Primary Producer Tax Benefits: 2026 Australia Guide

Discover primary producer tax benefits in Australia. Our 2026 guide explains FMDs, depreciation, and income averaging to boost your farm's cash flow.

Ansh Malhotra

A good season creates a strange problem. Grain comes off strong, livestock prices hold, receivables finally clear, and the bank balance looks better than it has in a while. Then your accountant sends the projected tax position, and suddenly the “good year” feels less comfortable.

That's the moment many farm owners make reactive decisions. They buy equipment they don't need, rush deductions without checking eligibility, or leave it too late to use the tax rules that help cash flow. The better approach is to treat tax as part of working capital management. For a primary producer, that means using the rules to keep more cash available for the next season, the next infrastructure upgrade, or the next shock.

If you run livestock or mixed farming, that same thinking applies all the way down to feed, waste, and input efficiency. Practical operating choices often sit right beside tax choices, which is why resources on smart decisions for poultry farms can be useful when you're looking at the full profit picture, not just the tax return.

Table of Contents

Beyond the Tax Bill A Strategic Approach to Farm Finances

A farm owner in a strong year usually sees the same pattern. Cash improves, suppliers get paid down, maybe there's room to replace fencing or sort out water infrastructure, and confidence returns. Then tax planning gets left until year end, when the best options are narrower and the pressure is higher.

The farm businesses that handle this well don't treat primary producer tax benefits as a once-a-year compliance exercise. They use them the way a CFO would use any financial lever. To hold cash in better seasons. To avoid being forced into bad borrowing in poor ones. To line up capital works with the timing of taxable income. To make sure a tax bill doesn't consume funds that should have been kept for resilience.

That's the key shift. Tax planning on a farm isn't only about reducing taxable income. It's about controlling when cash leaves the business and when it stays available for operations.

A tax deduction matters. Cash timing matters more.

That's why planning needs to sit beside forecasting, debt management, and capex decisions. If you're making infrastructure choices without a cash-flow model, you're only doing half the job. A practical framework for that sits in strategic and financial planning for growing businesses, and the same discipline applies on farm. Start with expected income volatility, layer in capital needs, then choose the tax tools that support the plan.

Do You Qualify for Primary Producer Tax Benefits

A lot of owners jump straight to deductions. That's backwards. The first gate is whether the ATO would treat your activity as a primary production business at all.

The first question is business status

The ATO says qualification depends on carrying on a primary production business in activities such as cultivation, animal maintenance, fishing, pearling, or tree farming, not merely owning land or running a hobby-scale activity. That classification is also relevant for beneficiaries of primary production trusts, as set out in the ATO guidance on primary production activities.

That sounds straightforward, but in practice many claims unravel. Owning rural land doesn't make you a primary producer. Running a few animals without commercial intent doesn't either. The tax system cares about the business activity, not the vibe of the property.

Use this as a practical test:

Commercial activity: Are you operating with a clear profit purpose and regular business activity, or is the property mainly lifestyle-driven?

Actual production: Are you cultivating, breeding, maintaining livestock, fishing, harvesting, or carrying on another recognised production activity?

Business systems: Do you keep business records, run bank accounts properly, issue invoices where relevant, and make decisions like an operator rather than a hobbyist?

Structure impact: Are you operating as an individual, partnership, trust, or company, and have you checked how the benefit flows through that structure?

Where owners get caught out

The grey zone is usually mixed-use operations. Lifestyle farms with some agistment. Rural properties with occasional livestock sales. Side businesses where the owner hopes the tax status will “sort itself out”. It won't.

If you're in that zone, the wrong move is to assume you qualify because someone nearby does. The right move is to document the business purpose, activity pattern, and ownership structure before making claims.

A trust adds another layer. The concession may not land where the owner expects, especially when trust distributions and beneficiary treatment are involved. That doesn't mean a trust is a problem. It means the classification work needs to happen early.

Practical rule: Before you plan deductions, confirm the entity and activity actually qualify. Good tax strategy built on the wrong classification is still bad tax strategy.

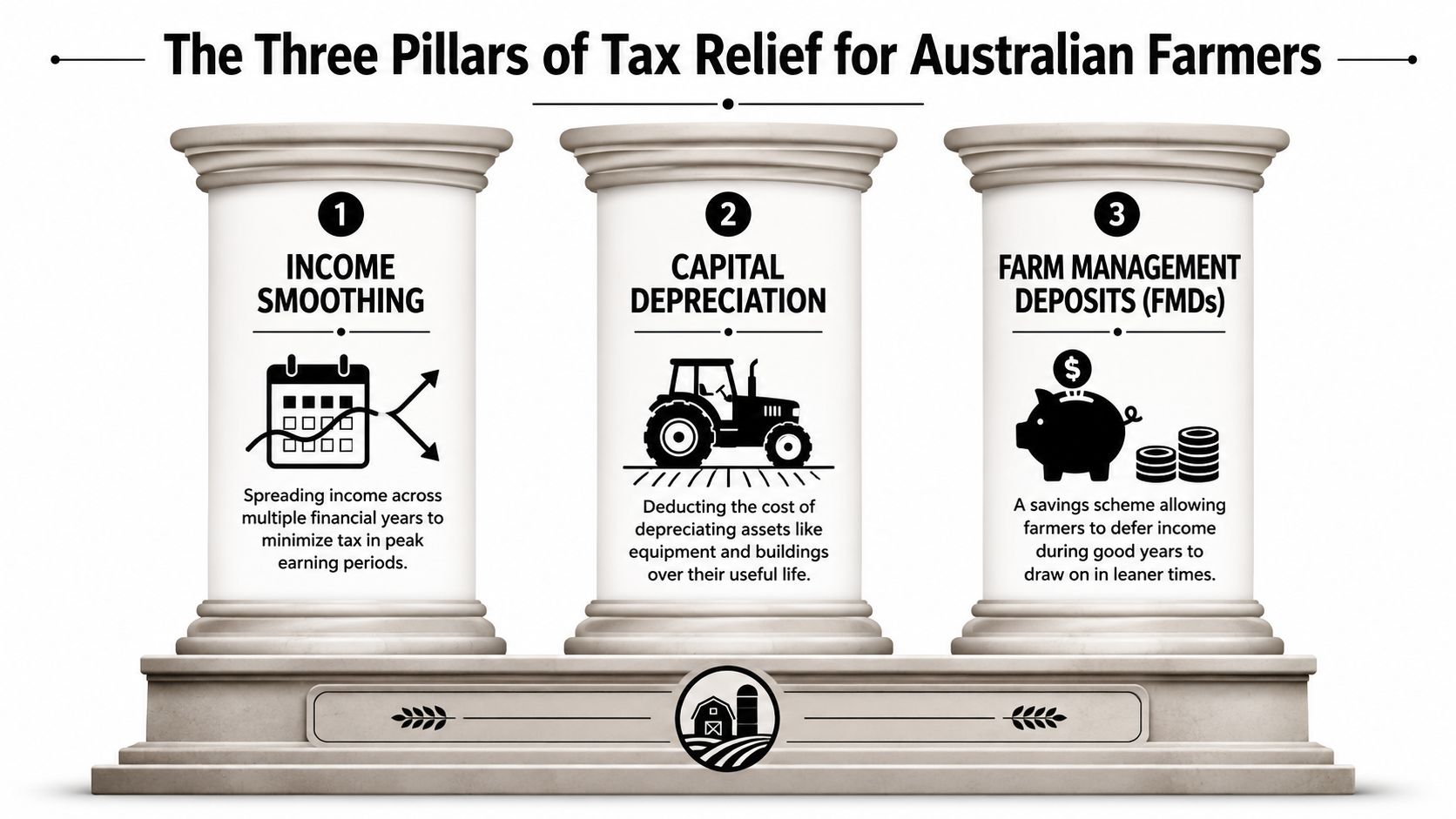

The Three Pillars of Tax Relief for Australian Farmers

Most farm tax planning gets explained as a list. Lists are easy to read and hard to use. In practice, the useful way to think about primary producer tax benefits is through three pillars: smoothing income, accelerating deductions, and using special rules for unusual farm events.

Pillar one Income smoothing

Farming income rarely arrives in a neat, predictable pattern. One year can carry strong yields or prices. The next can be hit by weather, input cost spikes, or forced destocking. The tax system recognises that volatility.

Under the Farm Management Deposits scheme, eligible primary producers can hold up to A$800,000 per person, and deposits are tax-deductible in the year they're made and become assessable income when withdrawn, according to Bentleys' overview of accounting for primary producers.

That gives you a direct income-smoothing tool. In a high-income year, you may be able to move part of that income into an FMD. In a lean year, you can bring it back into income when the business needs liquidity more than it needs a tax deduction.

Pillar two Accelerated capital deductions

This pillar is about infrastructure and productive assets. Not every tax rule helps cash quickly, but accelerated deduction rules can.

For farm businesses, tax planning begins to resemble finance strategy. If you're already spending on eligible infrastructure, bringing the deduction forward can improve after-tax cash flow in the same period you've written the cheque.

Pillar three Special provisions

Some rules exist because farming produces unusual events that ordinary businesses don't face in the same way. Livestock can be lost or sold under pressure. Seasons can force decisions no operator would choose in normal conditions.

The ATO notes that profits from the forced disposal or death of livestock can be spread over 5 years, and it also recognises tools such as income averaging and the FMD regime as part of the broader framework for primary producers in its guidance for primary producers and averaging arrangements.

Here's the strategic point. These pillars do different jobs:

Pillar | Best used for | Cash-flow effect |

|---|---|---|

Income smoothing | Good years followed by uncertain seasons | Preserves flexibility across years |

Accelerated deductions | Planned capex on eligible assets | Brings tax relief forward |

Special provisions | Forced sales, livestock events, uneven farm outcomes | Reduces one-off tax shocks |

A farm owner who sees these rules as one toolkit will usually make better decisions than one who treats them as unrelated claims.

Boosting Cash Flow with Capital Expenditure Write-Offs

Capex on farm is where cash disappears fast. New fencing, fodder storage, tanks, bores, channels, pumps. These aren't cosmetic purchases. They're operating assets, and they often land in the budget at exactly the moment the business is already under pressure.

Where the timing matters most

For Australian primary producers, fencing and fodder storage can be immediately deducted. Water facilities such as dams, tanks, bores, irrigation channels and pumps are immediately deductible if acquired after 12 May 2015, and fodder storage assets are fully deductible for expenses incurred on or after 19 August 2018, with a transitional three-year write-off for some earlier assets installed after 12 May 2015 and before 19 August 2018, as outlined in BMT's summary of primary production tax deductions.

Those dates matter because they change the economics of the purchase year. Instead of waiting through slower depreciation, an eligible producer may bring the deduction into the year the money is spent. That can materially reduce taxable income in the same period the capex hits the bank account.

There's also a broader small business angle. H&R Block notes that small businesses with aggregated turnover under A$10 million can generally access the instant asset write-off for eligible assets under the threshold instead of depreciating them over time, as explained in its guide to tax advice for farmers and primary producers.

How to think about write-offs versus financing pressure

The wrong way to use these concessions is to buy assets just to get a deduction. The deduction is helpful, but it doesn't make a poor purchase good. If the asset doesn't improve production, protect the property, or solve a real operating bottleneck, the tax benefit won't rescue the cash decision.

The right way is to ask three questions before committing:

Need first: Does the asset solve a real operating issue this season or before the next one?

Eligibility second: Is the asset clearly within the concession rules, with the purchase and installation timing documented properly?

Funding third: Will the business still have enough liquidity after the purchase, even before the tax benefit is realised?

For many farm owners, discipline is essential. Immediate deductibility improves the after-tax outcome. It does not eliminate the initial cash outlay. If debt is already tight or a poor season is possible, full expensing can still leave the business short on working capital.

A useful planning discipline is to map capex, debt commitments, and taxable income together before year end. That's the kind of thinking behind tax planning strategies for growing Australian businesses, and it's even more important in farm businesses where seasonality can punish overconfidence.

Buy the asset because the farm needs it. Use the tax rule because the timing helps. Don't reverse that order.

A Worked Example From a Good Year to a Tough One

The cleanest way to understand primary producer tax benefits is to follow the cash, not just the taxable income. Below is a simple example showing how one operator can use an FMD to shift profit from a strong year into a weaker one.

This example is qualitative on tax impact because the actual benefit depends on the owner's broader tax position, structure, and withdrawal timing.

Year one Banking profit instead of donating it to timing

Willow Creek Pastoral has a strong year. Commodity prices are favourable, stock turn is healthy, and the business finishes the season with more profit than expected. The owner's first instinct is to leave everything in the trading account and “deal with tax later”.

That's usually expensive thinking.

Instead, the owner reviews expected cash needs, debt commitments, and likely seasonal volatility. Because the business wants a reserve for a possible weaker year, part of the surplus is placed into an FMD. That lowers current-year taxable income and keeps the funds quarantined for future use.

Year two Using the reserve when the season turns

The next year is tighter. Feed costs rise, production softens, and there's less room to absorb expenses from operating cash alone. Rather than borrowing immediately or selling productive assets under pressure, the owner withdraws the FMD.

That withdrawal becomes assessable income in the lower-income year, but the key point is practical. The cash comes back when the business needs support.

Metric | Year 1 No FMD | Year 1 With FMD | Year 2 With FMD Withdrawal |

|---|---|---|---|

Profit season outcome | Strong | Strong | Tough |

Taxable income treatment | Full income assessed in the year earned | Part of income deferred through FMD | Withdrawn amount brought back into assessable income |

Cash held for future shocks | Lower, because more may leave the business through tax timing | Higher, because funds are reserved inside the FMD structure | Available to support operations in the weaker year |

Reliance on short-term finance | More likely | Less likely | Potentially reduced if the withdrawal covers operating pressure |

Strategic flexibility | Lower | Higher | Higher than if no reserve had been built |

This is why I treat an FMD as a cash-flow tool first and a tax tool second. The tax deduction matters, but the bigger win is preserving optionality. When the season turns, the operator who pre-positioned cash has choices. The one who didn't is often forced into them.

Averaging, livestock rules, and capex planning can complement that approach, but the underlying discipline is the same. Use a strong year to prepare for a weak one before the weak year arrives.

Common Pitfalls and Essential Record-Keeping

The biggest mistake with farm tax concessions is assuming that once you know the rule, the result is automatic. It isn't. Timing, documentation, and sequence decide whether a concession helps cash flow or creates a problem later.

RSM makes an important strategic point: many guides list concessions, but the critical issue is which benefit improves cash flow fastest during a crisis, and how deductions, smoothing tools, livestock cycles, and capex timing are sequenced for working capital, as discussed in its EOFY notes on tax planning tips for primary producers.

The mistakes that undo good planning

A common trap is treating an FMD like a generic savings account. It isn't. If you withdraw at the wrong time, you can pull assessable income back into a year where the business is already carrying stronger results than expected. That can blunt the point of the strategy.

Another trap is claiming capital deductions without clean records on acquisition date, asset type, and business use. If you can't show what was bought, when it was incurred, and how it fits the concession, the claim gets harder to defend.

The third mistake is buying capex for tax reasons while ignoring working capital. A deduction doesn't pay suppliers, wages, freight, or feed bills by itself. If the purchase drains liquidity, the concession may still leave the business cash-poor.

Keep asking one question: does this move improve cash in the bank when the farm needs it, or does it only improve the tax return on paper?

What records actually matter

For most primary producers, the essentials are simple:

Asset evidence: Keep invoices, contracts, finance documents, and installation records for fencing, water assets, fodder storage, and other capex.

Use evidence: Keep enough support to show the asset is tied to the business activity, not private or mixed use without apportionment.

FMD records: Retain deposit confirmations, withdrawal records, and notes showing why the timing fitted your income plan.

Entity records: If you operate through a trust, partnership, or company, keep structure documents and distribution records aligned with the tax treatment.

Video can help if you want a broader refresher on the mindset behind record discipline and tax timing:

Don't fall into a “set and forget” pattern. BAS reporting, year-end tax, financing decisions, and capex timing all interact. The operators who handle this well review their position before year end, after major seasonal changes, and before any large infrastructure spend.

Turn Tax Strategy into Cash with a Virtual CFO

Most tax agents are engaged to get the return right. That matters, but it's not enough for a farm business dealing with volatile income, major capex decisions, and tight working capital windows.

A virtual CFO approach is different. It treats tax concessions as one lever inside a wider operating plan. Forecast the season. Model debt pressure. Time infrastructure spend. Decide whether smoothing income is smarter than claiming more deduction now. Review the likely knock-on effects before cash leaves the account.

That's what turns primary producer tax benefits from a compliance topic into a finance tool. Used properly, they can support resilience, improve timing, and help fund productive investment without creating avoidable stress later.

If you want to understand how that kind of finance leadership works in practice, this overview of a virtual chief financial officer is a useful place to start.

If you want help turning tax concessions into a practical cash-flow plan, Nexist can help you model the timing, pressure-test the options, and build a finance rhythm that supports the farm year-round, not just at lodgement time.

primary producer tax benefits, farm tax deductions, income averaging australia, farm management deposits, agribusiness tax

" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="dSFdkJotL" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="wscNJE44G" transform="translate(0 0.129)" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="sTpjGo1tb" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="s7ffpmKOD" transform="translate(0 0.129)" width="24px"/><g d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.000006px" id="D0ecaHEcW" transform="translate(0 0)" width="24px"><path d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z" fill="rgb(55, 184, 218)" height="24.000006px" id="IPLFE6zXx" width="24px"/><path d="M 4.02 0 L 0 0 L 0 12.092 L 4.02 12.092 Z" fill="rgb(255, 255, 255)" height="12.09201px" id="FWhtzAyuY" transform="translate(2.863 8.375)" width="4.02px"/><path d="M 2.274 0 C 0.899 0 0 0.904 0 2.089 C 0 3.25 0.871 4.179 2.221 4.179 L 2.247 4.179 C 3.648 4.179 4.521 3.25 4.521 2.089 C 4.495 0.904 3.649 0 2.274 0 Z" fill="rgb(255, 255, 255)" height="4.17876px" id="VmOsKv4kO" transform="translate(2.625 2.545)" width="4.52095px"/><path d="M 7.641 0 C 5.509 0 4.554 1.173 4.019 1.996 L 4.019 0.284 L 0 0.284 C 0.053 1.419 0 12.376 0 12.376 L 4.019 12.376 L 4.019 5.623 C 4.019 5.262 4.045 4.9 4.151 4.642 C 4.442 3.92 5.103 3.172 6.214 3.172 C 7.667 3.172 8.25 4.282 8.25 5.907 L 8.25 12.376 L 12.269 12.376 L 12.269 5.442 C 12.269 1.728 10.286 0 7.641 0 Z" fill="rgb(255, 255, 255)" height="12.37626px" id="n1XUbhaq0" transform="translate(9.105 8.09)" width="12.268830000000001px"/></g></g></g></g></svg>)