Invoice Payment Terms: A Guide to Better Cash Flow

Master your cash flow with this guide to invoice payment terms for Australian SMEs. Learn common terms, legal risks, and how to get paid faster in 2026.

Ansh Malhotra

You're probably in one of two positions right now. Sales look fine on paper, work is going out the door, invoices are being sent, but the bank balance still feels tighter than it should. Or you're spending far too much time checking who's overdue, nudging clients, and trying to guess whether enough cash will land before payroll, BAS, suppliers, and rent all hit at once.

That tension usually isn't caused by one dramatic mistake. It comes from small decisions that never felt strategic in the first place. One of the biggest is the wording and structure of your invoice payment terms. Most founders treat terms as admin. Finance teams know better. Terms shape when cash arrives, how easy it is to collect, and how much stress sits in the business week to week.

Done well, invoice payment terms become part of cash flow design. Done poorly, they turn accounts receivable into a waiting game. If you already track margin and sales but still feel pressure in the bank account, it's worth looking at the cash timing inside your cash conversion cycle. That's often where the leak sits.

Table of Contents

Stop Chasing Money and Start Managing It

A founder finishes a strong month, sends out a stack of invoices, and expects the pressure to ease. Then the next week arrives. Wages are due, supplier accounts need attention, and a few large customers haven't paid because their invoice said “Net 30” but nobody defined the actual date, the reminder process, or what happens when that date passes.

That's where cash flow stress starts to feel personal. You've done the work. The revenue exists. But the money is still in someone else's bank account.

Invoice payment terms are often treated like boilerplate. They sit at the bottom of the invoice, copied forward from an old template, rarely reviewed, and almost never connected to the broader finance plan. That's a mistake. Terms are one of the few levers a business can adjust quickly without changing its product, team size, or cost base.

Practical rule: If your invoice terms don't change behaviour, they're not doing their job.

The best operators don't just ask, “What should this invoice say?” They ask better questions. How quickly do we need this cash? Which customers can handle shorter terms? Where are disputes starting? Which invoices should require a deposit, a milestone schedule, or immediate payment?

A business with loose terms usually ends up with loose collections. Staff improvise. Customers interpret wording differently. Forecasts become educated guesses. The owner steps in to chase money manually, which is expensive in a way that often goes unmeasured.

A business with clear terms behaves differently. The due date is known. The follow-up sequence is known. The escalation point is known. Cash doesn't become perfectly predictable, but it becomes far more manageable.

That shift matters. It turns payment terms from passive text into an active operating decision.

Deconstructing Invoice Payment Terms

Think of invoice payment terms as the rules of the game for getting paid. If the rules are vague, every invoice becomes a negotiation after the work is done. If the rules are clear, both sides know what happens, when it happens, and how payment should be made.

The due date matters more than the shorthand

Many businesses rely on terms like Net 7 or Net 30 and assume that's enough. It often isn't. Australian SMEs should treat payment terms as a working-capital lever, not just an invoice field. B2B invoices typically specify the invoice date, exact due date, discounts for early settlement, accepted payment methods, and late-payment penalties. It's also better to state the calendar due date explicitly rather than only using shorthand like “Net 30”, because that reduces ambiguity and disputes, as outlined in Sage's guidance on invoice payment terms and due dates.

A clear due date does two jobs. It tells the customer exactly when payment is expected, and it gives your finance process a fixed trigger for reminders, ageing, and escalation.

The other parts that make terms enforceable

A complete set of invoice payment terms usually includes several moving parts:

Accepted payment methods. If you want fast payment, remove friction. Spell out whether you accept bank transfer, card, or another method, and include the details the customer needs.

Early payment discounts. These can be useful when faster cash matters more than collecting the full amount on the standard cycle.

Late-payment penalties. These won't fix a weak collections process on their own, but they can set a firmer expectation.

Invoice date. This starts the timing clock. If the date is wrong or delayed, the whole collection cycle slips.

Supporting instructions. Purchase order references, approver names, and project identifiers can prevent an invoice from sitting in someone's inbox waiting for clarification.

Clear terms don't just help the customer pay. They help your team collect without improvising.

What works and what doesn't

What works is precision. “Payment due 14 May” works. “Net 14 from invoice date, payable by bank transfer to the account listed below” works even better.

What doesn't work is hoping shorthand will carry the meaning. “Due on receipt” can work for some businesses, but not if the customer's internal process requires approvals. “Net 30” can work too, but only if the due date is visible and the reminder cadence sits behind it.

The difference sounds small. In practice, it changes how confidently you can forecast incoming cash.

A Catalogue of Common Payment Terms

There isn't a single best option for every business. Good invoice payment terms reflect what you sell, who you sell to, how much bargaining power you have, and how much working capital the business can absorb.

Common Invoice Payment Terms Compared

Term | Meaning | Best For | Cash Flow Impact |

|---|---|---|---|

Payment on receipt | Payment is expected as soon as the invoice is received | Low-risk jobs, one-off services, small project work | Strongest immediate cash position if enforced |

Net 7 | Payment due within 7 days of invoice date | Fast-turn services, recurring retainers, customers with simple approval paths | Quick conversion of receivables into cash |

Net 30 | Payment due within 30 days of invoice date | Standard B2B arrangements where some flexibility is needed | Balanced, but still creates a funding gap |

Net 60 | Payment due within 60 days of invoice date | Larger corporate contracts or industries with slower pay cycles | Weaker cash position and more pressure on working capital |

Payment in advance | Full payment before work starts or goods are supplied | Custom work, high-risk customers, made-to-order supply | Best protection for cash and delivery risk |

Deposit plus balance | Part paid upfront, remainder due later | Projects with upfront labour or material cost | Reduces out-of-pocket exposure |

Milestone-based payments | Payments tied to defined project stages | Construction, consulting, creative, software implementation | Spreads cash inflow across delivery rather than waiting until the end |

End of month | Payment due at the end of the month under the agreed rule | Businesses aligned to monthly billing cycles | Can delay payment depending on invoice timing |

Split payments | Invoice broken into scheduled amounts | Longer engagements or high-value work | Improves cash timing compared with one final invoice |

Cash on delivery | Payment made when goods are delivered | Physical goods where delivery confirms fulfilment | Limits debtor exposure but may create sales friction |

Short terms suit speed and discipline

Payment on receipt and Net 7 work best when the job is short, the invoice amount is straightforward, and the customer isn't likely to push back on admin. Think trades, agencies on smaller projects, or service businesses billing frequent repeat work.

The advantage is obvious. You shorten the wait between delivery and cash. The challenge is that your internal process needs to be organised. If invoices go out late, short terms don't help much.

Standard terms help win some work, but they cost cash

Net 30 is often treated as the default because many customers recognise it. That doesn't make it harmless. Every extra day before payment leaves your business funding staff time, overheads, or inventory without cash in hand.

Net 60 is usually a commercial concession, not a neutral setting. It can make sense when a larger customer offers volume, strategic value, or longer-term stability. But if you accept it casually, you're effectively providing trade credit.

Longer terms can win deals. They can also push financing pressure back onto the supplier.

Upfront and staged terms protect margin

Payment in advance is the cleanest structure when the risk of delay, cancellation, or customisation sits with you. If the customer wants a custom product, reserved capacity, or specialised work, asking for cash before commencement is often sensible.

Deposit plus balance is a practical compromise. It works when you need commitment up front but don't want to block the sale with a full prepayment requirement.

Milestone-based payments are strong for project work because they match cash collection to delivery progress. Instead of waiting until the end and hoping approval lands quickly, you collect as value is created.

Terms should match the operating model

A wholesaler, agency, manufacturer, and consultant shouldn't all use the same invoice payment terms. The wrong choice creates avoidable pressure. The right one reduces friction while protecting cash.

If your current terms were inherited from old templates or copied from a larger competitor, they may fit your customers better than your own balance sheet.

How to Strategically Choose Your Payment Terms

A founder closes a good month on paper, then spends the next three weeks watching the bank balance tighten because invoices are sitting on Net 30 or Net 45. That gap is where payment terms stop being admin and start becoming a cash flow decision.

Start with the cash conversion cycle, not the template

Choose terms based on how long cash is tied up in your business. If wages, suppliers, subcontractors, or inventory have to be paid before the customer pays you, your invoice terms are part of your funding model.

That changes the question.

Instead of asking what sounds normal, ask how much trade credit the business can afford to offer without creating pressure elsewhere. If cash is tight, long terms can force bad decisions. Delayed tax payments, slower supplier payments, reduced marketing spend, or a heavier reliance on overdrafts and founder capital.

In practice, strong terms usually follow operating risk. Custom work often justifies a deposit. Larger projects are usually better billed in stages. Ongoing services are easier to manage with recurring monthly billing in advance or on short terms, rather than waiting until all work is complete.

Set a default policy, then make exceptions deliberately

Many businesses inherit terms from an old invoice template or from a large customer's procurement preference. That is backwards. Set a base position that fits your own cash cycle, then adjust for specific customer situations.

A useful framework looks like this:

Low-risk, repeat customers: standard credit terms where payment history supports it

New customers: shorter terms, upfront payment, or a deposit until behaviour is proven

Project work: milestone billing tied to clear deliverables or dates

Custom, reserved-capacity, or high-input work: deposit before commencement and staged payments through delivery

Large enterprise buyers: terms that reflect their approval process, but only after pricing the cash flow cost into the deal

This is a commercial judgment, not just a finance setting. If sales wants to offer longer terms to win a customer, the business should treat that as a concession with a cost attached.

Price the concession properly

Longer payment terms can help conversion. They can also transfer working capital pressure from the customer to you.

I usually advise founders to treat extended terms the same way they treat discounts. If a customer wants more time to pay, decide whether the margin, volume, retention value, or strategic fit justifies it. If it does, agree to it consciously. If it does not, hold the line or restructure the deal with a deposit, progress claims, or a narrower scope in the first phase.

Precision matters here. “Due on receipt,” “7 days from invoice date,” and “50% deposit, balance before delivery” give your team clearer triggers for follow-up than vague wording or inherited defaults.

This short explainer is useful if you want a quick finance refresher before reviewing your own terms:

Build terms that your systems can enforce

The best payment terms are the ones your team can apply consistently. If a term cannot be supported by your invoicing process, reminder workflow, approval checkpoints, and collection cadence, it will break down under pressure.

That is where automation becomes practical, not theoretical. Clear invoice dates, fixed due dates, deposit triggers, and milestone schedules are easier to load into accounting systems, schedule reminders against, and track in aged receivables. Ambiguous terms create manual follow-up, internal confusion, and slower collections.

Decision lens: Choose the shortest, clearest term your market will accept and your operations can enforce consistently.

Founders often look at payment terms as boilerplate. They are closer to a working capital policy. Set them with intent, review them by customer segment, and use them to control timing of cash, not just timing of invoices.

Australian Legal and Cash Flow Realities

Australian businesses operate in a payment environment that is more visible than many founders realise. The legal backdrop matters because it changes how payment behaviour is monitored and discussed, especially when small suppliers deal with large customers.

Why the Australian framework matters

In Australia, the formal legal framework around invoice payment terms is built around the Payment Times Reporting Act 2020, which came into force on 1 January 2021 and requires large businesses and government enterprises to report payment performance to the regulator. The scheme applies to entities with annual income of at least AU$100 million, which has created a national dataset around payment behaviour and made invoice timing a measurable cash-flow issue rather than just a contract detail, as described in this summary of the Payment Times Reporting Scheme in Australia.

For an SME, that doesn't mean every slow payment problem disappears. It does mean payment culture has more accountability around it when you supply into larger organisations.

The real financial effect of waiting longer

The operational impact is straightforward. If your customer pays later, you carry the business for longer.

A shift from Net 30 to Net 60 means the seller funds an extra month of operations before cash arrives. That can affect payroll timing, stock replenishment, tax planning, and debt usage. The issue isn't only profitability. It's the timing gap between earning revenue and receiving cash.

Here's how that plays out in practice:

A service business may complete the work this month but wait far longer to receive the cash.

A wholesale or manufacturing business may have already paid for materials, labour, and freight before the invoice is settled.

A founder drawing confidence from sales growth may still face pressure because receivables are stretching faster than collections.

Public reporting doesn't collect your money for you. It does make payment behaviour harder for large organisations to ignore.

What founders should do with that context

Australian SMEs should use this environment as an advantage in commercial discussions. If a large customer pushes for extended terms, that's a reason to negotiate structure, not just accept delay. You might not win a shorter final term, but you may win a deposit, stage billing, faster approval mechanics, or tighter invoice requirements.

Many founders miss the point. Legal context is useful, but cash discipline still comes from execution. Good invoice payment terms only help when they're matched with clean invoicing, fast issue dates, and consistent follow-up.

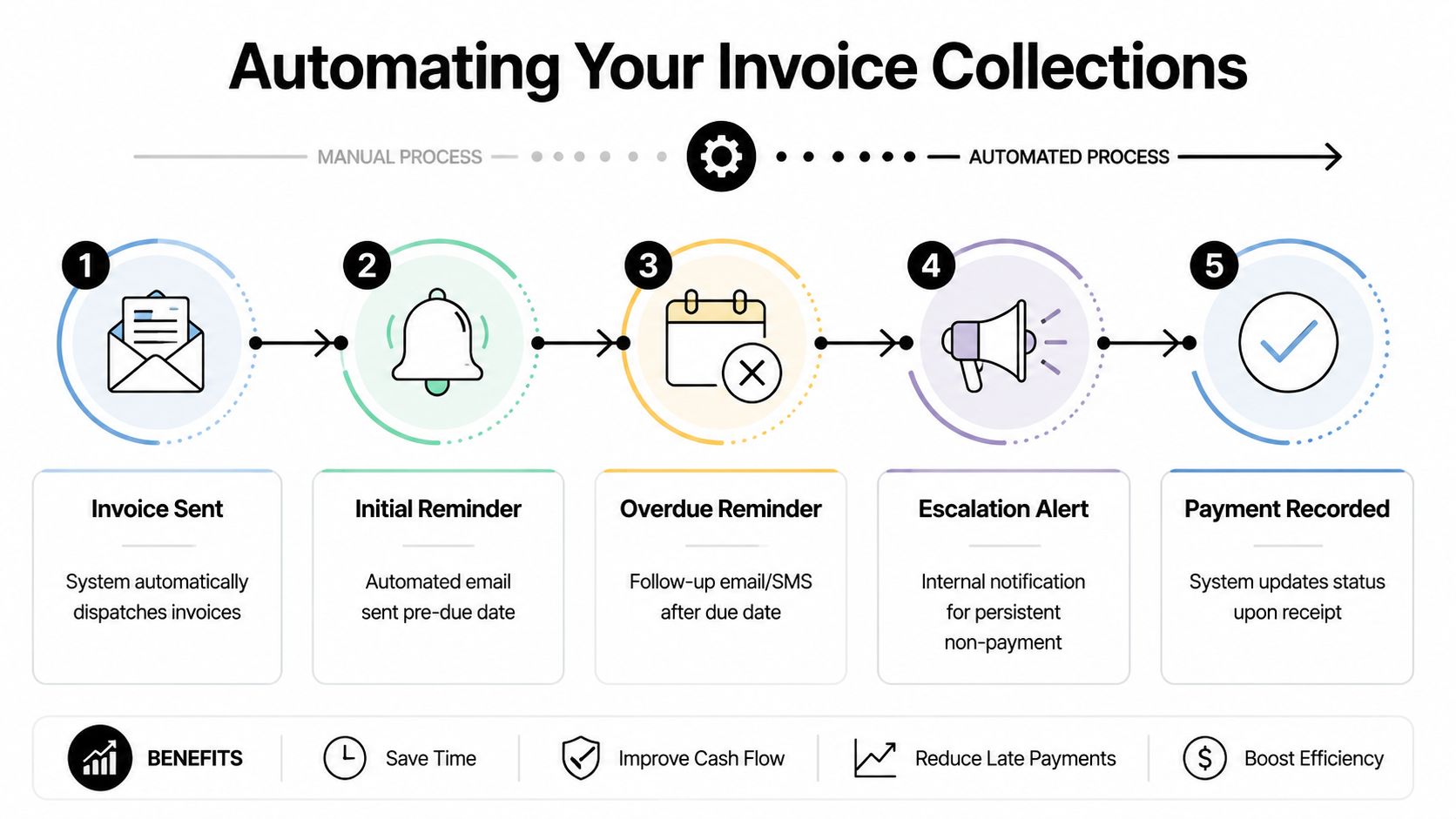

Automating Collections and Measuring Success

Most collection problems don't begin with a rude customer. They begin with a manual process. The invoice goes out late. The due date isn't clear. Nobody sends a reminder before the invoice becomes overdue. Then the owner steps in and spends Friday afternoon chasing money that software should have handled.

Australian businesses now have a better opportunity to fix that. The Australian Taxation Office continues to promote e-invoicing as a faster, safer way to exchange invoices, and broader government digital adoption has kept expanding. That matters because e-invoicing can reduce manual errors and speed up invoice processing, especially when businesses connect payment terms to reminders and approval workflows, as discussed in this article on e-invoicing and payment-term automation.

Build a collection system, not a reminder habit

A strong setup in Xero, MYOB, or QuickBooks usually includes:

Automatic invoice dispatch. The invoice is sent as soon as the trigger event happens, not when someone remembers.

Pre-due reminders. A polite prompt before the due date reduces “we forgot” delays.

Overdue workflows. The tone escalates in stages instead of relying on ad hoc follow-up.

Internal visibility. Someone in the business gets flagged when an account needs human intervention.

Payment reconciliation. Once funds arrive, the status updates quickly so your reporting stays clean.

That's the foundation. If your current process is inconsistent, start there.

Match the terms to the workflow

Many businesses lose the benefit of their invoice payment terms. They write one thing on the invoice, but the system behind it doesn't support collection. Net 7, deposit terms, split billing, and milestone invoices all need different triggers and templates.

For teams that want a firmer process and fewer awkward follow-ups, this guide on how to stop chasing client payments is a useful operational reference. It helps frame escalation as a system issue, not a personality test.

A more disciplined process usually includes:

A clear issue trigger tied to delivery, approval, or contract milestone.

Template-based reminders that use the exact due date.

Escalation rules for invoices that move beyond standard follow-up.

Review of dispute codes so repeated delay reasons can be fixed at the source.

The best collection workflow feels boring. That's a good sign. It means the process is doing the work.

Measure what the process is changing

If you want improvement to stick, measure it. Look at ageing, overdue patterns, dispute frequency, and how long receivables stay open. Many businesses also track Days Sales Outstanding as a way to understand how efficiently credit sales convert to cash.

What matters most is consistency. A clean accounts receivable management process gives you a repeatable way to see whether your chosen terms are producing faster, cleaner collections.

If the numbers don't improve, don't just chase harder. Review the term, the invoice timing, the customer onboarding process, and the reminder sequence.

From Terms on a Page to Cash in the Bank

Invoice payment terms aren't minor admin. They shape how long cash sits outside your business, how much pressure lands on the owner, and how reliable your forecasts really are.

The strongest approach is practical. Set terms that match the way your business operates. State the exact due date. Use structures like deposits or milestones when the delivery model calls for them. Build the reminders and escalation steps into software so collections don't depend on memory or mood.

If your invoicing workflow itself needs tightening, this walkthrough on how to process invoices is a helpful companion to the collection side of the process. Clean processing and strong terms work best together.

There's also a simple discipline that many founders overlook. Review your receivables by age, not just by total. A proper accounts receivable ageing report shows where payment terms are holding up and where they're falling short.

Good terms create clarity. Good systems turn that clarity into cash.

That's the difference between hoping invoices get paid and building a business that collects predictably. When cash arrives closer to when work is delivered, the business gets room to breathe. Decisions improve. Stress drops. Time comes back.

If you want a clearer view of where cash is leaking from your business, Nexist offers a 30-minute Business Scorecard that helps founders identify pressure points across receivables, margins, inventory, and process. It's a practical starting point if you want to turn finance from a source of stress into a system that puts real cash in the bank.

invoice payment terms, cash flow management, small business finance, accounts receivable, get paid faster

" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="dSFdkJotL" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="wscNJE44G" transform="translate(0 0.129)" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="sTpjGo1tb" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="s7ffpmKOD" transform="translate(0 0.129)" width="24px"/><g d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.000006px" id="D0ecaHEcW" transform="translate(0 0)" width="24px"><path d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z" fill="rgb(55, 184, 218)" height="24.000006px" id="IPLFE6zXx" width="24px"/><path d="M 4.02 0 L 0 0 L 0 12.092 L 4.02 12.092 Z" fill="rgb(255, 255, 255)" height="12.09201px" id="FWhtzAyuY" transform="translate(2.863 8.375)" width="4.02px"/><path d="M 2.274 0 C 0.899 0 0 0.904 0 2.089 C 0 3.25 0.871 4.179 2.221 4.179 L 2.247 4.179 C 3.648 4.179 4.521 3.25 4.521 2.089 C 4.495 0.904 3.649 0 2.274 0 Z" fill="rgb(255, 255, 255)" height="4.17876px" id="VmOsKv4kO" transform="translate(2.625 2.545)" width="4.52095px"/><path d="M 7.641 0 C 5.509 0 4.554 1.173 4.019 1.996 L 4.019 0.284 L 0 0.284 C 0.053 1.419 0 12.376 0 12.376 L 4.019 12.376 L 4.019 5.623 C 4.019 5.262 4.045 4.9 4.151 4.642 C 4.442 3.92 5.103 3.172 6.214 3.172 C 7.667 3.172 8.25 4.282 8.25 5.907 L 8.25 12.376 L 12.269 12.376 L 12.269 5.442 C 12.269 1.728 10.286 0 7.641 0 Z" fill="rgb(255, 255, 255)" height="12.37626px" id="n1XUbhaq0" transform="translate(9.105 8.09)" width="12.268830000000001px"/></g></g></g></g></svg>)