sales outcomes, and product usage where relevant. It also highlights metrics such as product adoption and churn as early warning signs of revenue issues in customer-focused settings, which is why a finance-minded operator tracks throughput, connects it to outcomes, and fixes the bottleneck through a measurable-outcomes QBR approach.

A good agenda starts broad, goes narrow where required, and ends with commitments.

A practical agenda for time-poor founders

For most SMEs, a focused quarterly business review can fit inside 90 minutes if the pre-read is done properly.

A clean flow looks like this:

Agenda block | What happens | What to avoid |

|---|---|---|

Opening and objectives | Confirm the few decisions the meeting must make | Letting people reopen the whole agenda |

Scorecard review | Review the top-level business numbers and key variances | Reading every line item aloud |

Deep dive on constraints | Analyse the few issues actually driving the result | Turning the room into a blame session |

Decision and action setting | Confirm what changes next quarter, who owns it, and by when | Ending with vague agreement |

After the opening, keep the scorecard tight. If a metric doesn't affect cash, margin, delivery capacity, retention, or owner time, it probably doesn't belong on the first page.

A short explainer on how teams can approach business metrics more usefully sits well alongside this thinking in this guide to business performance indicators.

A visual walkthrough can help if your team is used to loose meetings rather than disciplined reviews.

Build a KPI dashboard that reflects your business model

The biggest dashboard mistake is copying another business's metrics.

A retailer, an agency, and an electrical contractor can all report “revenue”, but revenue won't tell each of them the same thing. The dashboard needs to reflect how cash is earned, where margin gets lost, and which process failures create pressure fastest.

Use a small set of KPIs in categories, not a giant list.

Metric Category | KPI | Inventory-Heavy Example (Retail/Ecomm) | Service Business Example (Agency/Consulting) | Trade Business Example (Construction/Electrical) |

|---|---|---|---|---|

Revenue quality | Sales outcome | Sales by channel and gross margin by product line | Revenue by client, project, or retainer type | Revenue by job type or crew |

Cash conversion | Collection performance | Debtor ageing by wholesale account or marketplace payout timing | Overdue invoices by client and payment terms | Progress claims outstanding and debtor follow-up |

Working capital | Stock or WIP pressure | Slow-moving stock, stockouts, and reorder issues | Unbilled WIP and delayed sign-off | WIP ageing, materials on hand, supplier timing |

Delivery efficiency | Operational throughput | Fulfilment errors, return patterns, picking friction | Utilisation, write-offs, and scope creep | Labour efficiency, scheduling gaps, rework |

Customer health | Retention or usage signal | Repeat purchase trends or underperforming categories | Client retention risk and engagement quality | Repeat client pipeline and service call quality |

Execution discipline | Initiative progress | Stock clean-up, pricing changes, supplier renegotiation | SOP rollout, team capacity fixes, invoicing discipline | Job costing controls, admin automation, quoting process |

The dashboard should answer two questions quickly. What happened? Why did it happen?

Decision filter: Every KPI on your QBR dashboard should lead to one of three outcomes. Keep doing it, fix it, or stop it.

That's why vanity metrics are dangerous. Website traffic without conversion context doesn't help much. Social engagement without margin impact doesn't deserve precious meeting time. Even total sales can mislead if the business had to hold too much stock or discount too heavily to get there.

Use trend views where possible, not one-off snapshots. A QBR is about movement across the quarter and what that movement implies for the next one.

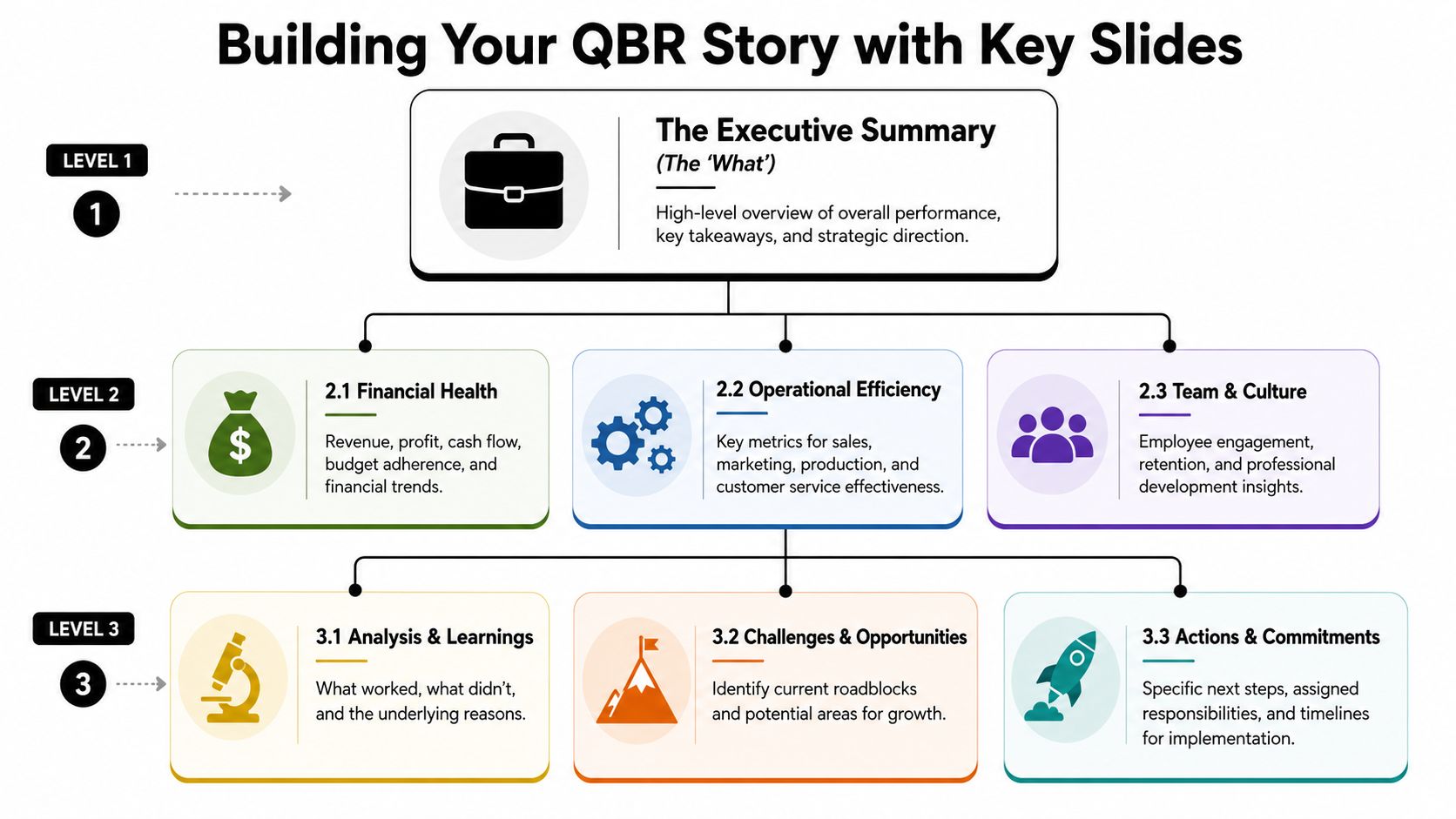

Building Your QBR Story with Key Slides

A good quarterly business review is a story about control. It explains where the business stands, what changed, why it changed, and what must happen next.

For Australian SMEs, the most defensible methodology is a cash-conversion review built around debtor days, inventory days, and creditor days, starting with actual versus forecast cash, then moving into aged receivables and slow-moving inventory before growth actions, according to this cash-conversion QBR method.

That gives you a better narrative than a standard pack of financial reports because it starts where pressure is felt first. In the bank account.

Start with cash, not commentary

If the first slide is a long summary paragraph, you've already lost the room.

Open with the clearest financial truth from the quarter. Was cash better or worse than forecast? Did receivables stretch? Did stock build faster than sales? Did payables timing support the business or create risk for the next quarter?

A practical first slide usually includes:

Actual versus forecast cash: Not just the variance, but the main reasons behind it.

Working capital pressure points: Aged debtors, inventory drag, supplier timing, or unbilled work.

Short outlook: What this means for the next quarter if nothing changes.

That first slide sets the tone. It stops the meeting from hiding behind revenue headlines.

The slides that move a meeting toward decisions

You don't need many slides. You need the right ones in the right order.

A clean finance-first sequence works well for most SMEs:

Executive summary

Use one page. Keep it brutal and readable.

Include the quarter result, the major variance, the biggest risk, the biggest opportunity, and the few decisions needed. If an executive can't understand the quarter from this page, the rest of the pack is probably too dense.

Cash conversion slide

This is the slide most generic QBR templates skip.

Show the movement in debtor days, inventory days, and creditor days. If you run a service business, adapt inventory thinking into WIP, deferred billing, or delayed job sign-off. The point is to show where operating activity is failing to convert into available cash.

When founders say, “We're busy but cash is tight,” this is usually the slide that explains why.

Actual versus forecast variance

Discipline becomes evident here.

Don't say revenue missed budget and move on. Split the miss into drivers. Was volume off? Was average sale lower? Were jobs delayed? Did discounting rise? Did labour overrun? Did collections slip? A useful variance slide names the operational causes, not just the accounting result.

Profit and loss deep dive

This is not a line-by-line tour of the ledger.

Focus on the few cost or margin movements that matter. For a product business, that may be discounting, freight, returns, or poor buying. For a service firm, it may be utilisation, subcontractor mix, or uncontrolled delivery hours. For trades, it may be scheduling inefficiency, quoting quality, or material recovery.

Top initiatives for next quarter

End with only a few priorities. Not ten.

List the initiative, the owner, the deadline, and the operating metric it should improve. If an initiative doesn't have a measurable operational effect, it's usually too vague to survive the quarter.

A QBR deck should feel less like finance theatre and more like a management instrument. That's when the story starts doing useful work.

Facilitating the Meeting for Real Decisions

Even a strong QBR pack can die in the room. The problem usually isn't the data. It's the way the discussion is managed.

Founders often let the meeting become too polite or too sprawling. Someone starts defending a variance. Someone else drifts into historical detail. A side debate starts on software, staffing, or one unhappy customer. Time disappears. The key decisions don't get made.

Set a decision standard at the start

Open the meeting with three things only. What decisions need to be made, what constraints matter most, and what won't be solved in this room.

That last point matters. Use a simple park board on a whiteboard, in Notion, in ClickUp, or even in the meeting notes. If a discussion is important but not central to the quarter's decisions, park it and assign it later.

Useful opening phrases:

“We're here to decide, not just review.”

“If this issue needs a separate working session, it goes on the park board.”

“Let's stay with causes we can control in the next quarter.”

Those lines sound simple, but they reset the tone fast.

Keep debate honest and useful

A good quarterly business review needs challenge. It doesn't need theatre.

Ask questions that force root-cause thinking:

What changed in the process, not just in the number?

Is this a one-off event or a repeating pattern?

What owner behaviour is still creating friction here?

If we do nothing, what problem gets worse next quarter?

Don't let people hide behind broad language like “market conditions”, “team capacity”, or “timing issues” unless they can explain the operational mechanism underneath.

A few facilitation habits work well in SME environments:

Cut narrative drift: If someone is retelling the quarter, ask for the decision implication.

Separate signal from exception: One bad week doesn't always justify a strategic change.

Push for a single owner: Shared ownership usually means no ownership.

Test realism: If an action depends on the founder doing everything personally, it probably won't happen.

The final part of the meeting should sound like commitment, not commentary. Who owns it. What changes. When it gets reviewed.

The best facilitators also watch energy. If the room is bogged down on one issue, summarise the options, ask for a call, and move on. A QBR isn't the place to solve every operational detail. It's the place to make the few decisions that propel the next quarter.

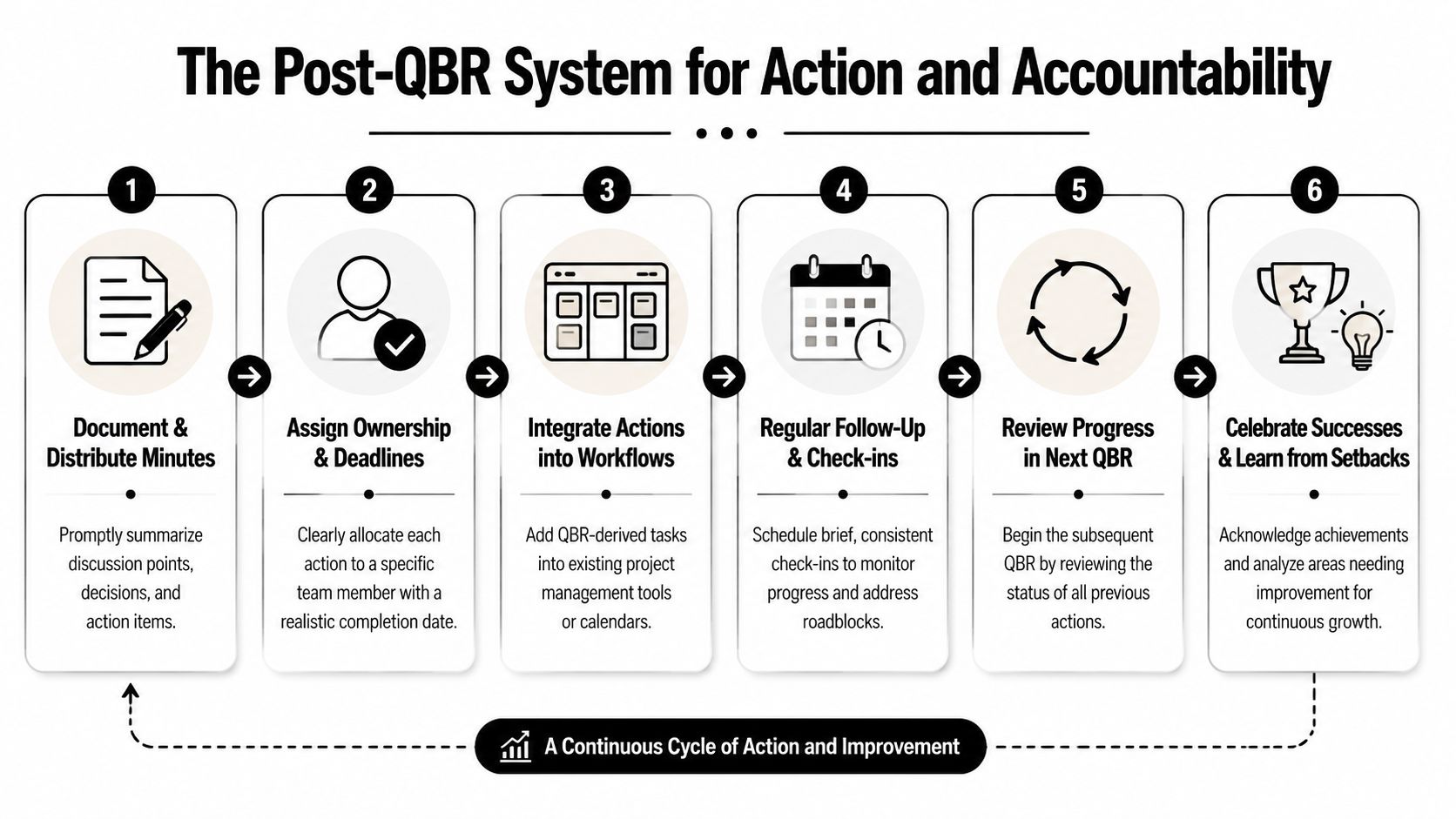

The Post-QBR System for Action and Accountability

Most businesses don't fail at reviewing. They fail at follow-through.

The core issue is the system and execution gap. Many QBR templates focus on reviewing the last quarter but don't ask whether the business has the SOPs, automation, or owner capacity to execute. A better question for Australian founders is which 1–3 bottlenecks are consuming the most time and creating the largest profit leak, as outlined in this system-and-execution-gap perspective.

That's why the post-QBR system matters more than the meeting notes.

Turn decisions into a one-page action plan

Right after the meeting, reduce everything into one page. Not a long memo. Not a buried document.

That page should include:

Top priorities: Only the few initiatives that matter this quarter.

Key actions: The practical tasks required to move each priority.

Single owner: One person accountable for progress.

Deadline: A real date, not “this quarter”.

Measure of movement: The operational indicator that should change if the action works.

A simple example helps.

Priority | Action | Owner | Deadline | Measure |

|---|---|---|---|---|

Improve collections discipline | Review overdue accounts weekly and escalate disputed invoices within a fixed process | Finance lead | Set during QBR | Reduction in overdue receivables pressure |

Reduce stock drag | Identify slow-moving SKUs and create clearance, bundling, or purchasing changes | Operations or inventory owner | Set during QBR | Better stock movement and less cash tied up |

Remove owner bottleneck | Shift approval or admin tasks into SOPs and team roles | Founder with ops lead | Set during QBR | Less founder intervention and faster execution |

Many businesses often overcomplicate things. They build a strategic plan when what they needed was a short operating plan.

Close the execution gap before the next quarter slips away

Your quarterly business review only works if it shows up in weekly rhythm.

That means the action plan has to move into the tools the team already uses. If your business runs on Asana, ClickUp, Monday.com, Trello, or a shared Teams planner, put the actions there immediately. If the business uses weekly huddles, add a standing QBR actions check-in. If the founder runs everything from a notebook, at least convert the commitments into a visible tracker that others can follow.

The check-in rhythm should be light but consistent:

Weekly: Are actions moving, blocked, or off track?

Mid-quarter: Do any actions need to be revised because assumptions changed?

Next QBR opening: Start by reviewing the status of the previous quarter's commitments.

A recurring problem discussed for three quarters is no longer a strategy issue. It's an execution failure.

One more rule matters here. Don't overload the quarter. Most SMEs get more traction from a few hard priorities executed properly than from a long list of initiatives that all stall halfway through.

The businesses that improve fastest aren't always the ones with the smartest dashboards. They're the ones that take a clear quarterly view, identify the few constraints that matter, and then build enough discipline to fix them.

If your quarterly business review keeps ending in discussion rather than action, Nexist helps Australian founders turn finance data into a practical operating system for cash flow, margin, and execution. If you want a sharper view of profit leaks, working capital pressure, and the few changes that would put more cash in the bank next quarter, it's worth starting with a conversation.

quarterly business review, business planning, sme guide australia, kpi dashboard, cash flow management

" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="dSFdkJotL" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="wscNJE44G" transform="translate(0 0.129)" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="sTpjGo1tb" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="s7ffpmKOD" transform="translate(0 0.129)" width="24px"/><g d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.000006px" id="D0ecaHEcW" transform="translate(0 0)" width="24px"><path d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z" fill="rgb(55, 184, 218)" height="24.000006px" id="IPLFE6zXx" width="24px"/><path d="M 4.02 0 L 0 0 L 0 12.092 L 4.02 12.092 Z" fill="rgb(255, 255, 255)" height="12.09201px" id="FWhtzAyuY" transform="translate(2.863 8.375)" width="4.02px"/><path d="M 2.274 0 C 0.899 0 0 0.904 0 2.089 C 0 3.25 0.871 4.179 2.221 4.179 L 2.247 4.179 C 3.648 4.179 4.521 3.25 4.521 2.089 C 4.495 0.904 3.649 0 2.274 0 Z" fill="rgb(255, 255, 255)" height="4.17876px" id="VmOsKv4kO" transform="translate(2.625 2.545)" width="4.52095px"/><path d="M 7.641 0 C 5.509 0 4.554 1.173 4.019 1.996 L 4.019 0.284 L 0 0.284 C 0.053 1.419 0 12.376 0 12.376 L 4.019 12.376 L 4.019 5.623 C 4.019 5.262 4.045 4.9 4.151 4.642 C 4.442 3.92 5.103 3.172 6.214 3.172 C 7.667 3.172 8.25 4.282 8.25 5.907 L 8.25 12.376 L 12.269 12.376 L 12.269 5.442 C 12.269 1.728 10.286 0 7.641 0 Z" fill="rgb(255, 255, 255)" height="12.37626px" id="n1XUbhaq0" transform="translate(9.105 8.09)" width="12.268830000000001px"/></g></g></g></g></svg>)