Division 296 Calculator: Estimate Your Super Tax 2026

Use our Division 296 calculator to estimate 2026 super tax on balances >$3M. Learn the formula, examples, and impact for Australian founders.

Ansh Malhotra

You check your super statement after a strong year in the business and the number jumps out. It's larger than it used to be, larger than many Australians ever reach, and suddenly it doesn't feel like a passive retirement account anymore. It feels like another balance sheet that needs active management.

That shift matters because Division 296 turns a high super balance into a planning issue, not just a reporting issue. If you're a founder, an owner-operator, or someone building wealth through a mix of business profits, property and super, a division 296 calculator helps answer a practical question: what could this mean for your future tax, liquidity and timing decisions?

Most founders don't need more theory. They need to know whether they're anywhere near the line, how the calculation works, and what decisions they should revisit before the first assessment year. If you're already juggling payroll, debt, stock, margins and personal wealth, this is another item that's easy to leave for later. That's usually a mistake. Tax changes rarely stay boxed inside tax. They flow into contribution strategy, exit timing, SMSF asset choices and personal cash flow.

Table of Contents

Your Super Balance Is High Is That a Problem?

You sell part of the business, top up super as part of the broader wealth plan, and for a while it feels like a tidy tax outcome. Then the balance moves past the point where super stops being a low-maintenance bucket and starts affecting cash flow planning, liquidity, and even the timing of an exit. That is the main issue founders need to focus on.

For Australian founders, Division 296 targets very large super balances, with the core threshold set at $3 million in total superannuation balance. Under the framework outlined by SuperGuide's summary of Division 296, the tax applies at 15% to the portion of earnings attributable to the balance above $3 million, with an additional 10% on the portion above $10 million. In practical terms, balances well above the line can face a heavier tax drag inside a structure many people assumed would stay concessionally taxed.

The tax issue is rarely the headline number on its own. The founder question is whether your super settings still fit the rest of your balance sheet.

Why founders should care before the first assessment

The first assessment is expected to be based on earnings for the 2026/27 financial year, as noted earlier in ORDS' calculator guidance. That gives founders time to plan, but only if they treat super as part of the broader capital strategy now.

High-balance super rarely happens by accident for business owners. It usually follows a specific event or a run of decisions. A business sale. Strong asset growth inside an SMSF. A restructure. Larger contributions over time. Property held in super that has appreciated faster than expected.

Each of those decisions can be sensible in isolation. Together, they can create a tax position that changes how much wealth you want locked inside super versus held where you have easier access to cash.

Practical rule: if your super is already close to the line, model the effect before you make a major business or investment move. After the year closes, your options are narrower.

I see founders make one planning mistake repeatedly. They separate business strategy from personal wealth strategy too aggressively. That works for management accounts. It does not work when a tax tied to your super balance can affect retirement funding, SMSF asset mix, estate planning, and how much liquidity you need outside super to stay flexible.

If you are already reviewing broader tax issues, keep them in proportion. Questions like medical expenses and tax claims in Australia can help tidy up annual returns. Division 296 sits at a different level. It can influence where you hold assets and when you realise gains.

What a division 296 calculator is really for

A division 296 calculator is a planning tool, not just a tax estimator.

Used properly, it helps answer three commercial questions:

Are you likely to be caught by the threshold?

How exposed are you if markets rise or a large contribution lands at the wrong time?

Which decisions deserve scenario modelling before you act?

That last point is where founders get the most value. A useful estimate can change how you think about contributions, pension commencements, asset sales inside an SMSF, and whether part of your long-term wealth should sit outside super for flexibility.

For a founder, the calculator earns its keep when it turns a policy proposal into a decision about timing, structure, and access to cash.

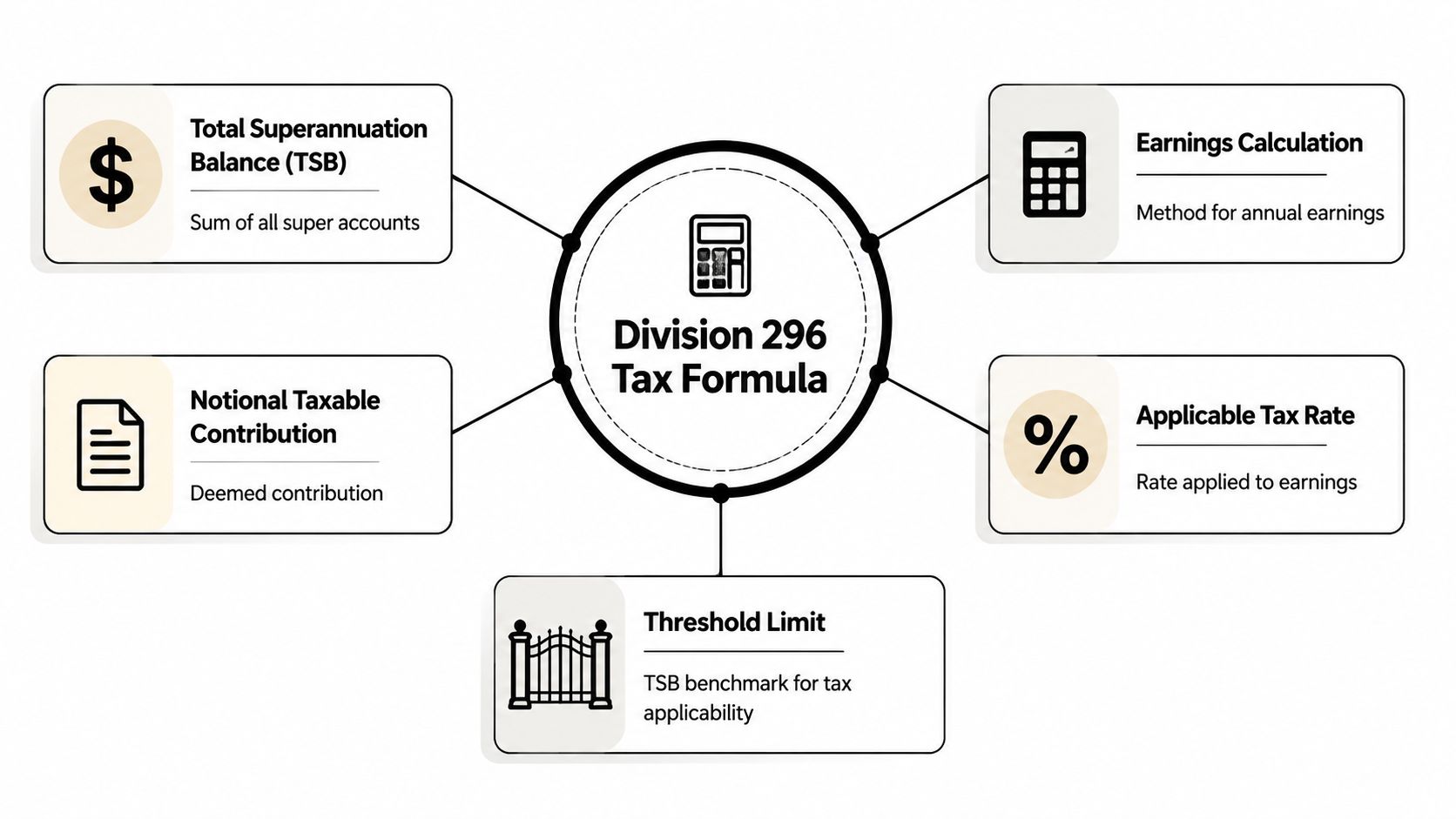

Understanding the Division 296 Tax Formula

A founder can have a strong year on paper and still misread their Division 296 exposure. I see this when an SMSF holds business property, private assets have been sold, or large concessional and non-concessional contributions hit near year end. The portfolio result looks clear enough. The tax formula does not use that number on its own.

What the threshold means

The threshold is not a switch that taxes your entire super balance once you cross $3 million. It only pulls part of your super earnings into the calculation. The higher your balance sits above the line, the larger the share of earnings that can be attributed to that excess.

That distinction matters in practice. A founder with a balance just over the threshold faces a very different outcome from someone well above it, even if both funds report similar investment returns for the year. The formula is trying to measure how much of your super growth relates to the portion above the cap, not impose a flat surcharge on the whole account.

This is why small balance changes can matter around key decision points. A one-off contribution, a revaluation of business real property in an SMSF, or a strong year in listed markets can push more of the balance into the taxable zone than expected.

Why earnings are the hard part

The earnings piece catches people out because it is broader than portfolio performance. For Division 296 purposes, the working concept is the movement in your total super balance over the year, adjusted for money going in and out. In plain terms, contributions are stripped out and withdrawals are added back so the calculation focuses on wealth growth inside super rather than simple cash movement.

SMSF practitioners often express the starting point this way: end of year total super balance, minus start of year total super balance, minus net contributions, plus withdrawals. Cloudvara's guide to tax software is useful if you are trying to pull those records together across fund reports, accounting files, and trustee documents before modelling scenarios.

That is where founders need to slow down. If your SMSF holds lumpy assets such as property, unlisted investments, or business premises, valuation timing can affect the result. If you started a pension, took a withdrawal, or made a late contribution after a liquidity event, the balance movement by itself will not tell you enough.

Component | Plain English meaning |

|---|---|

TSB | Your total superannuation balance across relevant super interests |

Opening and closing position | The balances used as the reference points for the year |

Contributions | Money added that may need to be adjusted out of the earnings base |

Withdrawals | Money taken out that may need to be added back for calculation purposes |

Threshold test | Whether enough of the balance sits above the line to trigger attribution |

A division 296 calculator works more like a reconciliation tool than an investment return estimate. It measures the change in super wealth after adjusting for cash flows.

Indexation is part of the framework, but the founder takeaway is simpler than the legislative detail. Thresholds are intended to move over time rather than stay frozen forever. That matters for long-range planning because a tax that seems irrelevant today can become relevant later through market growth alone, especially if your wealth strategy concentrates heavily inside super.

For business owners, the formula is not just a tax rule. It affects where you hold future assets, how much liquidity you keep outside super, and whether an SMSF remains the right home for specific investments after a growth event or exit.

How to Manually Calculate Your Estimated Tax

A founder sells shares, makes a contribution to super, starts a pension, and then sees markets lift before 30 June. The year-end balance looks strong, but that headline number does not tell you what Division 296 exposure may look like. The manual estimate matters because it helps you decide whether to keep more liquidity outside super, defer a contribution decision, or prepare for a personal tax bill that arrives separately from fund cash flow.

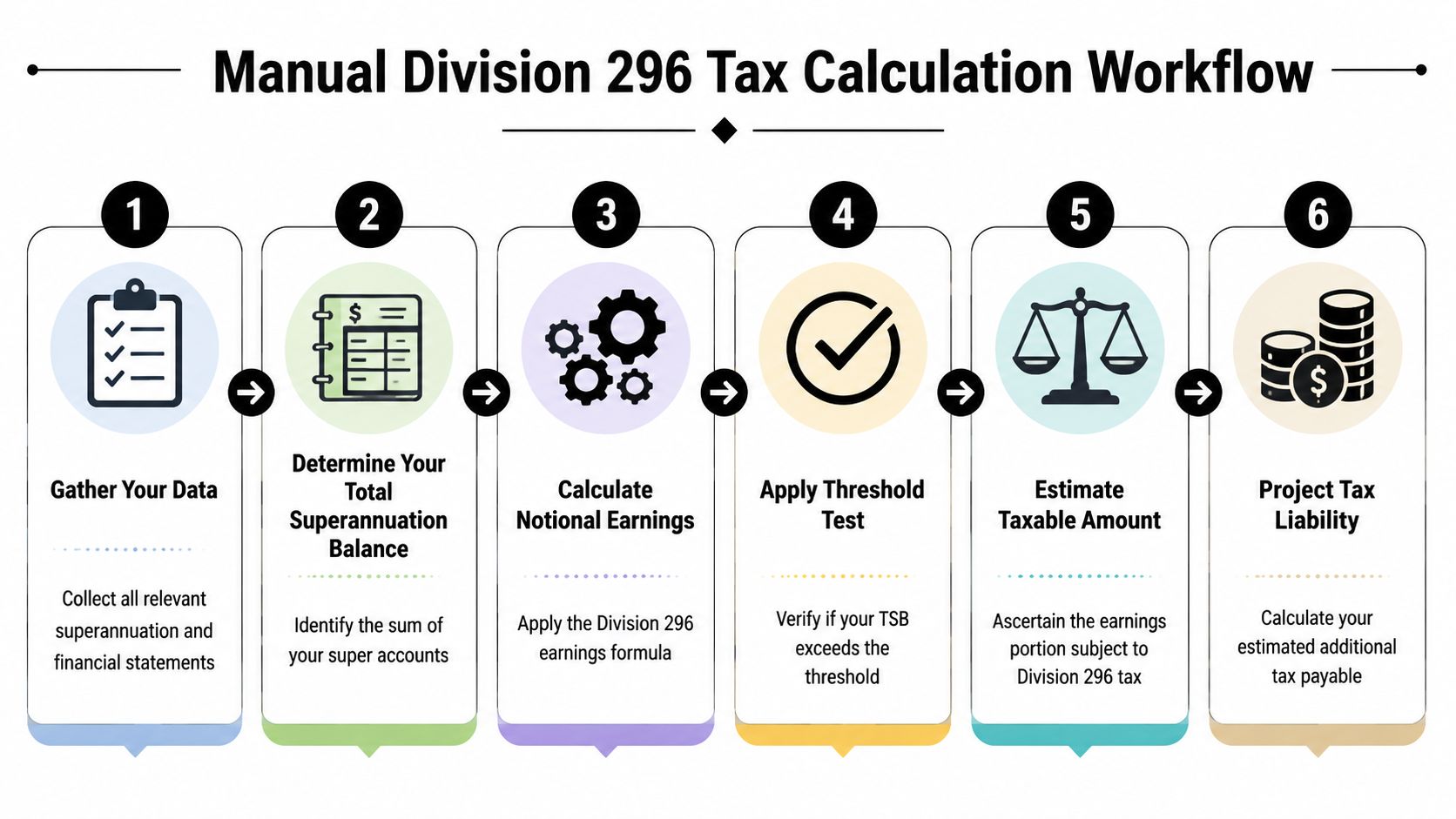

Gather the figures before you touch a calculator

Start with source documents. A rough estimate built from memory is how founders understate withdrawals, miss contribution timing, or use stale SMSF asset values.

Pull together records that show:

Your opening and closing super balances for the relevant period

Contributions made during the year, especially if they came from irregular founder income

Withdrawals or pension payments

SMSF asset movements, if your fund holds direct property, shares, business premises or other assets where valuation timing matters

For some founders, that means exporting data from an industry fund portal. For others, it means trustee reports, accounting files, pension schedules and valuation papers for an SMSF.

If your records sit across Xero, a document vault, fund reports and accountant emails, organise them before you calculate anything. Founders tightening the broader finance stack often benefit from tools that centralise tax records and compliance workflows. For that purpose, Cloudvara's guide to tax software is a useful starting point because it focuses on the operating side of tax data as well as filing.

Work through the estimate in order

Once the records are assembled, run the estimate in sequence.

Confirm your total superannuation balance

Check whether your balance is above the relevant threshold. If it is below, Division 296 may not apply for that year.Estimate the earnings base

Use the broad calculation framework noted earlier. Start with the change in your total super balance across the year, then adjust for contributions and withdrawals. In practice, that means end-of-year TSB minus start-of-year TSB, minus net contributions, plus withdrawals.Work out the proportion above the threshold

At this stage, many manual estimates go wrong. The tax is aimed at the share of earnings attributable to the excess over the threshold, not the whole earnings figure.Apply the relevant tax rate

After you have the attributed earnings amount, apply the Division 296 rate to estimate the extra tax exposure.

Use a worksheet like this to keep the logic clean:

Step | What you're checking |

|---|---|

Balance test | Are you above the threshold at all? |

Earnings test | What was the adjusted increase in super wealth? |

Attribution test | What share of that earnings figure belongs to the excess balance? |

Tax estimate | What extra tax could arise from that attributed amount? |

A manual estimate is most useful when it feeds a decision. If the number is modest, the issue may be simple cash flow planning. If the number is large, the key question is whether your current wealth structure still fits your next stage, especially after a capital raise, business sale, or major shift in SMSF assets.

Later in the process, this explainer may help clarify some of the concepts in video form:

Common mistake: using the investment return shown on a fund report as if it were the Division 296 earnings figure. That shortcut can miss the effect of contributions, withdrawals and valuation timing.

Manual estimates are useful for planning conversations. They do not replace specific advice where SMSFs, business property, large contributions or irregular cash movements are involved.

Worked Examples for Common Founder Scenarios

A founder sells shares, moves from a salary-and-dividends pattern to a large pool of investable capital, and suddenly super is no longer a background account. It becomes part of a bigger allocation decision alongside trust assets, private investments, property and cash reserved for tax, living costs and the next deal.

As noted earlier, the first assessments are expected to be based on earnings from the 2026/27 financial year, and balances as of 30 June 2027 are expected to be the first officially measured against the threshold. For founders, that timing matters because planning is more useful before a liquidity event, contribution, or valuation shift than after the balance has already moved.

Founder after a business exit

After an exit, the calculator answers a specific planning question. How much of future super earnings could fall into the extra tax if the balance sits above the threshold?

That sounds narrow, but the decision behind it is much broader. A founder with sale proceeds often has competing uses for capital. Some money may stay outside super for personal liquidity, some may back a new venture, and some may be allocated for long-term investing. The tax estimate helps compare those options, especially where access to cash matters as much as after-tax return.

I usually see better decisions when founders model more than one year. A single estimate can understate the effect of continued growth, later contributions, or a second liquidity event. A simple forecast tied to a few business performance indicators often gives a better picture than a one-off tax number because it connects super planning to the operating reality of the business and the founder's future cash needs.

Business premises inside an SMSF

An SMSF that owns the trading premises can still make sense. It can align rent, long-term asset ownership and retirement planning. The trade-off is that valuation growth does not always arrive with spare cash.

A property-heavy fund can show a stronger balance because the premises have appreciated, while the fund itself remains relatively illiquid. That matters for Division 296 planning. The projected tax may be acceptable in theory, but the practical question is whether the fund has enough cash flow to meet obligations without forcing awkward asset sales or changing investment settings at the wrong time.

Founders in this position need tighter records, cleaner valuations and regular trustee reviews. Good specialised SMSF accounting helps because the technical tax estimate is only part of the job. The harder part is keeping valuations, rent flows, pension settings and liquidity aligned so the structure still works under pressure.

Property inside super can be tax-efficient and strategically useful. It can also create a paper gain without giving the fund much room to pay real liabilities.

Founder approaching the line

Some of the best planning work happens before the balance clearly exceeds the threshold.

A founder approaching the line still has options. Future wealth might be building through company profits, contributions, investment growth or retained cash that has not yet been deployed. At that stage, the calculator is less about today's liability and more about direction. If the current path continues, where does the balance land, what does that imply for future tax, and does that still fit the founder's wider wealth plan?

Useful discussions here usually focus on a few practical decisions:

Contribution pattern: whether new money should keep flowing into super at the same pace

Asset location: whether the highest-growth assets still belong inside super

Timing: whether planned actions should occur before the first assessment period is expected to apply

Liquidity: how much capital should remain personally accessible for business volatility, investment opportunities or family use

The common thread across these scenarios is straightforward. A Division 296 calculator is most useful when it informs a capital allocation decision. Founders rarely need another abstract tax example. They need to know what the projected number means for liquidity, flexibility and long-term wealth after the business changes shape.

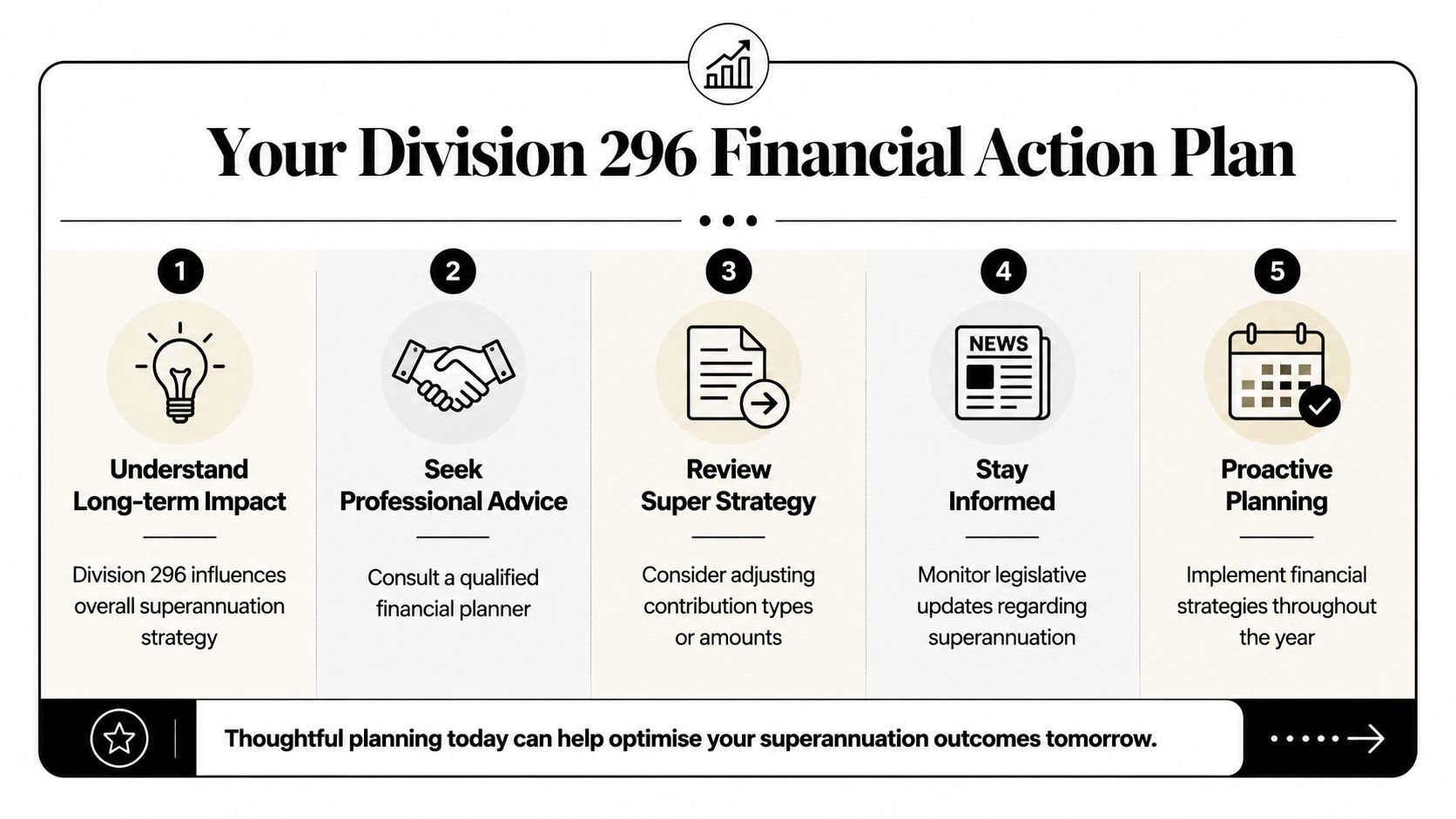

Strategic Planning for High Super Balances

Paying the future tax isn't the only decision. Often it isn't even the main one. The core issue is whether your current wealth structure still fits the next stage of your life and business.

The real decision is not the tax bill

Founders tend to ask, “How much will this cost me?” That's fair, but it's incomplete. The better question is, “What does this change make less efficient, and what does it leave untouched?”

A high super balance can still be useful. The problem comes when owners keep feeding a structure by habit, even after the trade-offs have changed. Super remains attractive for many reasons, but once Division 296 enters the picture, you need a more deliberate framework for where future capital goes.

A practical review usually looks at decisions such as:

Contribution strategy: Continuing the same pattern may no longer be the default best move.

Asset placement: Growth assets inside super may produce a different long-term outcome than income-focused assets, depending on your wider structure.

Cash outside super: More accessible capital can matter if your business is cyclical, acquisitive or still funding growth.

Exit proceeds: If a liquidity event is on the horizon, the sequence of decisions matters more than people expect.

What tends to work better

The founders who handle this well don't chase a single “hack”. They build a joined-up plan across business, personal cash flow and retirement strategy.

That can include reviewing whether different family members should hold wealth in different structures, whether the SMSF still holds the right assets, and whether personal liquidity should be strengthened before locking more money into super. If an SMSF is involved, specialist support matters due to the overlap of tax, compliance, and asset strategy. For technical implementation support, specialised SMSF accounting can be valuable when your fund structure is no longer simple.

A founder should also look at Division 296 through the same lens used for business reporting. If your business already tracks cash conversion, gross margin, debtor days and stock turn, your personal wealth plan should have an equivalent dashboard. The discipline behind business performance indicators that actually drive decisions applies here too. What gets measured tends to get managed.

Strategic question | Why it matters |

|---|---|

Do I still want more wealth inside super? | Tax settings and access rules may no longer align with your goals |

Do I have enough personal liquidity? | Tax planning is weaker when every decision assumes perfect cash timing |

Are my SMSF assets still appropriate? | Illiquid or lumpy assets can create planning pressure |

Am I modelling future years? | One-year estimates rarely capture founder reality |

Founders rarely regret modelling early. They often regret assuming a structure will stay optimal just because it worked in the previous stage.

What doesn't work is treating Division 296 as a small technical nuisance while leaving the bigger capital allocation decisions untouched. That approach usually preserves convenience, not outcomes.

Beyond the Calculator Your Next Financial Steps

A division 296 calculator gives you an estimate. It doesn't give you a financial operating system.

That's the gap many founders run into. They can identify that a future tax issue exists, but they haven't connected it to drawdown strategy, business exit timing, debt reduction, family wealth structures or the amount of cash they want available outside super. The number is useful. The surrounding decisions matter more.

Turn an estimate into a plan

A practical next step is to turn the estimate into a short planning file that covers:

Your likely super position over the next few years

Expected business events, including distributions, sale activity or major investment decisions

Cash flow implications if tax becomes payable

Asset location choices across super and non-super structures

Review dates before key year-end points

That kind of document is simple, but it changes behaviour. It moves Division 296 out of the “I should ask someone later” category and into active wealth management.

This broader perspective is why many founders eventually need more than isolated tax advice. They need integrated oversight across tax, forecasting and private wealth decisions. If you're assessing how those pieces fit together, it's also worth reading about the role of a private wealth advisor for business owners, because Division 296 usually sits inside a larger capital strategy.

The founders who stay in control are usually the ones who treat tax changes as signals. Not signals to panic. Signals to review structure, timing and liquidity before the rules force their hand.

If you want help turning a Division 296 estimate into a broader business and personal finance plan, Nexist can help. Their virtual CFO approach is built for founders who need more than a one-off calculation. It connects cash flow, forecasting, tax visibility and strategic decision-making so you can protect wealth without losing focus on the business. A practical first move is to book a Business Scorecard session and get clear on where your financial structure stands now.

division 296 calculator, division 296 tax, superannuation tax, australian sme finance, virtual cfo

" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="dSFdkJotL" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="wscNJE44G" transform="translate(0 0.129)" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="sTpjGo1tb" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="s7ffpmKOD" transform="translate(0 0.129)" width="24px"/><g d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.000006px" id="D0ecaHEcW" transform="translate(0 0)" width="24px"><path d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z" fill="rgb(55, 184, 218)" height="24.000006px" id="IPLFE6zXx" width="24px"/><path d="M 4.02 0 L 0 0 L 0 12.092 L 4.02 12.092 Z" fill="rgb(255, 255, 255)" height="12.09201px" id="FWhtzAyuY" transform="translate(2.863 8.375)" width="4.02px"/><path d="M 2.274 0 C 0.899 0 0 0.904 0 2.089 C 0 3.25 0.871 4.179 2.221 4.179 L 2.247 4.179 C 3.648 4.179 4.521 3.25 4.521 2.089 C 4.495 0.904 3.649 0 2.274 0 Z" fill="rgb(255, 255, 255)" height="4.17876px" id="VmOsKv4kO" transform="translate(2.625 2.545)" width="4.52095px"/><path d="M 7.641 0 C 5.509 0 4.554 1.173 4.019 1.996 L 4.019 0.284 L 0 0.284 C 0.053 1.419 0 12.376 0 12.376 L 4.019 12.376 L 4.019 5.623 C 4.019 5.262 4.045 4.9 4.151 4.642 C 4.442 3.92 5.103 3.172 6.214 3.172 C 7.667 3.172 8.25 4.282 8.25 5.907 L 8.25 12.376 L 12.269 12.376 L 12.269 5.442 C 12.269 1.728 10.286 0 7.641 0 Z" fill="rgb(255, 255, 255)" height="12.37626px" id="n1XUbhaq0" transform="translate(9.105 8.09)" width="12.268830000000001px"/></g></g></g></g></svg>)