Small Business Taxation: A 2026 Guide for Aussie SMEs

Master Australian small business taxation in 2026. Our guide covers GST, PAYG, income tax, and cash flow strategies to help you stay compliant and profitable.

Ansh Malhotra

It's late. BAS is due. Your bookkeeper has messaged twice, your payroll file still needs approval, and you're staring at a bank balance that looks healthy until you remember some of that cash isn't yours. It belongs to the ATO, your team's super fund, and the tax bill you've been meaning to plan for since July.

That's where most founders get small business taxation wrong. They treat it like paperwork. It isn't. It's a cash flow system. If you don't run that system properly, tax becomes the reason a profitable business feels broke.

I see the same pattern constantly. Owners work hard, sell well, and still get blindsided because they mix tax money with operating cash, delay recordkeeping, or assume quarterly habits are still safe when the rules have shifted. The fix is usually not more effort. It's better structure, tighter timing, and a sharper view of what the ATO prioritizes.

Table of Contents

Navigating the Tax Maze as a Business Owner

A founder I spoke with recently had sales coming in, staff getting paid, and work booked solid for weeks. From the outside, the business looked fine. Inside, it was chaos. Receipts were scattered across email, glovebox and phone photos. GST had been spent without realising it. Super was treated like a problem for later. Tax time felt like punishment for being busy.

That situation isn't unusual. It's what happens when the business grows faster than the finance habits behind it.

Most owners don't need more tax jargon. They need a clean operating rhythm. You need to know what money is collectible revenue, what money is tax, what money is payroll liability, and what money is free cash. Until those lines are clear, every hiring decision, stock order and wage increase gets riskier than it should be.

Practical rule: If you only find out what your tax position looks like when a deadline is close, you're already managing too late.

The good news is that Australian small business taxation becomes manageable when you stop seeing it as one giant problem. It's a set of separate obligations with different cash flow impacts. Some amounts you collect on behalf of the ATO. Some amounts you withhold from wages. Some amounts belong to future profit tax. Each needs its own process.

The owners who stay calm around tax usually do three things well:

Separate funds early: They move tax money out of the trading account before it gets swallowed by wages, stock or supplier payments.

Keep records live: They code transactions weekly, not months later when memory is unreliable.

Forecast pressure points: They look ahead to lodgements, payroll cycles and super obligations before cash gets tight.

That's the fundamental shift. Tax stops being a once-a-year scramble and becomes part of how you protect the business.

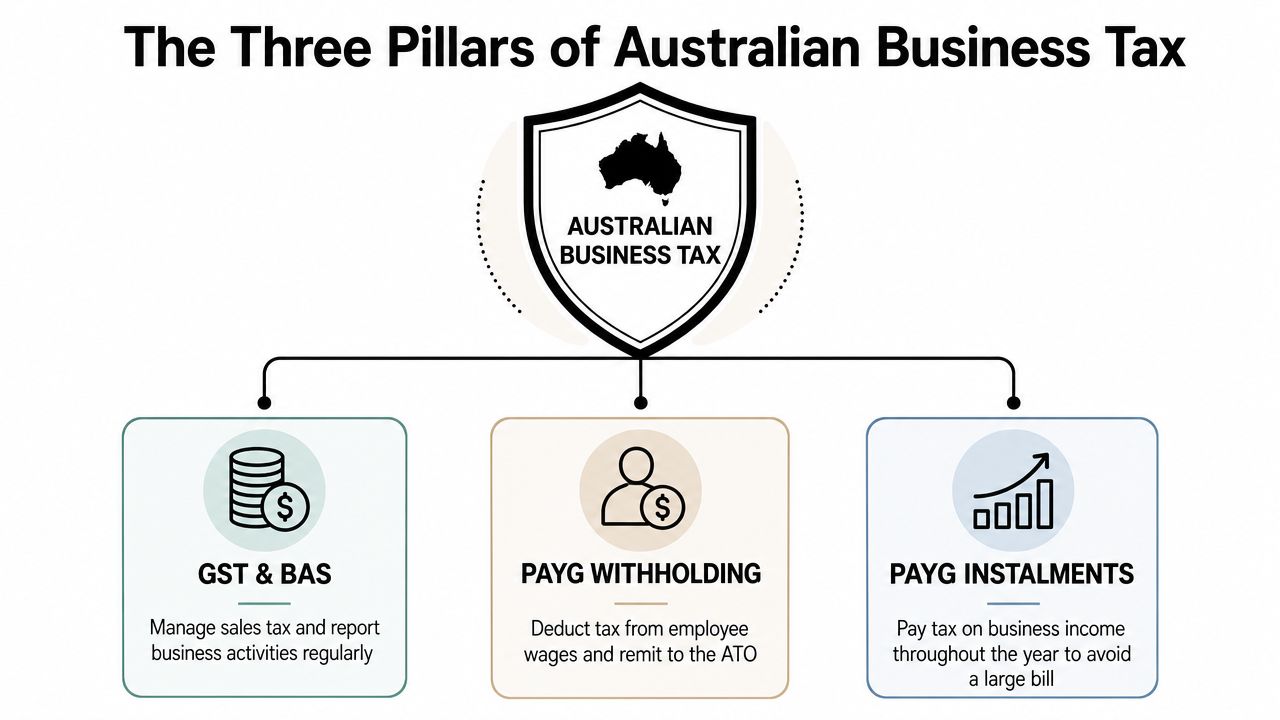

The Three Pillars of Australian Business Tax

The simplest way to understand small business taxation is to stop thinking about forms and start thinking about three buckets. Each bucket holds money with a different purpose. Confuse them, and your cash flow gets distorted fast.

Think in buckets, not in forms

The first bucket is GST and BAS. If you're charging GST on sales, some of the cash hitting your bank account isn't operating income. It's tax collected from customers. Treating it like spare cash is one of the fastest ways to create a BAS shock. Good operators move that amount aside as transactions happen, or at least reconcile it every week.

The second bucket is PAYG withholding. If you employ staff, you withhold tax from wages and remit it to the ATO. That money never belonged to the business. It passed through your payroll account on the way to the ATO. Founders who use it to smooth cash flow are borrowing from a deadline they already know is coming.

The third bucket is PAYG instalments or income tax provisioning. Often, businesses encounter difficulties here because profit on paper doesn't mean cash in bank. You can be profitable and still be stretched if margin is tied up in inventory, debtors or equipment. Income tax needs its own running provision, not a vague plan to “deal with it at year end”.

A practical setup looks like this:

Operating account: For normal trading activity.

Tax holding account: For GST, PAYG withholding and expected income tax.

Payroll clearing process: So wages and tax obligations are reconciled together, not separately.

GST is not your revenue. PAYG withholding is not your float. Tax provisions are not optional.

What the company tax rate really means

If you trade through a company, your tax rate matters because it affects what you retain after profit. For the 2023/2024 financial year, eligible base rate entities pay 25%, while the standard company tax rate is 30%. To qualify for the lower rate, the company must have aggregated turnover under $50 million and passive income must be less than 80% of total assessable income, according to iKeep's summary of Australian small business company tax rates.

That's not a minor detail. It affects how much profit stays inside the business for stock, debt reduction, hiring or owner distributions. But don't reduce this to a rate-chasing exercise. If your records are sloppy and your income mix is unclear, you can misclassify the business and create a bigger problem than the rate difference solves.

Here's a clearer perspective:

Tax area | What it means for cash flow | Owner priority |

|---|---|---|

GST and BAS | Cash collected that must be preserved | Reconcile weekly |

PAYG withholding | Payroll-linked tax liability | Lodge and remit on time |

Company income tax | Profit-based future cash outflow | Provision monthly |

Founders who master these buckets rarely say tax is confusing. They say it's disciplined. That's a better description.

Strategic Tax Planning for Healthy Cash Flow

If your tax plan begins in June, it's not a plan. It's a clean-up job.

Tax needs to sit inside your normal finance rhythm, alongside payroll, debtor collections and purchasing decisions. The businesses that stay in control don't just ask, “What tax will we owe?” They ask, “When will cash leave, and what do we need to change now so that payment doesn't hurt?”

Tax planning is a weekly finance habit

Strong tax planning is operational. It lives in your chart of accounts, your bank rules, your payroll workflow and your forecasting cadence. If you only talk tax with your accountant after the year has closed, you've left too much to chance.

Run these habits instead:

Provision from every sales cycle: Move estimated tax amounts into a separate account as money lands.

Review margins before year end: If profit is weaker than expected, fix pricing, stock purchasing or labour efficiency early.

Time major decisions carefully: Equipment purchases, bonuses, owner drawings and stock builds all change your cash position and often your tax position too.

Forecast obligations together: Don't model BAS, wages, super and income tax in separate silos. They hit the same bank account.

This is also where founders need to be careful with cross-border reading. Plenty of online finance content is useful for understanding cash discipline generally. For example, guidance on Intelligent Contacts' HSA rules is obviously US-specific, but it's a reminder that compliance rules always hinge on timing and allowed use of funds. Australian tax works the same way. Money with a restricted purpose needs to be handled deliberately, not casually.

Why Payday Super changes the game

A lot of generic tax content still talks about super as if it's a periodic admin task. That view is out of date. According to the ATO-focused guidance referenced in this Payday Super discussion for Tax Time 2026, Payday Super is mandated from 1 July 2025, requiring employers to pay super guarantee at the same time as wages.

That change matters because it compresses your cash cycle. Under old habits, some businesses mentally parked super in the “later” category. With Payday Super, that buffer disappears. If wages go out and super doesn't, you've created a compliance problem immediately.

Stop treating super like a quarterly clean-up item. Build it into every payroll run, every roster decision and every hiring conversation.

For time-poor founders, the recommendation is simple. Automate payroll and super workflows together, then reflect that combined outflow in your rolling cash forecast. If your gross margin can't support wage costs plus on-time super, the issue isn't payroll software. It's pricing, productivity or staffing mix.

That's why I'm opinionated on this. Tax planning is not annual. It's weekly cash stewardship. If your systems don't reflect that, the rules will catch up with you before growth does.

Smart Recordkeeping and Essential Deductions

Messy records cost you twice. First, they waste time. Second, they make you either miss deductions or claim things you can't properly defend.

Neither outcome is acceptable. A serious business needs a digital paper trail that can survive staff changes, tax review and growth.

Build a digital paper trail

If you're still relying on spreadsheets, inbox searches and a shoebox of receipts, fix that first. Use cloud accounting software like Xero, MYOB or QuickBooks. Connect bank feeds. Publish a clear expense policy. Make receipt capture part of the transaction, not an archaeological dig at BAS time.

Your recordkeeping system should answer four questions fast:

What was purchased

Why it was for the business

When it was incurred

How it was paid

That means keeping source documents, tax invoices, payroll records, contractor invoices, loan documents and support for asset purchases in one organised system. It also means separating personal and business spending. A dedicated business card and business account are basic discipline, not advanced finance.

A practical weekly routine looks like this:

Code transactions every week: Don't let uncategorised items pile up.

Attach documents immediately: Use your accounting app's file attachment feature.

Reconcile payroll without delay: Match wage, PAYG and super entries while details are fresh.

Review unusual spend monthly: Travel, motor vehicle, home office and mixed-use costs need extra care.

If you want a focused example of how narrowly deduction rules can apply, Nexist's article on travel to work tax deduction rules is worth reading. It's a good reminder that common assumptions often don't match what's claimable.

Claim what is real, not what is convenient

Most owners know the obvious deduction categories. The trouble starts with mixed-use expenses, weak substantiation and broad assumptions. Vehicle costs, home office expenses, subscriptions, software, phones, equipment and contractor costs can all be valid. But only if the business use is real and the records support it.

Use this filter before claiming anything:

Question | Why it matters |

|---|---|

Is there a clear business purpose? | Personal spending disguised as business spend creates risk |

Do you have proper evidence? | A claim without records is weak even if it was legitimate |

Is the treatment consistent? | Random coding decisions create avoidable errors |

This is also where founders can overlook more specialised opportunities. If your business develops products, processes or technical improvements, don't rely on guesswork. Read comprehensive R&D tax credit information to understand the documentation mindset required for those claims. Even when the underlying rules differ across jurisdictions, the lesson is useful: detailed project tracking beats vague year-end reconstruction every time.

Clean books don't just protect deductions. They help you spot margin leaks, duplicate software, stale stock and spending drift.

One more blunt point. Don't chase deductions that damage decision-making. Buying something useless just to reduce tax is still bad cash management. Keep the asset if it helps operations. Keep the cash if it doesn't.

Your 2026 Small Business Tax Calendar and Checklist

Deadlines don't become less painful because they're predictable. They become less painful when your business is organised around them.

Most tax stress comes from poor cadence, not lack of information. When you know which periods trigger BAS work, payroll reporting, super obligations and annual tax tasks, you can build staffing, bookkeeping and cash provisioning around the calendar instead of reacting late.

A practical annual rhythm

Use this as a working checklist, then confirm exact lodgement dates with your accountant or registered tax agent. If you need a broader governance view around reporting and obligations, Nexist's guide to tax and compliance for growing businesses is a useful companion.

Australian SME Tax and Compliance Checklist 2026

Period | Obligation (GST/BAS, PAYG, Super) | Deadline |

|---|---|---|

Weekly | Reconcile bank feed, code transactions, review tax holding account | Internal business deadline |

Each payroll run | Process wages, PAYG withholding and super together | Same payroll cycle |

Monthly | Review BAS position, payroll reports, debtor collections and cash forecast | Internal business deadline |

Each quarter | Prepare and lodge BAS, review PAYG obligations, confirm super processing | ATO and fund deadlines vary |

Year end | Finalise books, review deductions, prepare company tax records | After financial year close |

Tax return period | Lodge annual income tax return through your adviser | Based on your lodgement program |

The point of this table isn't legal precision down to every date. It's operating discipline. A founder should know which obligations are recurring, which are payroll-linked, and which need cash reserved before the due date gets close.

Owner checklist you should review every month

Use a short review, not a heroic catch-up session.

Tax cash ringfenced: Is money for BAS, PAYG and income tax sitting outside your trading account?

Payroll synced: Are wages, withholding and super processed as one workflow?

Books current: Are bank feeds reconciled and uncoded items cleared?

Red flags visible: Have you checked unusual deductions, owner spending and contractor payments?

Forecast updated: Does the next cash flow view include tax outflows, not just supplier bills?

That monthly discipline is what keeps annual obligations boring. Boring is good.

Common Tax Pitfalls and How to Avoid Them

Small errors aren't harmless when they repeat across thousands of businesses. The ATO's own numbers make that clear. For 2022–23, the ATO estimated the net small business income tax gap at $27.2 billion, which represented 17.4% of total theoretical tax liability. It also noted that omission of income accounts for about 49% of the overall gap, while over-claimed business deductions represent nearly 48% of the remainder, according to the ATO's latest small business income tax gap estimate and trends.

That should change how you think about “minor” mistakes. The ATO isn't looking at a few isolated slip-ups. It's looking at repeated patterns in underreported income and unsupported claims.

Small mistakes aren't small

One common belief gets owners into trouble. They assume that because they're small, the ATO won't care about edge cases, rough estimates or personal spending mixed through the business. That's the wrong mindset.

The bigger risk isn't one dramatic act. It's routine sloppiness. Rounded numbers. Missing sales. Expenses coded to the wrong category. Director spending pushed through the company card. Those patterns create the exact kind of distortion the tax gap reflects.

Another major blind spot is business status itself. Some ventures are run more like hobbies or side projects than commercial enterprises. Yet owners still try to deduct losses against other income as if the activity is clearly a business. That's dangerous. ATO focus areas for small businesses in 2025 include non-commercial loss misreporting and incorrect claims around small business measures, as highlighted in Wolters Kluwer's summary of the ATO's 2025 focus areas.

The mistakes that trigger pain

The highest-friction errors are usually these:

Mixing private and business spending: This makes deductions weaker, bookkeeping slower and reviews harder to defend.

Treating side ventures as obvious businesses: If profit intent, structure and business-like behaviour are weak, loss claims become risky.

Using GST cash for operations: That creates a known liability without reserved funds.

Ignoring payroll-linked obligations: Wage compliance isn't complete if related obligations are late or fragmented.

Ask yourself hard questions:

Pitfall | Better approach |

|---|---|

Personal costs through the business | Use separate accounts and classify director spending clearly |

Vague deduction claims | Keep invoices, business purpose notes and consistent coding |

Side-hustle loss claims | Get advice on whether the activity is genuinely commercial |

Reactive compliance | Review books and obligations before lodgement pressure builds |

If you can't explain why an expense exists, how it earns income, and where the evidence sits, don't claim it until you can.

My blunt advice is this. Don't optimise aggressively on weak records. First get clean books, clear business purpose and disciplined cash handling. Then optimise. The order matters.

Beyond Tax Returns The Role of a Virtual CFO

A tax agent helps you lodge correctly. That matters. But it doesn't fix the operating habits that caused the tax stress in the first place.

If you're constantly short before BAS, unsure whether margins are real, or making decisions off yesterday's numbers, you don't only have a tax issue. You have a finance engine issue.

A tax agent files history, a virtual CFO manages the future

That distinction matters more than most founders realise. A tax return tells the ATO what already happened. A virtual CFO helps you shape what happens next.

That means asking different questions:

Can the business afford this hire once wages, super and tax timing are included?

Is margin being lost through pricing, discounts, stock holdings or poor purchasing discipline?

Which customers pay too slowly and create hidden tax pressure?

What does the next quarter look like if sales soften or inventory expands?

A virtual CFO also forces a stronger operating cadence. Weekly cash reports. Monthly forecast updates. KPI visibility. Cleaner approval processes. Decision-making based on current numbers rather than gut feel.

One option for founders who want that structure is a service like virtual chief financial officer support, where forecasting, cash flow planning, reporting and finance process design sit alongside compliance. That's different from only meeting someone after the year is over.

What changes when finance becomes operational

When a founder has proper finance support, tax pressure usually drops because the root causes get addressed. Stock purchasing gets tighter. Debtors are chased earlier. Payroll is mapped properly. Owner drawings become planned instead of random. Compliance stops living in someone's memory and starts living in process.

This short video gives a useful sense of that shift in practice.

You also reclaim attention. That might be the biggest gain. Founders waste enormous energy carrying financial uncertainty in the background. When reporting is clear and obligations are visible, you stop second-guessing every spend and start leading the business properly.

The right finance setup should help you do all of this:

See cash pressure early: Not after the account balance drops.

Link tax to operations: So payroll, pricing and purchasing decisions reflect real obligations.

Create repeatable systems: So the business doesn't depend on heroic catch-ups.

Make confident decisions: Because the numbers are timely enough to trust.

If your current setup only produces answers after the fact, it's too late for a growth-stage business. Compliance is necessary. Control is better.

If tax keeps surprising you, the issue usually isn't effort. It's structure. Nexist helps Australian founders build that structure through cash flow forecasting, reporting, tax-aware finance processes and hands-on virtual CFO support, so the business stops reacting to numbers and starts using them.

small business taxation, australian tax guide, sme tax obligations, cash flow management, virtual cfo

" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="dSFdkJotL" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="wscNJE44G" transform="translate(0 0.129)" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="sTpjGo1tb" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="s7ffpmKOD" transform="translate(0 0.129)" width="24px"/><g d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.000006px" id="D0ecaHEcW" transform="translate(0 0)" width="24px"><path d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z" fill="rgb(55, 184, 218)" height="24.000006px" id="IPLFE6zXx" width="24px"/><path d="M 4.02 0 L 0 0 L 0 12.092 L 4.02 12.092 Z" fill="rgb(255, 255, 255)" height="12.09201px" id="FWhtzAyuY" transform="translate(2.863 8.375)" width="4.02px"/><path d="M 2.274 0 C 0.899 0 0 0.904 0 2.089 C 0 3.25 0.871 4.179 2.221 4.179 L 2.247 4.179 C 3.648 4.179 4.521 3.25 4.521 2.089 C 4.495 0.904 3.649 0 2.274 0 Z" fill="rgb(255, 255, 255)" height="4.17876px" id="VmOsKv4kO" transform="translate(2.625 2.545)" width="4.52095px"/><path d="M 7.641 0 C 5.509 0 4.554 1.173 4.019 1.996 L 4.019 0.284 L 0 0.284 C 0.053 1.419 0 12.376 0 12.376 L 4.019 12.376 L 4.019 5.623 C 4.019 5.262 4.045 4.9 4.151 4.642 C 4.442 3.92 5.103 3.172 6.214 3.172 C 7.667 3.172 8.25 4.282 8.25 5.907 L 8.25 12.376 L 12.269 12.376 L 12.269 5.442 C 12.269 1.728 10.286 0 7.641 0 Z" fill="rgb(255, 255, 255)" height="12.37626px" id="n1XUbhaq0" transform="translate(9.105 8.09)" width="12.268830000000001px"/></g></g></g></g></svg>)