Corporate Trustee Family Trust: Your Australian Business

Unlock benefits of a corporate trustee family trust for your Australian business. Guide covers 2026 costs, asset protection & tax implications.

Ansh Malhotra

Your business is doing better than it did two years ago, but the finances feel less clear, not more. Profit is showing up on the P&L. Cash isn't always showing up in the bank. You're thinking about buying property, bringing family into the ownership picture, protecting assets, and making sure the structure still works if something happens to you.

That's usually when the trust question lands on your desk.

For Australian founders, the primary concern isn't whether a family trust appears impressive. It's whether the structure helps you protect wealth, move cash sensibly, keep records clean, and hand control over without creating a mess later. The choice between an individual trustee and a corporate trustee affects all of that. It changes how risk sits, how decisions are documented, and how easy it is to keep the business and family group organised as things grow.

Table of Contents

Choosing Your Trust Structure Is More Than a Legal Formality

A common founder scenario goes like this. The trading business is growing. Stock levels are higher than they used to be, payroll is bigger, and the owner starts thinking beyond this quarter's BAS. They want better asset protection, more control over how family wealth is held, and a structure that won't unravel when succession becomes real rather than theoretical.

That's where a corporate trustee family trust starts to move from legal admin into strategic finance.

A family trust isn't just a box you tick because your accountant or lawyer suggested it. It sits underneath decisions about retained profits, beneficiary distributions, future investment assets, and who controls the structure if the founder steps back. If the trust holds business interests, those decisions affect lending conversations, boardroom clarity, and how easy it is to explain the group structure to bankers and advisers.

Founders sometimes look at offshore commentary to understand broad trust concepts, especially where family business governance is involved. If you want a non-Australian comparison point on how trust rules can shape control and succession, this guide to trust laws for Florida family businesses is useful context. The legal systems are different, but the commercial question is familiar. Who controls the assets, under what rules, and what happens when family and business interests overlap?

The decision usually appears when complexity rises

The trigger is rarely abstract. It's usually one of these:

The business has value now: You're no longer protecting an idea. You're protecting contracts, retained earnings, equipment, inventory, and future sale value.

The founder wants cleaner separation: Personal assets, business assets, and family investments shouldn't sit in a loose pile.

Family wealth planning becomes urgent: A spouse, adult children, or a future transfer of control changes the risk of keeping everything informal.

Tax planning gets more deliberate: Distribution strategy starts to matter, which is why broader tax planning strategies for Australian businesses usually need to be considered alongside the trust structure itself.

Practical rule: If the structure affects who controls cash, who bears risk, and how ownership passes on, it's not just legal paperwork.

The founders who handle this well don't ask, “Should I have a trust?” They ask better questions. Who should act as trustee? What level of liability am I carrying personally? How much administration can the business support? And will this still make sense when the business is twice the size it is today?

Individual vs Corporate Trustee A Clear Comparison

An individual trustee is the person who legally holds and manages the trust assets for the beneficiaries. A corporate trustee is a company that plays that role instead, with the directors controlling the company.

The easiest way to think about it is this. With an individual trustee, you personally stand at the front of the structure. With a corporate trustee, you create a dedicated vehicle to stand there for you.

Why the trustee choice changes the outcome

In Australia, a family trust is not a separate legal entity; instead, the trustee holds assets for beneficiaries. Advisory guidance also stresses that the economic value usually comes from discretionary distribution, not automatic tax minimisation. The trustee can allocate income to family members in lower tax brackets, which can improve after-tax outcomes when used properly, as outlined by LegalVision on leveraging a family trust for business structuring.

That point matters because many founders misunderstand what they're buying. They think they're choosing between two bits of paperwork. They're choosing who carries legal responsibility and how the trust behaves in real life.

A good plain-English explainer from a US perspective on institutional fiduciaries is this piece on understanding trust companies. The terminology differs from Australia, but it helps show why some families prefer a dedicated vehicle rather than a person wearing every hat.

Here's a quick visual before the detail.

Individual Trustee vs Corporate Trustee at a Glance

Feature | Individual Trustee | Corporate Trustee |

|---|---|---|

Who acts as trustee | One or more people act personally | An ASIC-registered company acts as trustee |

Legal separation | Less separation between the person and the role | Stronger separation between the trustee vehicle and the individuals behind it |

Asset handling | Greater risk of blurred lines if records are sloppy | Cleaner partitioning of trust assets from personal assets |

Succession | Change can be cumbersome if a trustee dies, resigns, or loses capacity | Company continues to exist, so control can shift by changing directors |

Administration | Simpler at first glance | More moving parts, including company compliance |

Cost | Lower setup burden in many cases | Higher setup and ongoing administration burden |

Founder optics | Can feel informal and familiar | Usually feels more structured to advisers, lenders, and successors |

Best fit | Small, simple arrangements with low complexity | Growing businesses, family groups, and founders planning for continuity |

A few trade-offs matter more than the rest.

Personal exposure: An individual trustee often feels simpler because there's no extra company. Simpler doesn't always mean safer.

Control mechanics: With a corporate trustee, the founder often remains in control as director, but the control sits inside a company structure rather than directly in their own name.

Governance quality: A corporate trustee usually forces better habits. Separate bank accounts, separate records, formal resolutions, and clearer authority lines.

The structure that feels slightly more annoying in year one is often the one that causes fewer headaches in year five.

For a busy founder, that's the true comparison. Individual trustees can work. A corporate trustee family trust usually works better when the business has material value, multiple stakeholders, or any serious succession intent.

Asset Protection and Succession With a Corporate Trustee

When founders choose a corporate trustee, they're usually trying to solve two problems. They want better separation between trust assets and personal risk, and they want a structure that can survive changes in people.

That's why this isn't just an estate planning conversation. It's an operating model decision.

Why separation matters in practice

In Australia, a corporate trustee is typically structured as an ASIC-registered company with at least one director. It holds trust assets as a separate legal entity, which improves asset partitioning and reduces the risk of mixing personal and trust property. Its ongoing existence also makes succession materially cleaner than using an individual trustee, as explained by The Gild Group's comparison of corporate and individual trustees.

That separation matters most when things go wrong.

If a business owner runs everything loosely, personal and trust dealings can start to overlap. A payment comes from the wrong account. A loan is poorly documented. An asset sits in the trust but gets treated like it's personally owned. Those mistakes don't just create accounting problems. They weaken the practical protection the structure was meant to provide.

Three operational habits make the structure hold up:

Separate banking: The trust should have its own bank account and transactions should be traceable.

Clean balance sheet treatment: Loans, drawings, and beneficiary entitlements need to be recorded properly.

Formal decision records: Minutes and resolutions shouldn't be reconstructed months later from memory.

Succession is cleaner when the trustee survives the people

Many founders often underestimate the value of a corporate trustee family trust.

An individual trustee can become unavailable. They can die, lose capacity, resign, or become difficult to deal with. Once that happens, changing the trustee can trigger delay, legal work, and confusion about who now controls the trust assets. If the trust holds shares in an operating company, that disruption can spill into the business itself.

A corporate trustee doesn't solve every succession issue, but it does make the mechanics cleaner. The company remains. Control can change through director appointments and company records rather than rebuilding the trust's legal footing from scratch.

That's useful in several situations:

Founder retirement: Control can move gradually rather than in one abrupt legal event.

Next-generation involvement: Adult children can be introduced through governance rather than immediate beneficial ownership changes.

Unexpected incapacity: The structure has a clearer pathway for continuity if the founder can't act.

A trust deed can set the rules, but the trustee structure determines how painful those rules are to administer when life changes.

From a CFO perspective, cleaner succession has a direct financial benefit. Banks, buyers, and advisers value continuity. If ownership and control can be explained clearly, the business is easier to fund, easier to diligence, and easier to transition.

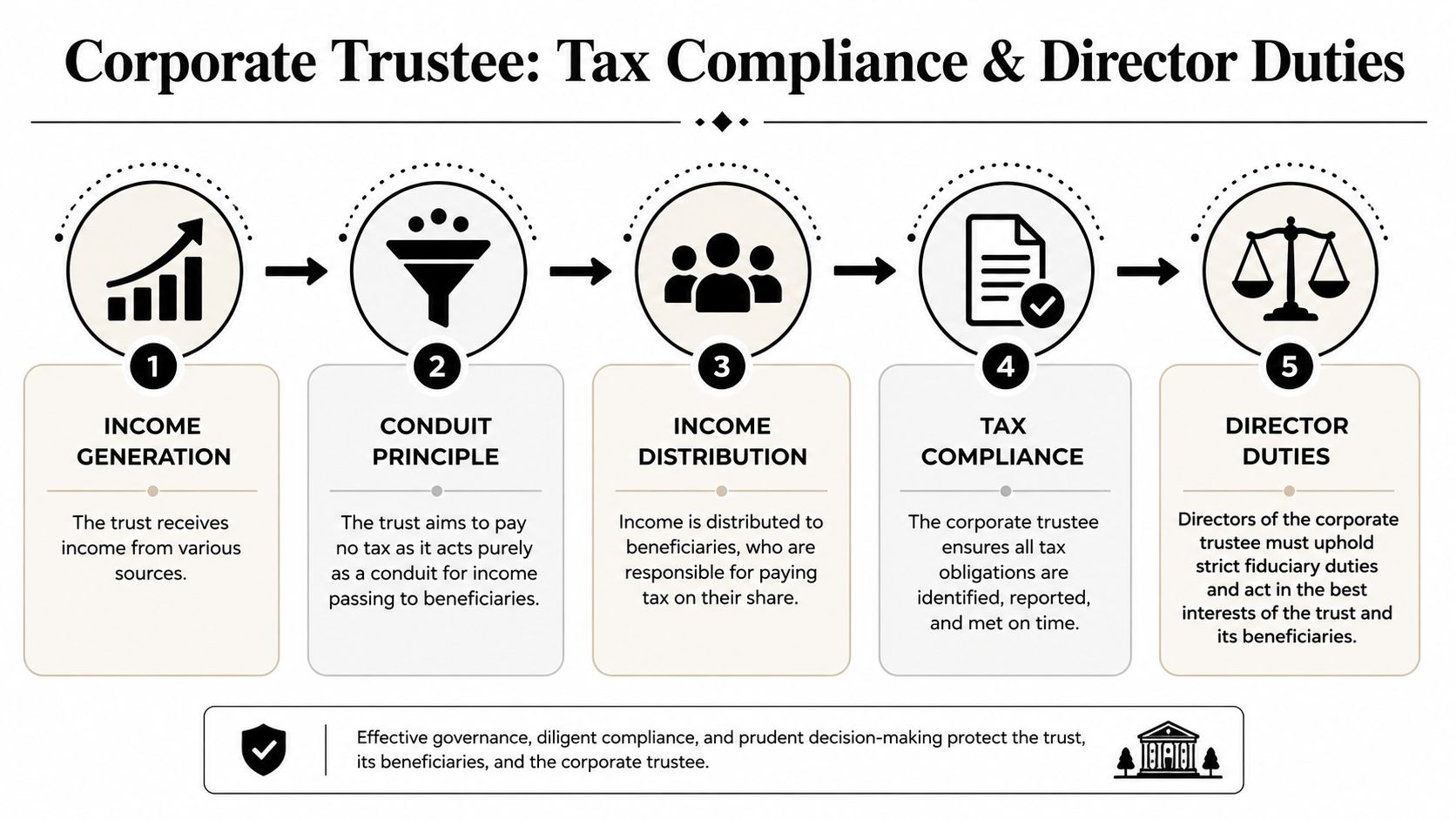

Navigating Tax Compliance and Director Duties

A corporate trustee family trust can improve control. It also creates obligations that founders can't treat as background admin.

The tax work happens every year. The governance work happens every time the trustee makes a decision.

The annual tax cycle founders need to control

For Australian family trusts, the tax mechanics are driven by annual trust-tax treatment. The trust must lodge a return and distribute income where possible. Any undistributed income can be taxed at the highest marginal rate, which is why timely distribution resolutions matter for reducing tax leakage, as outlined by LegalVision on corporate versus individual trustee tax treatment.

That's not a technical footnote. It's a cash-flow control issue.

When the trustee doesn't deal with distributions properly, the family group can lose cash unnecessarily. The P&L may still look respectable, but after-tax cash ends up worse than it needed to be. I've seen founders focus heavily on sales growth while ignoring year-end trust decisions that affect how much cash the group retains.

A disciplined annual rhythm usually includes:

Interim review before year end

Estimate trust income early enough to make decisions deliberately, not in a panic.Beneficiary planning

Check who can receive distributions under the deed and what outcome the family group is trying to achieve.Trustee resolution preparation

Ensure the trustee's decision is documented on time and aligns with the deed.Return and ledger follow-through

Record entitlements properly so the tax decision matches the accounting records.

Director duties are active, not decorative

Directors of a trustee company can't treat the role as ceremonial. If you're the director, you are the decision-maker behind the trustee.

In practical terms, that means:

Acting in good faith: Decisions should be made for the trust's proper purpose and in line with the deed.

Keeping proper records: Accounts, resolutions, supporting documents, and company records need to be current.

Separating roles clearly: Founder, shareholder, director, beneficiary, and manager are not interchangeable hats.

Reviewing decisions before cash moves: If money is being advanced, distributed, or reinvested, document why and under what authority.

If you need a plain-English refresher on the governance side, this guide on what a director in a company actually does is a useful starting point.

One warning: The structure only protects you if you respect the structure. Sloppy records and informal decisions are how founders lose the benefit they paid to create.

The founders who stay on top of this usually build a simple compliance calendar. Not a fancy one. Just a repeatable process that links tax planning, board-style approvals, and year-end reporting.

The Real Costs and Hidden Pitfalls to Avoid

A corporate trustee is often the better long-term structure for a growing founder. It still has a cost. It also creates friction if the business owner expects the trust to behave like a personal wallet.

That's where many setups go sideways.

The upfront cost is real, but so is the cost of getting it wrong

A practical Australian benchmark from North Advisory is that establishing a family trust with a corporate trustee typically costs around A$1,500 to A$2,500 in legal and administrative fees, which is a useful baseline when weighing structure against complexity and compliance cost, according to North Advisory's guide on the value of a family trust for your business.

That amount won't decide the issue on its own. What matters is whether the structure matches the value and risk profile of what it's holding.

If the trust is expected to hold meaningful business interests, investment assets, or future family wealth, the setup cost is usually the easy part. The harder question is whether the founder is willing to maintain the discipline that comes with it.

Where founders create friction without realising it

The common problems aren't exotic legal failures. They're ordinary operating mistakes.

Pitfall | What it looks like in practice | Why it hurts |

|---|---|---|

Treating trust cash as personal cash | Taking money out casually, then trying to explain it later | Creates record-keeping issues and weakens discipline |

Poor documentation | Minutes and resolutions are missing or created after the event | Makes tax and legal positions harder to defend |

Blurry entity boundaries | Business expenses, personal expenses, and trust expenses overlap | Reporting becomes unreliable |

Ignoring liquidity needs | The trust holds value, but available cash is tight | Founders feel “asset rich, cash poor” |

No succession process | Everyone assumes they know what happens next | Conflict rises when a change is forced |

The cash-flow issue deserves more attention than it usually gets.

A trust can hold valuable assets while the founder still feels squeezed for cash. That's especially common in inventory-heavy businesses where profit is tied up in stock, debtors, or expansion costs. The structure might be sound, but the founder hasn't modelled how money moves between the operating business, the trust, beneficiaries, and any related entities.

The trust doesn't create liquidity by itself. It only creates a framework. Cash still has to be planned, timed, and documented.

A practical decision checklist

A corporate trustee family trust is usually worth serious consideration if most of these are true:

You're protecting something material: The business or investment assets have enough value that informal ownership is no longer sensible.

You want cleaner succession: You care about what happens if a director changes, retires, or loses capacity.

You can handle added administration: Your finance function can support separate records, annual resolutions, and ongoing company compliance.

You need governance, not just tax outcomes: The structure has to support control, reporting, and long-term transfer of wealth.

You're willing to act formally: If you know you'll keep treating entities casually, the benefits shrink fast.

What doesn't work is choosing a corporate trustee because it sounds more prestigious, then refusing to run it properly.

Practical Setup and Strategic Financial Management

A good trust structure should make the business easier to manage, not harder to understand. The legal setup gets it started. Financial management is what makes it useful.

What setup usually looks like

At a high level, the process normally runs like this:

Get legal advice on the deed and roles: The deed needs to fit the family's intended control and beneficiary arrangements.

Register the corporate trustee company: The trustee is typically a company, so it needs to be established correctly.

Complete trust registrations and banking: The trust then needs its own administrative foundation, including tax registrations where required and separate accounts.

Set up accounting properly from day one: Xero, MYOB, or your chosen ledger should reflect the trust and the trading entities separately.

Document how money will move: Loans, distributions, and reimbursements should never be left to memory.

If you're trying to pull these parts into a broader owner-level framework, this guide on how to build a comprehensive financial plan is a useful complement to the structural decisions.

How a virtual CFO makes the structure useful

This is the part most founders miss. A trust doesn't manage itself commercially. It needs to connect to the operating rhythm of the business.

A virtual CFO helps by turning the structure into a decision framework:

Cash-flow planning: Forecast what can be distributed, retained, reinvested, or moved across the group without creating strain.

Reporting clarity: Separate operating performance from trust activity so you can see what the business is doing versus what the ownership structure is doing.

Scenario modelling: Test retirement, succession, dividend, and beneficiary strategies before they become urgent.

Documentation discipline: Tie financial decisions back to records, board actions, and year-end resolutions.

For founders who need that ongoing finance oversight, a virtual chief financial officer can sit between the lawyer, accountant, and owner to keep the structure commercially usable. Firms such as Nexist provide that kind of support by combining forecasting, reporting, cash-flow management, and operational finance process.

The payoff is straightforward. The corporate trustee family trust stops being a legal file in a drawer and starts acting like part of the business's financial architecture.

If you want help deciding whether a corporate trustee family trust fits your business, or you need the structure translated into practical cash-flow reporting and founder-level decision-making, talk to Nexist.

corporate trustee family trust, family trust australia, asset protection, business structuring, virtual cfo

" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="dSFdkJotL" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="wscNJE44G" transform="translate(0 0.129)" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="sTpjGo1tb" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="s7ffpmKOD" transform="translate(0 0.129)" width="24px"/><g d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.000006px" id="D0ecaHEcW" transform="translate(0 0)" width="24px"><path d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z" fill="rgb(55, 184, 218)" height="24.000006px" id="IPLFE6zXx" width="24px"/><path d="M 4.02 0 L 0 0 L 0 12.092 L 4.02 12.092 Z" fill="rgb(255, 255, 255)" height="12.09201px" id="FWhtzAyuY" transform="translate(2.863 8.375)" width="4.02px"/><path d="M 2.274 0 C 0.899 0 0 0.904 0 2.089 C 0 3.25 0.871 4.179 2.221 4.179 L 2.247 4.179 C 3.648 4.179 4.521 3.25 4.521 2.089 C 4.495 0.904 3.649 0 2.274 0 Z" fill="rgb(255, 255, 255)" height="4.17876px" id="VmOsKv4kO" transform="translate(2.625 2.545)" width="4.52095px"/><path d="M 7.641 0 C 5.509 0 4.554 1.173 4.019 1.996 L 4.019 0.284 L 0 0.284 C 0.053 1.419 0 12.376 0 12.376 L 4.019 12.376 L 4.019 5.623 C 4.019 5.262 4.045 4.9 4.151 4.642 C 4.442 3.92 5.103 3.172 6.214 3.172 C 7.667 3.172 8.25 4.282 8.25 5.907 L 8.25 12.376 L 12.269 12.376 L 12.269 5.442 C 12.269 1.728 10.286 0 7.641 0 Z" fill="rgb(255, 255, 255)" height="12.37626px" id="n1XUbhaq0" transform="translate(9.105 8.09)" width="12.268830000000001px"/></g></g></g></g></svg>)