Overcome Small Business Cash Flow Problems: 2026 Playbook

Facing small business cash flow problems? Our practical playbook for Australian founders provides diagnosis, short-term fixes, & long-term systems to regain

Ansh Malhotra

You're looking at the bank balance, the P&L says you made money, and yet payroll, rent, BAS, supplier payments, and your own drawings are all competing for the same dollars. That's the point where a lot of founders start wondering whether the business is working.

It usually is. The problem is that revenue timing, stock decisions, payment terms, and operational friction can drain cash long before the accounts catch up. In Australia, nearly 80% of small and medium businesses said their cash flow had been affected in the previous year, with the biggest drivers being declining revenue (35%), low cash reserves (30%), and seasonal fluctuations (27%), according to UNSW's January 2025 report on a Commonwealth Bank-commissioned survey.

Most articles stop at “chase invoices faster”. That matters, but it's only one leak. Cash also disappears into over-ordering, poor handoffs between sales and finance, unnecessary subscriptions, labour inefficiency, and payment processor delays that make sales look healthy while cash lands late. If you want to fix small business cash flow problems, you need to trace where the money stalls, not just where the profit sits.

Table of Contents

The Profit Paradox Why Your Business Is Successful but Broke

A founder finishes the month with strong sales, sees a positive net profit, then realises there still isn't enough cash to cover everything due this week. That isn't unusual. It's one of the most common small business cash flow problems.

Profit is an accounting result. Cash is a timing reality. You can record a sale today, but if the customer pays in a month, the bank account doesn't improve today. You can also show profit while cash falls because stock was purchased upfront, tax is due, loan repayments hit, or wages landed before customer receipts.

That's why a profitable business can still feel starved. A wholesale business may have a healthy gross margin but too much cash tied up in stock. A service business may have a full pipeline but weak billing discipline, so work is done long before invoices go out. An ecommerce operator may be selling well through a platform, but settlement timing, returns, and ad spend drag the bank balance down.

If you're trying to improve margin at the same time, this guide on B2B profit margins for leaders is useful because it separates pricing and margin decisions from pure cash timing. The two are related, but they're not the same problem.

Practical rule: Don't ask only, “Did we make money?” Ask, “When does the cash actually arrive, and what has to be paid before then?”

Founders often treat cash stress as a sign they're failing. Usually, it's a sign the business has outgrown informal financial management. A spreadsheet built for startup stage won't protect you once payroll, GST, inventory, and supplier commitments become lumpy and frequent. That's where disciplined planning matters, especially if you want decisions tied back to a proper strategic and financial planning framework.

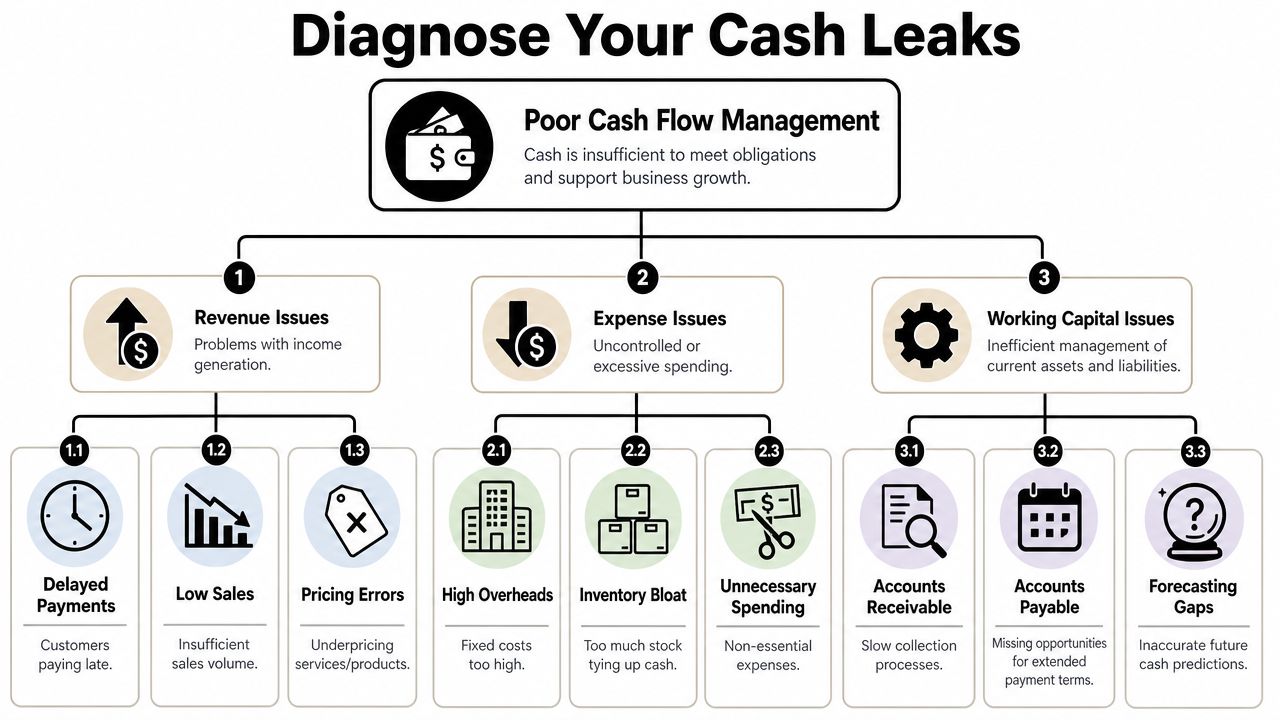

Diagnose Your Cash Leaks Before You Fix Them

Before you cut costs or chase debtors, work out which leak is draining cash. Otherwise, you'll spend energy on the wrong fix.

A useful reality check is this: 39% of small businesses say they don't have enough cash on hand to cover one month of operating expenses in an emergency, and cash flow is the top concern for 31% of owners, as outlined in this small business cash flow and financing benchmark. Thin buffers mean even minor timing problems can turn into a crisis.

Read cash movement, not just the P and L

Start with your Statement of Cash Flows if you have one. If you don't, rebuild the same logic from your bank transactions, receivables, payables, and payroll file.

Look at three buckets:

Operating activity. This tells you whether day-to-day trading is generating cash.

Investing activity. Equipment, fitout, software implementation, or large stock purchases often sit here and can create pressure quickly.

Financing activity. Loan repayments, director drawings, and debt inflows can hide an underlying trading problem for months.

If operating cash is weak while sales look fine, the leak is usually in working capital. If cash drops after major purchases, the issue may be timing and commitment discipline rather than poor sales.

Use the cash conversion cycle as a leak detector

The cash conversion cycle shows how long cash is trapped between paying out and getting paid back. In plain English, it tracks three things:

Area | What to examine | What a bad signal looks like |

|---|---|---|

Receivables | How long customers take to pay | Invoices aging without follow-up |

Inventory | How long stock sits before sale | Slow movers building up quietly |

Payables | How fast you pay suppliers | Paying early while customers pay late |

The formula matters less than the habit. Ask simple questions. Are invoices sent on completion, or days later? Are you ordering based on forecast demand, or anxiety about stockouts? Are supplier terms aligned with customer payment behaviour, or are you funding the whole cycle yourself?

If you want a deeper explanation of how this works in practice, Nexist has a clear piece on the cash conversion cycle for growing businesses.

If cash is always tight, assume there's a timing problem first. Then prove or disprove it with debtor days, stock age, and supplier terms.

Look for operational leaks outside the ledger

Some leaks don't show up clearly in standard reports.

A few I see often:

Inventory bloat. Buyers keep ordering because margin looks good, but no one asks how long that stock will sit.

Returns friction. Ecommerce brands can lose cash through replacement shipping, reverse logistics, and delayed resale. That's why practical guidance on strategies to reduce ecommerce returns can matter as much as a debtor report.

Payment processor delays. Card settlements, reserve holds, chargebacks, and marketplace release schedules can create a gap between “sale made” and “cash available”.

Process lag. Jobs are completed, but someone forgets to mark them ready for invoicing. Or purchase approvals sit in email while urgent spend keeps happening.

Payroll mismatch. Labour gets paid weekly, but revenue comes in later and less predictably.

A fast diagnosis workshop with the owner, ops lead, and finance contact usually reveals more than a stack of reports. Follow one dollar from quote to bank. Then follow one dollar from purchase request to supplier payment. The gaps become obvious quickly.

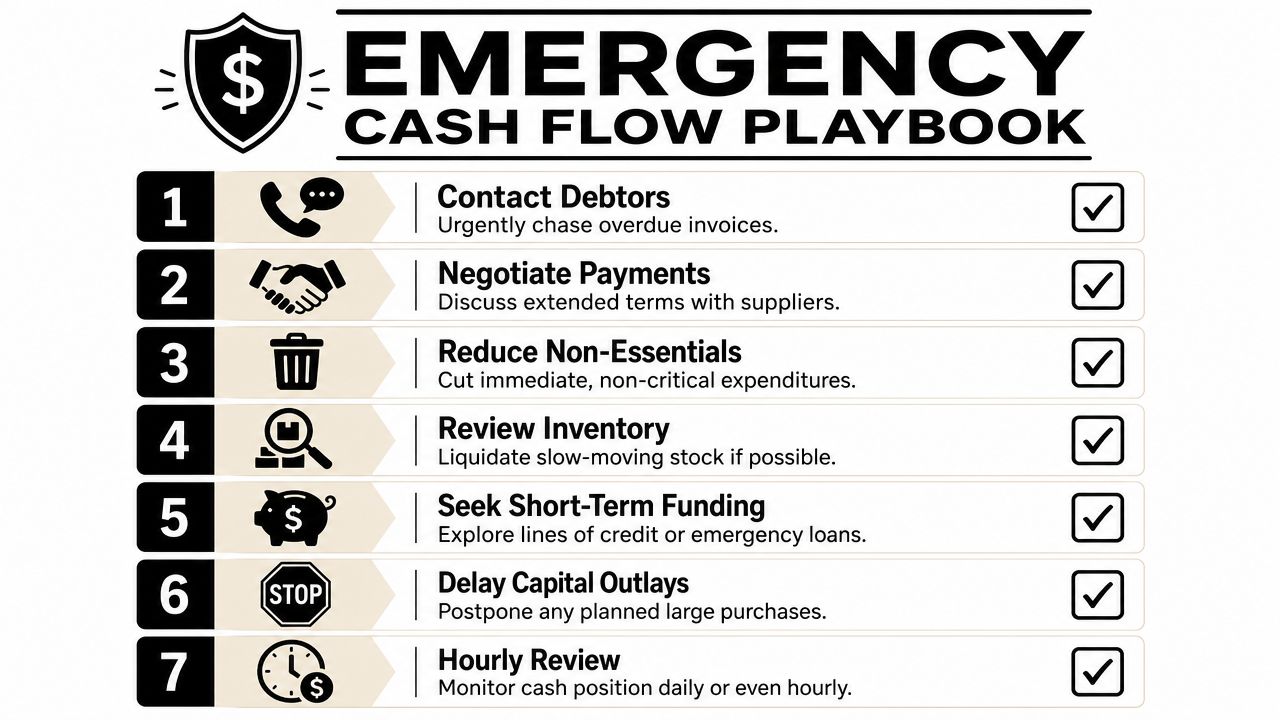

Your Emergency Playbook Immediate Stabilisation Tactics

When the bank balance is under pressure, you don't need theory first. You need room to breathe.

Start with this checklist.

Cash-flow disruptions affect 88% of small businesses, and one of the most direct fixes is reducing the cash conversion cycle by invoicing immediately, enforcing payment terms, and negotiating better supplier terms, according to the U.S. Chamber's cash flow guidance for small businesses.

First moves in the next 48 hours

Pull these levers in order.

Freeze non-essential spending

Stop software purchases, discretionary marketing tests, low-priority contractors, travel, equipment upgrades, and any stock reorder that isn't tied to near-term demand. This isn't forever. It's triage.Send every billable invoice immediately

Not tomorrow. Not after the month-end tidy-up. If work is complete or goods have shipped, invoice now.Call overdue debtors

Email is too passive when cash is tight. Pick up the phone. Confirm they received the invoice, confirm there's no dispute, and ask for a payment date while you're on the call.Review stock for liquidation candidates

Old lines, excess variants, and low-turn items can often be converted into cash faster through bundles, discounts, or wholesale clearance than by waiting for full-price perfection.Stretch payables carefully

Don't ignore suppliers. Talk to them before due dates. Reliable communication preserves goodwill better than silence.

Here's the mindset. Protect wages, tax obligations, and suppliers that keep the core operation running. Everything else gets challenged.

A useful explainer on the discipline behind these decisions is below.

How to talk to debtors and suppliers without making things worse

Founders often avoid these calls because they don't want to sound desperate. That hesitation is expensive.

Use direct language with customers:

“I'm calling about invoice 1048. Can you confirm it's approved for payment, and what date we should expect funds in the account?”

If they say there's an issue, surface it immediately. Delivery dispute, missing purchase order, wrong contact, incomplete paperwork. Most overdue invoices are delayed by process friction, not bad intent.

With suppliers, be honest and specific:

“We want to keep trading cleanly. Cash is tight this fortnight. Can we move this payment to next week and keep current terms for upcoming orders?”

Specific beats vague. A supplier is far more likely to cooperate if you offer a date and show control.

Use short-term funding carefully

There are times when bridging finance is sensible. Invoice finance, an overdraft, or a line of credit can buy time if receipts are due and the gap is temporary.

Use these products for timing mismatches, not for structural losses. If you're borrowing every month because margin is too thin, labour is inefficient, or stock keeps piling up, debt won't fix the root problem. It will just make it more expensive.

A short decision filter helps:

Option | Useful when | Dangerous when |

|---|---|---|

Invoice finance | Large receivables are real and collectible | Customers are disputed or chronically late |

Line of credit | You need short breathing space between inflows and outflows | You rely on it as normal operating cash |

Supplier extension | Relationship is strong and issue is temporary | You repeatedly break agreed dates |

If you need support getting control fast, one option in the market is Nexist, which works across forecasting, receivables, payables, stock, and operating processes to identify where cash is leaking and what needs to change first. The key point is not the provider. It's that emergency action works best when someone owns the list, the deadlines, and the daily cash view.

Building a Resilient Cash Flow System for the Long Term

Firefighting helps this week. Systems protect the next quarter.

For Australian SMEs, the most reliable control is a rolling 13-week cash forecast updated weekly because it turns AR, AP, payroll, and BAS/GST obligations into a practical liquidity plan that a monthly P&L won't catch, as discussed in this 13-week cash forecasting reference.

Build the 13-week forecast properly

A real 13-week forecast isn't a hopeful sales spreadsheet. It's a timing tool.

Build it this way:

Start with opening bank balance. Use actual cash, not projected cash.

Layer expected receipts by date. Tie them to invoices, recurring revenue schedules, and realistic customer behaviour.

Add mandatory outflows. Wages, super, BAS/GST, tax, rent, debt service, software, insurance, and supplier payments.

Separate committed from discretionary spend. This shows what can be paused if needed.

Run three views. Best case, base case, and worst case.

Weekly updates are essential. Once the forecast slips out of date, people stop trusting it and revert to checking the bank app. That's not financial management. That's anxiety management.

Systemise AR and AP instead of relying on memory

Most recurring cash pain comes from informal habits.

A stable AR process includes:

Immediate invoicing after dispatch, milestone completion, or signed timesheet.

Clear payment terms written into proposals, onboarding, and invoices.

Automated reminders before due date and after due date.

Escalation rules so old debts trigger a call, not another polite email.

A stable AP process includes:

Approval controls before spend happens.

Scheduled payment runs rather than ad hoc payments whenever an invoice lands.

Supplier term negotiation based on volume, history, and reliability.

Visibility of upcoming obligations at least several weeks out.

A lot of founders think automation is the answer by itself. It isn't. Software only speeds up the process you already have. If the workflow is messy, automation just makes the mess happen faster.

Track the indicators that warn you early

You don't need a huge dashboard. You need a short list that people review.

Indicator | What it tells you | Why it matters |

|---|---|---|

Debtor days | How long customers take to pay | Rising days usually show collection weakness or poor customer quality |

Inventory turns | How quickly stock converts to sales | Slow turns trap cash and hide purchasing mistakes |

Creditor days | How long you take to pay suppliers | Helps manage timing and preserve working capital |

Forecast variance | Difference between forecast and actual | Shows whether your planning is reliable enough to act on |

Gross margin by line | Which products or services create room | Prevents cash being tied up in low-value activity |

For product businesses, inventory deserves special discipline. Practical advice on streamlining inventory for D2C brands is useful because warehouse and stock decisions are usually financial decisions in disguise.

A resilient business doesn't wait for month-end to discover a cash problem. It sees the pressure building weeks earlier and adjusts before the bank balance forces the decision.

Industry-Specific Strategies for Cash Flow Optimisation

Cash leaks look different depending on how the business earns money. An ecommerce or wholesale operator usually traps cash in stock. A service or trade business usually loses cash through billing lag, labour timing, and uneven collections.

A major issue for inventory-heavy businesses is seasonality and inventory lock-up. The key question is when buying early for stock availability destroys more cash than it protects in margin, as explored in this research on seasonal cash flow challenges.

Inventory-heavy businesses

Retail, ecommerce, wholesale, and manufacturing businesses often mistake stock for security. It can be the opposite. Stock sitting in a warehouse is cash you can't use for wages, ads, supplier payments, or buffer.

Three moves matter most.

First, do an ABC analysis. Separate fast sellers, steady contributors, and slow movers. Your A items deserve tight replenishment attention. Your C items need hard questions. Why are they still here, what's the exit plan, and who keeps reordering them?

Second, align purchase decisions with cash reality, not supplier pressure. Bulk-buy discounts look attractive until they create a hole in the bank account. Margin saved on paper can be wiped out by the cost of carrying dead stock and losing flexibility.

Third, negotiate smarter terms. Deposits, staggered deliveries, smaller minimums, consignment, or delayed final payments can all reduce pressure. Not every supplier will agree, but many will if you ask clearly and give them confidence in the relationship.

A practical review for inventory-led businesses should include:

Ageing by SKU so old stock is visible.

Stock cover by weeks or months to expose overbuying.

Promotional exit plans for lines that aren't moving.

Reorder rules based on sales velocity, not guesswork.

Service and trade businesses

Service firms and trades often have the opposite problem. There's little inventory, but cash still runs tight because labour gets paid before the job is fully billed and collected.

The usual fixes are commercial, not accounting-based.

Take deposits on larger jobs. Use progress claims for longer work. Bill immediately at milestone completion. Don't leave invoicing until the end of the month because “the office is busy”. That habit turns completed work into unpaid working capital.

Payment platforms create another hidden drag. Card terminals, gateways, booking systems, and marketplaces don't always settle funds as quickly as founders expect. Strong sales can still leave a cash hole if part of the takings are delayed, reserved, or offset by refunds and chargebacks. That's why service businesses should map cash arrival by channel, not just total revenue.

A quick comparison helps:

Business type | Main leak | Better control |

|---|---|---|

Ecommerce or retail | Overstock and slow movers | SKU-level review, staged purchasing, stricter reorder logic |

Wholesale or manufacturing | Large supplier commitments before collection | Deposits, production scheduling, supplier term negotiation |

Agency or consulting | Work done before invoice raised | Milestone billing, immediate invoicing, tighter collections |

Trades or field services | Payroll and materials paid before final receipt | Deposits, progress billing, daily job-cost visibility |

The right strategy depends on where cash gets trapped in your operating model. If you misdiagnose that, even disciplined founders keep feeling broke.

When to Stop DIY and Engage a Virtual CFO

There's a point where founder-led cash management becomes too expensive in time, stress, and missed decisions.

If you're spending hours each week reconciling payments, chasing debtors, guessing stock buys, and trying to predict whether BAS will hurt, you're already paying for the problem. You're just paying in a less visible way.

One trigger is constant firefighting. Another is inaccurate forecasting. Another is when sales are strong but cash still feels unpredictable because no one has visibility into payment timing, platform holds, and settlement delays. That kind of mismatch is exactly the issue highlighted in this cash flow perspective on the small business sector from JPMorgan Chase Institute.

A good bookkeeper records what happened. A virtual CFO helps decide what should happen next. That includes scenario planning, working capital management, pricing discipline, inventory decisions, payment timing, and turning reports into actions.

You should seriously consider outside support when:

You can't trust your forecast enough to hire, buy, or invest.

Cash issues keep returning even after a good sales month.

Operations and finance are disconnected so jobs, stock, and invoices don't line up.

You've hit a growth ceiling because every expansion decision feels risky.

You need decision support, not just reconciliations and compliance.

If you're unsure what that role includes, this explanation of what a CFO does for a growing business is a useful starting point.

The right time to bring in a virtual CFO isn't when the account is nearly empty. It's when the business has enough complexity that better visibility will change decisions before they become expensive.

If your business is profitable on paper but cash still feels tight, Nexist can help you find the leaks, rebuild the forecast, and put structure around receivables, inventory, and operating decisions so more cash stays in the bank.

small business cash flow, cash flow management, virtual cfo australia, business finance guide, working capital

" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="dSFdkJotL" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="wscNJE44G" transform="translate(0 0.129)" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="sTpjGo1tb" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="s7ffpmKOD" transform="translate(0 0.129)" width="24px"/><g d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.000006px" id="D0ecaHEcW" transform="translate(0 0)" width="24px"><path d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z" fill="rgb(55, 184, 218)" height="24.000006px" id="IPLFE6zXx" width="24px"/><path d="M 4.02 0 L 0 0 L 0 12.092 L 4.02 12.092 Z" fill="rgb(255, 255, 255)" height="12.09201px" id="FWhtzAyuY" transform="translate(2.863 8.375)" width="4.02px"/><path d="M 2.274 0 C 0.899 0 0 0.904 0 2.089 C 0 3.25 0.871 4.179 2.221 4.179 L 2.247 4.179 C 3.648 4.179 4.521 3.25 4.521 2.089 C 4.495 0.904 3.649 0 2.274 0 Z" fill="rgb(255, 255, 255)" height="4.17876px" id="VmOsKv4kO" transform="translate(2.625 2.545)" width="4.52095px"/><path d="M 7.641 0 C 5.509 0 4.554 1.173 4.019 1.996 L 4.019 0.284 L 0 0.284 C 0.053 1.419 0 12.376 0 12.376 L 4.019 12.376 L 4.019 5.623 C 4.019 5.262 4.045 4.9 4.151 4.642 C 4.442 3.92 5.103 3.172 6.214 3.172 C 7.667 3.172 8.25 4.282 8.25 5.907 L 8.25 12.376 L 12.269 12.376 L 12.269 5.442 C 12.269 1.728 10.286 0 7.641 0 Z" fill="rgb(255, 255, 255)" height="12.37626px" id="n1XUbhaq0" transform="translate(9.105 8.09)" width="12.268830000000001px"/></g></g></g></g></svg>)