Finding Your Private Wealth Advisor: Founder's Guide

Unlock success! Our guide helps Australian founders find a private wealth advisor. Learn about services, fees, & how it connects to your virtual CFO.

Ansh Malhotra

Your business throws off profit. The management reports are sharper than they were two years ago. You know your gross margin, your cash conversion cycle and which product line funds the rest. But once money leaves the business, the picture gets messy.

A founder's personal finances often look like this: a home loan structured years ago, a growing offset account, an SMSF no one has reviewed properly, a few direct shares, maybe an investment property, maybe a trust, and a vague idea that “I'll sort it out after the next growth phase”. Meanwhile, most of your wealth still sits inside one illiquid asset. Your company.

That mismatch is common. Strong business finance doesn't automatically create strong personal wealth management. It just creates the opportunity for it. A private wealth advisor helps turn that opportunity into an actual strategy, especially when your life now sits at the intersection of business cash flow, tax, family, succession and long-term investing.

Table of Contents

Your Business Is Thriving But Your Personal Wealth Is Not

A founder can run a disciplined business and still have disorganised personal wealth. That sounds contradictory until you see how it happens.

Inside the company, there's structure. BAS is lodged. Payroll runs. Debtors are chased. Stock is measured. Forecasts get reviewed. Outside the company, decisions are often made in fragments. A dividend goes out with no long-term deployment plan. A trust distribution solves one year's tax issue but creates another planning question. Extra cash lands in the offset because it feels safer than making the wrong move.

That gap usually widens during growth. The business demands attention, so personal wealth gets treated as a side project. Founders tell themselves they'll focus on it after the next hire, the next acquisition, the next funding round, the next EOFY.

What this often looks like in practice

Cash rich but unclear: You've built liquidity, but you don't know how much should remain accessible versus invested.

Asset heavy but concentrated: Most wealth is tied to the company, yet your personal plan assumes that value is stable and realisable.

Tax aware but not tax coordinated: Your accountant handles compliance well, but no one is connecting business structure, super, trusts and personal goals into one strategy.

Retirement discussed but not modelled: You know you should plan, but there's no real framework for when work slows, income changes or an exit happens.

Founders rarely have an income problem first. They have a coordination problem.

A private wealth advisor becomes useful. Not because you've joined some elite club, but because your financial life has become too interconnected for ad hoc decisions.

The right advisor works on your personal balance sheet the way a strong finance lead works on your business. They help define liquidity, risk, tax positioning, investment structure, succession intent and family priorities. Without that, even a profitable business can leave the owner exposed, overconcentrated and oddly uncertain about what all the hard work is building toward.

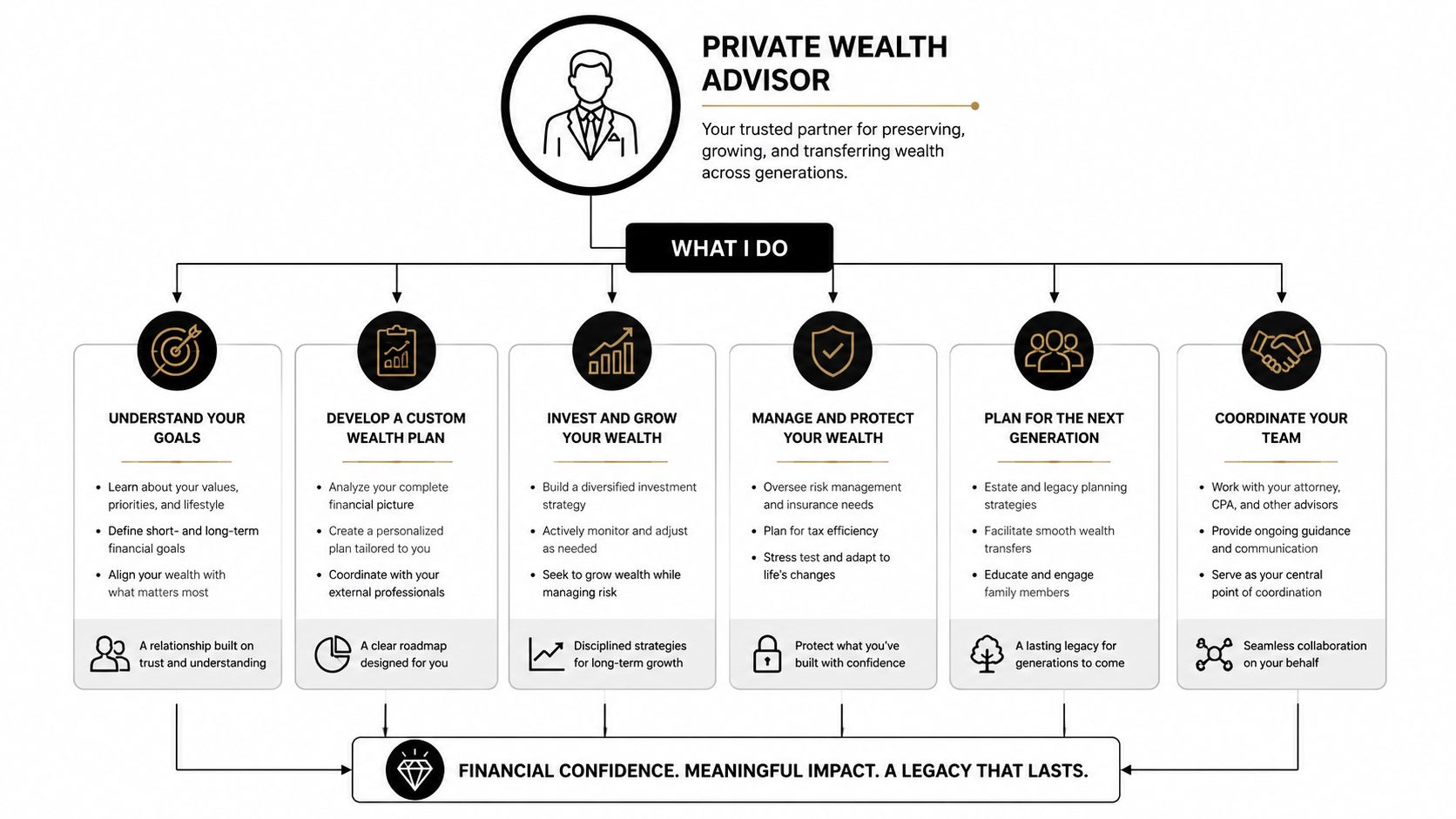

What a Private Wealth Advisor Actually Does

A founder can run a $5 million, $10 million or $20 million business and still have a personal financial setup that is scattered. Cash sits in the wrong entities. Super is treated separately from the rest of the balance sheet. Insurance was put in place years ago and never reviewed. No one has tied future business value to a personal plan.

That is the role of a private wealth advisor.

A good one helps turn fragmented personal finances into a coordinated system. For founders, that usually means working across investments, super, trusts, debt, property, insurance, estate planning and the likely timing and shape of future business proceeds. The point is not more paperwork. The point is better decisions.

From a vCFO perspective, this is familiar territory. In a business, strong financial control starts with visibility, cash discipline, forecasting and clear decision rules. Personal wealth needs the same treatment once the company starts producing meaningful surplus cash or equity value. Founders who want more context on how these issues connect across business and personal finance can browse the Nexist insights library for founder finance strategy.

They organise the founder's personal balance sheet

Most founders do not need someone to pitch products. They need someone to answer practical questions clearly.

How much cash should stay liquid outside the business?

How much risk already sits inside the company?

Should surplus funds go to debt reduction, super, family trusts, market investments or reserve capital for future tax?

If an exit happens in three years rather than ten, what changes now?

A capable private wealth advisor helps set those priorities and keep them aligned. In practical terms, that often includes:

Investment strategy: Building a portfolio around your existing concentration risk. If most of your wealth depends on one private company, your external investments should play a different role.

Liquidity planning: Setting aside accessible capital for tax, family spending, lending covenants, business shocks and personal opportunities, instead of leaving the decision to habit.

SMSF coordination: Aligning contributions, asset location and drawdown planning with your broader family position.

Estate planning input: Working with legal advisers so ownership structures, nominations and succession intentions are clear and usable.

Tax coordination: Working alongside your accountant so distributions, realised gains, debt arrangements and super decisions support the same plan.

There are trade-offs in every one of those calls. More liquidity usually means lower long-term returns. More tax efficiency can mean more structural complexity. More growth exposure can improve outcomes over time, but it can also leave a founder overexposed if the business hits a rough patch at the same time markets fall.

Good advice is strategic, not product-first

Weak advice starts with an investment menu. Strong advice starts with your cash flows, entity structure, concentration risk and likely future events.

That matters for founders because personal wealth decisions are rarely isolated. A plan that looks sensible in a generic retirement model can fail quickly if you are funding expansion, buying out a shareholder, moving from PAYG income to trust distributions, or preparing the company for sale. The advisor's job is to build around those realities, not ignore them.

The better advisers also show their work. They explain why assets are held in specific entities, what liquidity buffer is being protected, how tax has been considered, and what assumptions sit behind the plan. If responsible investing matters to you, ask how the screening process is measured and how portfolio construction changes as a result. ASIC has also warned issuers and advisers against vague or overstated sustainability claims in Information Sheet 271 on how to avoid greenwashing when offering or promoting sustainability-related products.

Practical rule: If an advisor cannot explain how your investments, tax position, liquidity needs and business timeline fit together, you are not getting integrated private wealth advice.

Founders also need an advisor who respects the line between business finance and personal strategy. Your accountant handles compliance. Your lawyer handles legal documents. Your vCFO improves operating control and cash visibility inside the business. A private wealth advisor should connect the owner-side decisions around those inputs, not pretend to replace every other specialist.

For a broader perspective on how long-term planning is shaped by tax policy as well as structure, EndureGo Tax's views on wealth tax planning are worth reading.

The Advisor Landscape A Clear Comparison

Founders often hire the wrong financial professional because the titles sound interchangeable. They aren't.

Why founders get the roles confused

Envision a medical team. Your bookkeeper handles routine financial administration. Your accountant deals with compliance, tax reporting and some structuring. A virtual CFO acts like the doctor managing the operating health of the business. A private wealth advisor is closer to the specialist looking after the owner's long-term financial position outside, and alongside, the company.

The confusion usually starts when one professional stretches beyond their lane. An accountant may comment on investments. An advisor may discuss business cash flow without really understanding operations. A founder then assumes one person can cover everything.

Usually, they can't.

If you want broader perspective on how founder finance issues connect across growth, operations and strategy, the Nexist insights library is a useful starting point.

Advisor Role Comparison

Role | Primary Focus | Typical Client | Key Deliverable |

|---|---|---|---|

Private wealth advisor | Personal wealth strategy across investments, liquidity, tax coordination, estate considerations and family goals | Founders, executives, families with growing financial complexity | An integrated personal wealth plan |

Financial planner | Personal goals such as retirement, insurance, super and general investment planning | Individuals and households needing broad advice | A plan for personal financial goals |

Wealth manager | Portfolio management and broader asset oversight, often through an institutional or boutique model | Clients wanting ongoing investment oversight | Managed portfolio and asset allocation |

Virtual CFO | Business cash flow, margins, forecasting, working capital, pricing, systems and decision support | SMEs and growth-stage companies | Financial control and operating decisions inside the business |

The key difference for founders is scope. A virtual CFO works on the engine that produces wealth. A private wealth advisor works on what happens to that wealth once it reaches your personal world.

That distinction matters when your company is profitable but unpredictable, or valuable but illiquid. In those cases, business finance and personal finance must talk to each other, but they still need different specialists.

The right setup isn't one advisor doing everything. It's each expert knowing where their job starts and where it stops.

Key Triggers for Hiring a Private Wealth Advisor

Most founders wait too long because they think private wealth advice starts at some magic net worth figure. In practice, complexity is the primary trigger.

Complexity matters more than a wealth threshold

A lot of content in this category still speaks almost exclusively to very high net worth households. That misses most business owners. Existing content targets HNWIs with A$5M+ assets, ignoring the 99.8% of Australian businesses operating as SMEs, where 60% of owners lack formal succession planning, leading to a 30% business value loss on transfer, based on the underserved-founder analysis cited here.

That's exactly why founders shouldn't use a prestige threshold as the test. If your financial decisions now affect family security, tax exposure, ownership structure and future exit options, you're already in territory where a private wealth advisor can add value.

The founder situations that usually justify advice

Some triggers are obvious. Others sneak up on you.

You've started taking more cash out of the business than you spend personally

Once surplus cash begins to accumulate outside working capital requirements, “leave it in the bank” stops being a strategy. You need a deployment plan.Your wealth is concentrated in one operating asset

Many founders look diversified because they own a business, property and some super. Economically, they're still highly concentrated. Their future depends on one company, one sector or one sale event.You're approaching a liquidity event

Selling a division, bringing in investors, buying out a shareholder or preparing for a full exit all create decisions that should be made before money lands, not after.Your structures have multiplied

Once you're juggling company income, trusts, super and personal debt, the cost of uncoordinated decisions rises fast. Each move may be sensible in isolation and poor in combination.Family and succession questions are no longer theoretical

If a partner, children or future successors will be affected by your business wealth, advice needs to move beyond investment selection.

A founder doesn't need to arrive with a polished family office. But they do need clean financial inputs. That means reliable business numbers, clear drawings policy, visibility on tax liabilities and realistic cash flow forecasting. Without those, even a good advisor will be forced to plan around guesswork.

How to Evaluate and Interview Your Future Advisor

A founder walks into a first meeting with clean business numbers, a growing cash reserve, a trust structure, and no clear personal wealth plan. That meeting can save years of drift, or waste an hour on portfolio jargon that ignores how founder money behaves.

What to test in the first meeting

The first interview is not about being impressed. It is about finding out whether the advisor understands the gap between a successful SME and a well-structured personal balance sheet.

A good private wealth advisor should be able to work from founder facts. Irregular drawings. Capital tied up in the company. Tax obligations that arrive in lumps. Family goals that compete with reinvestment plans. If they default straight to risk profiling and model portfolios, they are starting too far down the process.

Listen closely to their questions. Strong advisors ask how cash moves through the business, how much of your wealth is still trapped in equity, what personal spending needs to be funded outside the company, and which decisions depend on a future sale, dividend stream, or property purchase. That line of questioning matters because personal wealth strategy for founders only works when the business engine is understood first.

Communication matters as much as technical skill. You do not need someone with the same background as you. You do need someone who can speak clearly, deal well with complexity, and show sound judgement around founder-specific trade-offs. If you want a sense of how this kind of commercially grounded advice is approached, review Neha Malhotra's founder finance background.

For a broader checklist on the selection process, Wealth Collective's advisor guide is a useful companion piece.

Questions that reveal whether they understand founders

Use questions that force specifics, not polished generalities.

How do you treat my business equity when setting my personal asset allocation?

If they focus only on liquid investments, they are ignoring the main source of your wealth and risk.How do you coordinate with my accountant on trust distributions, super contributions and tax timing?

Good advice requires cooperation across roles. It should not create silos.How would you plan my personal liquidity if the business has a weak quarter or needs extra capital?

This shows whether they understand that founder cash flow can tighten quickly, even in a profitable year.What work should happen before an exit or partial sale?

The strongest advisors have a view on pre-liquidity planning, not only what to do after cash arrives.How do you approach concentrated wealth?

Founders need a strategy that reflects one dominant operating asset, not a standard retail template.How do you charge, and what do I receive each quarter or each year?

Fee clarity matters. Vague service scopes turn into disappointment later.

I look for one more thing. Process.

Ask them to walk you through their planning sequence from first meeting to first recommendation. What information do they gather first? When do they ask for business financials? When does tax input come in? What events trigger a review? Advisors who can answer those questions clearly usually have a repeatable method. Advisors who cannot often rely on charisma and generic advice.

A strong first meeting leaves you with a clearer picture of how your business success can support personal wealth, without putting strain on the company that created it.

Common But Costly Pitfalls Founders Must Avoid

The biggest mistakes aren't usually dramatic. They're structural, and they compound over time.

Where advisory relationships go wrong

One common error is treating business and personal finances as separate planets. A founder commits to long-term investments personally, then needs liquidity because the business hits a rough patch, carries excess stock or faces a tax bill larger than expected. The problem isn't the investment itself. The problem is that no one mapped business volatility against personal commitments.

Another mistake is hiring an advisor who understands portfolios but not founder concentration risk. If most of your economic future sits in one private company, your liquid wealth strategy can't be built as if you were a salaried employee with diversified income. That mismatch creates false confidence.

Founders also get caught by polished advice that is generic. A neat slide deck, a standard risk profile and a basket of familiar funds can look professional while ignoring the essential work, which is coordination across entities, timing, liquidity and decision rights.

What better practice looks like

A better setup usually has these traits:

Shared visibility: Your advisor understands how you draw income, when tax liabilities arise and where business cash flow can become tight.

Clear boundaries: The accountant handles compliance, the advisor handles strategy, and both communicate.

Liquidity discipline: Cash reserved for tax, family needs or business support isn't accidentally treated as long-term capital.

Concentration awareness: Your company exposure is treated as central to the plan, not an afterthought.

Fee clarity: You understand whether you're paying for strategic advice, implementation, portfolio management, or all three.

Founders don't need more financial products. They need fewer blind spots.

One final trap is choosing purely on chemistry. Rapport matters, but it can't replace technical depth. The best relationships feel easy because the underlying work is hard and well done.

Uniting Your Business and Personal Finances The Nexist Advantage

A founder can finish a strong quarter, see profit on the P and L, and still feel unsure about buying a home, setting an investment plan, or increasing personal super contributions. I see this often. The business is working, but the path from company performance to personal wealth is still unclear.

Why better personal advice starts with cleaner business finance

Private wealth advice gets better when the underlying business numbers are usable. If reporting is late, margins shift without explanation, or owner drawings happen ad hoc, personal planning becomes guesswork. An advisor may still build a strategy, but the inputs are weak, so the recommendations stay conservative or miss the timing issues that matter to founders.

Clean finance changes that. With reliable forecasts, clearer working capital visibility, and a defined approach to paying yourself, decisions become easier. You can separate surplus cash from operating cash. You can see whether a lump sum belongs in tax reserves, debt reduction, the family balance sheet, or a long-term investment plan.

That distinction matters more for founders than salaried professionals. Personal wealth often depends on one operating asset, one income engine, and a small number of large decisions. If the business side is messy, the personal side stays reactive.

A stronger founder finance team

The best results usually come from two coordinated roles.

One focuses on the business. Better reporting, cleaner cash management, clearer forecasts, tighter control over margins and timing.

The other focuses on the owner. Investment structure, tax-aware wealth planning, estate considerations, and the shift from company value to personal financial security.

For founders who need the first part in place, financial control for growing businesses at Nexist gives private wealth advice something solid to work from. That means fewer decisions based on rough estimates and more decisions based on current numbers.

This is the gap many founders miss. They assume private wealth advice starts once they already look like a traditional high-net-worth client. In practice, the right time is often earlier, once the business has enough momentum to produce real surplus cash and enough complexity to justify structure. A vCFO helps create that starting point.

If your business is creating wealth but your personal finances still feel disconnected from it, fix the operating picture first. Then bring in the wealth advisor with clean data, a clearer pay strategy, and a realistic view of what the business can fund without strain. That is how business success starts showing up in personal wealth.

Written with the Outrank tool

private wealth advisor, wealth management, financial planning australia, virtual cfo, founder finances

" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="dSFdkJotL" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="wscNJE44G" transform="translate(0 0.129)" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="sTpjGo1tb" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="s7ffpmKOD" transform="translate(0 0.129)" width="24px"/><g d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.000006px" id="D0ecaHEcW" transform="translate(0 0)" width="24px"><path d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z" fill="rgb(55, 184, 218)" height="24.000006px" id="IPLFE6zXx" width="24px"/><path d="M 4.02 0 L 0 0 L 0 12.092 L 4.02 12.092 Z" fill="rgb(255, 255, 255)" height="12.09201px" id="FWhtzAyuY" transform="translate(2.863 8.375)" width="4.02px"/><path d="M 2.274 0 C 0.899 0 0 0.904 0 2.089 C 0 3.25 0.871 4.179 2.221 4.179 L 2.247 4.179 C 3.648 4.179 4.521 3.25 4.521 2.089 C 4.495 0.904 3.649 0 2.274 0 Z" fill="rgb(255, 255, 255)" height="4.17876px" id="VmOsKv4kO" transform="translate(2.625 2.545)" width="4.52095px"/><path d="M 7.641 0 C 5.509 0 4.554 1.173 4.019 1.996 L 4.019 0.284 L 0 0.284 C 0.053 1.419 0 12.376 0 12.376 L 4.019 12.376 L 4.019 5.623 C 4.019 5.262 4.045 4.9 4.151 4.642 C 4.442 3.92 5.103 3.172 6.214 3.172 C 7.667 3.172 8.25 4.282 8.25 5.907 L 8.25 12.376 L 12.269 12.376 L 12.269 5.442 C 12.269 1.728 10.286 0 7.641 0 Z" fill="rgb(255, 255, 255)" height="12.37626px" id="n1XUbhaq0" transform="translate(9.105 8.09)" width="12.268830000000001px"/></g></g></g></g></svg>)