Non Concessional Contribution Cap 2026: Business Owner's

Master non concessional contribution caps for 2026. Understand rules, limits, and leverage after-tax contributions to boost your super as a business owner.

Ansh Malhotra

You've had a solid year. There's cash in the business or sitting in your personal account, and the usual options are staring at you: clear debt, buy stock, hold a buffer, invest outside super, or move money into super.

That last option gets treated like a tax trivia question. It isn't. A non concessional contribution is a capital allocation decision. For founders, that means one thing. You don't judge it by whether the ATO allows it. You judge it by whether it's the best use of cash after weighing tax efficiency against access, control, and business volatility.

If your company lives with uneven receivables, supplier pressure, payroll spikes, or lumpy inventory buys, locking personal cash into super can be smart or reckless. The difference is timing.

Table of Contents

Why After-Tax Super Contributions Matter for Founders

A founder finishes the year with surplus cash and usually asks the wrong first question. They ask, “How much can I put into super?” The better question is, “What job should this money do next?”

Sometimes the right answer is obvious. If the business is thin on working capital, the cash belongs outside super. If the company is stable, debt is under control, and the owner has too much wealth tied to the business, moving after-tax money into super can be one of the cleaner ways to build personal wealth away from operating risk.

That matters because many founders are asset rich in one place only: their company. They've built enterprise value, but their personal balance sheet is concentrated. A non concessional contribution helps shift some wealth from “all eggs in the business basket” into a different structure.

This is not a niche strategy

Treasury's historical data shows non-concessional contributions have been used at scale. In 2005–06, an estimated 2.4 million people aged under 65 made non-concessional contributions, totalling about $24.5 billion. Treasury also estimated that 51% of total NCC value was made by men, while the median NCC was $1,125 for women and $1,792 for men, according to Treasury's contribution distribution data.

That doesn't mean you should automatically do it. It means this is a mainstream planning tool, not a niche move for tax obsessives.

Practical rule: If most of your net worth still depends on next quarter's sales, supplier terms, or your own stamina, your first priority is balance-sheet resilience, not squeezing every available dollar into super.

Founders also benefit from looking outside the Australian system to sharpen how they think about retirement tax structures. If you want a useful cross-border comparison of how retirement-tax strategy can work in other systems, this guide on how to convert to Roth is worth reading.

And if your broader objective is building wealth outside the business with proper strategy rather than ad hoc transfers, working with a private wealth advisor can help connect super decisions to the rest of your personal balance sheet.

Defining Non Concessional Contributions

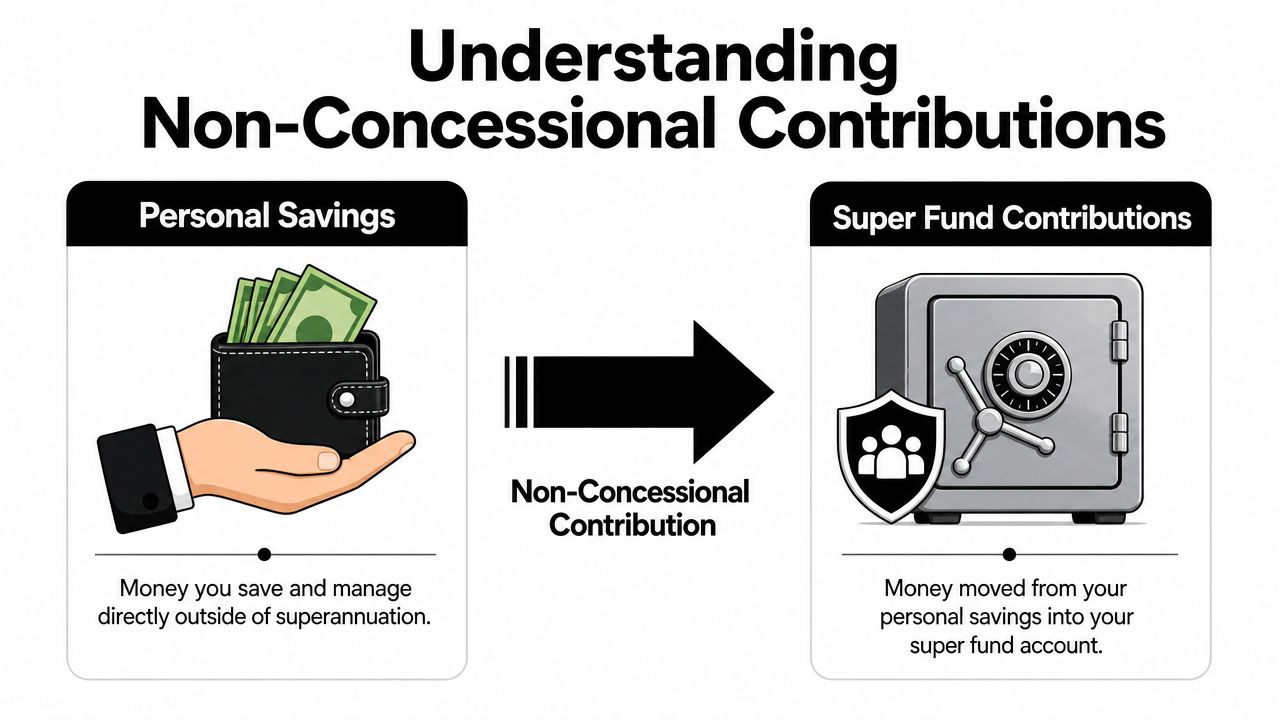

A non concessional contribution is money you put into super from funds that have already been taxed. That's the cleanest definition.

You're not claiming a tax deduction for it. You're not salary sacrificing it. You're taking money that already sits in your personal world and moving it into your super environment.

Think of it as moving money from one bucket to another

The simplest way to understand it is this. Picture two buckets:

your personal bank account or savings

your super fund

A non concessional contribution is just moving money from the first bucket to the second.

That sounds simple because it is simple. The complexity starts after that. Once the money is inside super, access becomes restricted by super rules. So while the transfer itself is straightforward, the consequence is major. You've traded flexibility for a concessionally taxed environment.

Put bluntly, this is not a parking account. It's a long-term decision.

How it differs from concessional contributions

Founders often muddle non concessional and concessional contributions because both end up in super. The source and tax treatment are different.

Feature | Non concessional contribution | Concessional contribution |

|---|---|---|

Money source | Personal money that's already been taxed | Pre-tax or deductible money |

Personal tax deduction | No | Often yes, depending on structure and compliance |

Main use | Move personal capital into super | Reduce taxable income while funding super |

Founder mindset | Wealth transfer from outside super | Tax planning plus retirement saving |

Big trade-off | Loss of liquidity and control | Contribution cap management and deduction strategy |

If you're a busy founder, here's the fast version. Concessional contributions are usually about tax deduction mechanics. Non concessional contributions are more about asset location. You're deciding where your money should live.

That distinction matters because the decision isn't technical. It's strategic. If you use after-tax cash for a non concessional contribution, you're saying that capital no longer needs to protect your household liquidity, support the business, or fund near-term opportunities.

Understanding the NCC Cap and Eligibility Rules

A founder sells a parcel of shares, has cash sitting in the offset, and wants to move part of it into super before 30 June. The transfer is easy. The mistake is assuming eligibility is easy too.

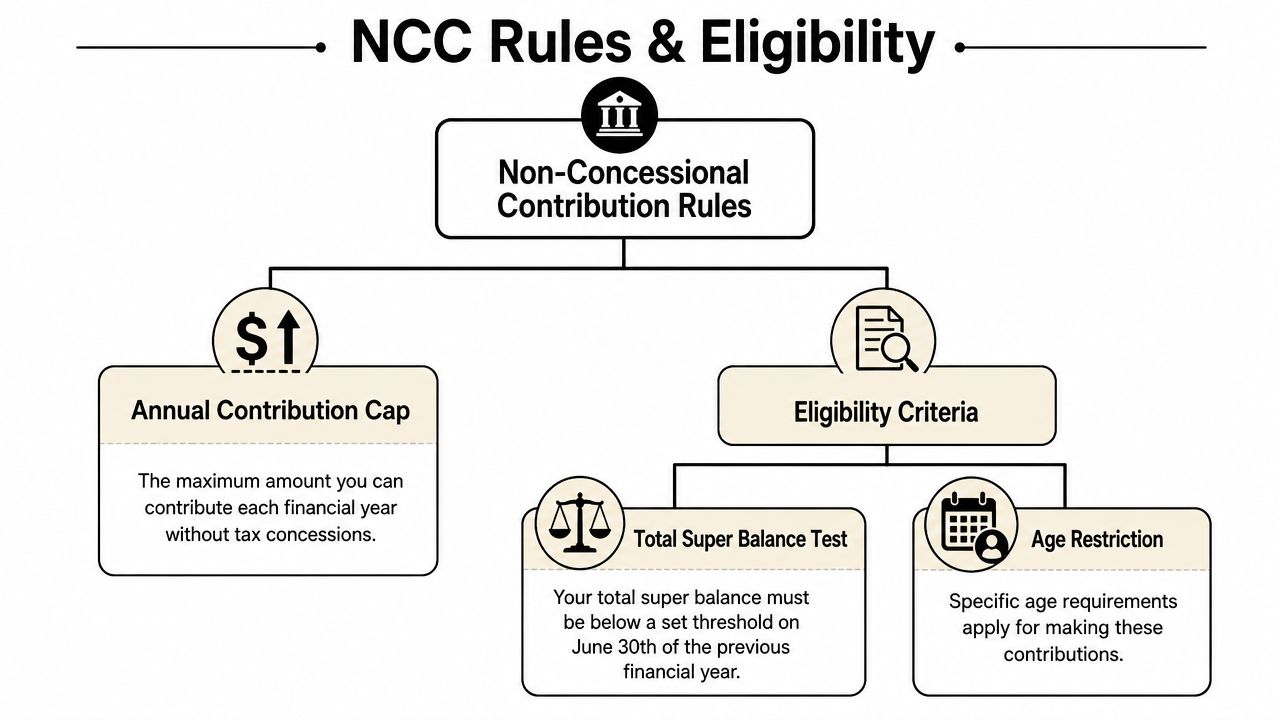

Most NCC errors come from poor capital allocation discipline. Owners focus on getting money into super and ignore the two filters that decide whether the contribution is even allowed. Your annual cap. Your total super balance.

The annual cap is the first gate

The non concessional cap is indexed over time. For planning purposes, many advisers expect it could rise to $130,000 from 1 July 2026, up from $120,000 in 2025-26, because these thresholds are reviewed and adjusted in line with indexation. Treat that as a planning assumption, not a locked fact.

The practical point is simple. Financial year timing changes your available cap. If you are deciding whether to contribute in June or July, you are not just choosing a date. You are choosing which year's limit applies.

For founders, that is a cash decision before it is a super decision. Money sent to super stops funding wages, inventory, tax reserves, and deal capacity. Set the target year first. Then decide whether the business and household can afford the transfer.

Your balance can shut the door completely

The cap alone does not give you the right to contribute. Your total super balance can reduce your NCC cap, or wipe it out for the year altogether if you are already at the relevant threshold.

Business owners often fall into this trap. They know the annual cap. They have not checked the balance test. Then they move cash based on a rule they only half understood.

Use this sequence instead:

Pick the financial year first. Do not guess which cap applies.

Confirm your total super balance before contributing. Close enough is not good enough.

Decide the amount last. The contribution size only matters after the first two checks.

If you are weighing after-tax contributions against pre-tax options in the same year, map both together. Founders often get a better result by pairing NCC decisions with carry forward concessional contribution planning, instead of treating them as separate admin tasks.

If your balance is near a threshold, stop relying on memory or last year's numbers. Check the current position first, then move cash.

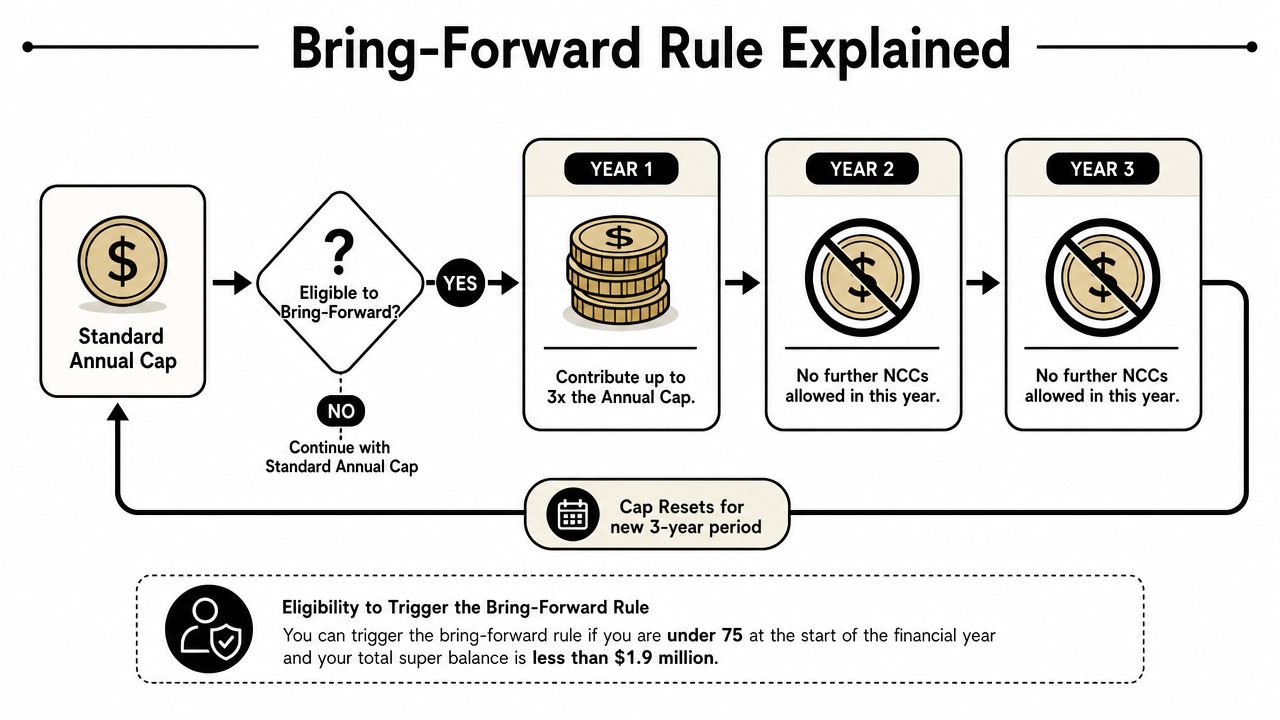

Using the Bring-Forward Rule to Accelerate Savings

The bring-forward rule is the tool founders usually reach for after a one-off capital event. A business sale. A property settlement. A windfall. A year where personal cash suddenly becomes abundant.

Used well, it lets you move more capital into super sooner. Used badly, it can trap funds you should've kept available.

Two founders make two very different moves

Founder one runs a steady business with predictable drawings and contributes after-tax amounts progressively when personal surplus appears. That approach is boring. Boring is often good. It preserves flexibility and keeps contribution decisions tied to actual cash generation rather than optimism.

Founder two sells an asset, receives a lump sum, and wants to accelerate retirement savings in one move. In such circumstances, the bring-forward rule can be useful. Instead of stretching contributions over multiple years, they may be able to pull future years forward and make a larger after-tax contribution in the first year, subject to eligibility and balance-based limits.

The strategic difference isn't just size. It's optionality. Founder one keeps more room to change course if trading conditions worsen. Founder two gets money into super faster, but gives up some future contribution flexibility because part of the future cap is effectively used early.

When accelerating makes sense

The bring-forward rule suits founders who can say yes to most of these:

Personal liquidity is already strong. They won't need this cash for living costs or emergency support.

The business no longer depends on owner cash injections. Working capital is funded properly.

A major capital event has created surplus outside normal trading. The contribution isn't coming from money the business may soon need back.

Their super balance position supports the strategy. They've confirmed eligibility before acting.

What I tell founders is simple. Don't use an accelerated super strategy to solve a tax itch when the business still has cash-flow swings. Use it when the business is already stable and the owner wants to shift excess capital into a long-term structure.

A larger permitted contribution doesn't automatically make it the right contribution.

Another practical point. Once you trigger a bring-forward arrangement, your future room changes. That's why timing around asset sales, distributions, and personal cash reserves matters more than the contribution form itself. This is one of those decisions where the paperwork is easy and the judgment is hard.

Real-World Scenarios for Business Owners

Rules don't make decisions. Context does. The same non concessional contribution can be sensible for one founder and a poor move for another.

Ecommerce founder with cash tied to stock

An ecommerce owner has had a profitable run. Their accountant says super is tax effective, which is true in broad terms. But this founder also has long supplier lead times, ad spend that needs front-loading, and a warehouse full of slow-moving SKUs.

For this person, I'd usually favour caution. Inventory-heavy businesses can look profitable while starving for cash. If personal cash may need to support stock buys, debt reduction, or a rough sales quarter, a non concessional contribution is lower priority.

The wrong move here is confusing accounting profit with deployable cash.

Service business owner after a sale event

A service firm owner sells part of the business or exits fully. Their operating risk drops sharply. The business no longer needs them to top up payroll or absorb client payment delays.

That's the profile where an after-tax contribution often makes more sense. They've turned business value into personal liquidity. The question shifts from “Can the business spare it?” to “How much personal capital should remain outside super for flexibility?”

For this founder, the answer is usually to carve the pool into separate jobs: some for near-term liquidity, some for investment flexibility, and some for super.

Startup founder with first meaningful personal liquidity

A startup founder finally has cash after years of low drawings. They're emotionally ready to “do the smart adult thing” and fund super properly.

That instinct is good, but early-stage founders still need a high tolerance for uncertainty. Capital calls happen. Hiring plans change. Runways compress. A founder with volatile income should resist the urge to lock up too much too quickly.

A measured contribution can still be sensible. An aggressive one often isn't.

A quick founder filter

Ask these before you move money:

If sales fell suddenly, would I wish I still had this cash personally?

If a lender tightened terms, would this contribution feel clever or painful?

Am I building retirement assets, or am I reacting to a good month?

Those questions cut through most bad decisions fast.

Key Planning Considerations and Potential Pitfalls

A founder has a cash surplus after a strong quarter. The temptation is obvious. Push the money into super, get the tax benefits, and call it disciplined planning.

That can be the wrong move.

A non concessional contribution is not just a tax decision. It is a capital allocation decision. Once that cash goes into super, it stops being available for payroll shocks, supplier pressure, debt reduction, and opportunistic growth. If the business or your household may need that liquidity, keep the money outside super.

Tax efficiency is only one part of the decision

Super can be tax effective. That does not make it the best use of cash.

Put the contribution behind these uses of capital if they are still underfunded:

Working capital for the business

A personal emergency buffer

Repayment of expensive debt

Expansion projects with a clear and believable return

Cash reserves for uneven founder income

This is the standard I recommend. Only contribute after-tax money to super when the cash has already lost the contest against those alternatives.

The cap settings can also shape timing. If the annual non concessional cap rises in future, including the projected increase to $130,000 from 1 July 2026, that creates a real planning question. Contribute earlier under current rules, or wait and preserve liquidity for a period that may matter more to the business. The right answer depends on your cash runway, not your enthusiasm for tax efficiency.

The expensive mistakes are usually simple

Founders rarely blow this up through complex structuring. They usually get caught by sloppy execution or bad timing.

Watch for these failure points:

Assuming you are eligible without checking your total super balance

Sending money near year-end and guessing which financial year it lands in

Treating super planning separately from business cash-flow planning

Making a large contribution after one unusually good year

Forgetting that money inside super is harder to access when conditions change

Large balances create another layer of planning. If extra super contributions could push you closer to broader super tax issues, use a Division 296 calculator for high-balance super planning before you commit more capital.

My recommendation is simple. Do not make a non concessional contribution because it feels prudent. Make it because the cash is genuinely surplus to your business, your household, and your near-term plans.

Making and Tracking Your Contributions

Execution should be simple. If it feels messy, stop and verify before money moves.

Use this checklist:

Check your total super balance first. Confirm the figure through your records and super reporting. Don't rely on memory.

Choose the financial year deliberately. If you're contributing near year-end, timing can affect which cap period applies.

Confirm with your fund how to pay. Most funds provide specific payment methods and member references.

Transfer the money from the correct source. Keep the payment trail clean and identifiable.

Record the contribution type properly. A pure non concessional contribution is different from a deductible personal contribution.

Don't file the wrong paperwork. A Notice of Intent is relevant to deductible contribution arrangements, not to a pure after-tax non concessional contribution.

Check that the fund received and allocated it correctly. Payment sent is not the same as contribution processed.

Keep evidence. Save confirmations, receipts, and correspondence.

If you're a founder, do one more step. Put the contribution decision into your cash-flow model before you make it. If the model looks tighter than you expected, that's your answer.

A smart super strategy should strengthen your overall position, not weaken your flexibility.

If you want help deciding whether a non concessional contribution fits your cash-flow reality, Nexist can help you weigh it like a CFO would. That means looking at working capital, debt, owner drawings, runway, and personal wealth strategy together, so you don't make a tax-smart move that creates a cash problem later.

non concessional contribution, superannuation, bring forward rule, smsf strategy, business owner finance

" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="dSFdkJotL" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="wscNJE44G" transform="translate(0 0.129)" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="sTpjGo1tb" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="s7ffpmKOD" transform="translate(0 0.129)" width="24px"/><g d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.000006px" id="D0ecaHEcW" transform="translate(0 0)" width="24px"><path d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z" fill="rgb(55, 184, 218)" height="24.000006px" id="IPLFE6zXx" width="24px"/><path d="M 4.02 0 L 0 0 L 0 12.092 L 4.02 12.092 Z" fill="rgb(255, 255, 255)" height="12.09201px" id="FWhtzAyuY" transform="translate(2.863 8.375)" width="4.02px"/><path d="M 2.274 0 C 0.899 0 0 0.904 0 2.089 C 0 3.25 0.871 4.179 2.221 4.179 L 2.247 4.179 C 3.648 4.179 4.521 3.25 4.521 2.089 C 4.495 0.904 3.649 0 2.274 0 Z" fill="rgb(255, 255, 255)" height="4.17876px" id="VmOsKv4kO" transform="translate(2.625 2.545)" width="4.52095px"/><path d="M 7.641 0 C 5.509 0 4.554 1.173 4.019 1.996 L 4.019 0.284 L 0 0.284 C 0.053 1.419 0 12.376 0 12.376 L 4.019 12.376 L 4.019 5.623 C 4.019 5.262 4.045 4.9 4.151 4.642 C 4.442 3.92 5.103 3.172 6.214 3.172 C 7.667 3.172 8.25 4.282 8.25 5.907 L 8.25 12.376 L 12.269 12.376 L 12.269 5.442 C 12.269 1.728 10.286 0 7.641 0 Z" fill="rgb(255, 255, 255)" height="12.37626px" id="n1XUbhaq0" transform="translate(9.105 8.09)" width="12.268830000000001px"/></g></g></g></g></svg>)