Accounts Receivable Management: A Playbook for Aussie SMEs

Master accounts receivable management with this practical playbook for Australian SMEs. Improve cash flow, reduce late payments, and reclaim your time.

Ansh Malhotra

You've probably lived this already. Sales are up, the P&L says the business is profitable, and yet payroll week still feels tight. BAS is due, suppliers want paying, and the cash in the account doesn't match the confidence the reports should give you.

That gap is usually sitting in debtors.

For Australian SMEs, accounts receivable management isn't a bookkeeping tidy-up. It's a working-capital system. If invoices go out late, contain errors, or sit unchallenged once overdue, cash gets trapped where you can't use it. Founders then solve the wrong problem. They cut spend, delay hiring, or lean on overdrafts when the problem is that revenue hasn't been converted into cash.

The practical question isn't just how to collect faster. It's how to collect profitably. Some invoices should be chased personally. Some should be automated. Some should move to a third party. Some should be written off before they drain more staff time than they're worth. That's the lens that matters.

Table of Contents

Why Your P&L Is Lying About Your Cash Flow

A profitable month can still produce a cash crisis. That's not a contradiction. It's how accrual accounting works. Your P&L records sales when you earn them, not when the customer pays you. If those invoices sit unpaid, your profit is real on paper but unavailable in the bank.

That's why founders get blindsided. They look at revenue, gross margin, and net profit, then wonder why cash still feels strained. The missing link is receivables. A debtor ledger is not a list of wins. It's a list of cash you haven't collected yet.

Late payments turn profit into pressure

In Australia, late payment is a major drag on small-business working capital. The ASBFEO has reported that around 60% of small business invoices are paid late, and the average late payment period is about 26 days beyond terms, as summarised in this Australian receivables overview. The same source notes that late payment costs Australian small businesses billions of dollars each year in lost productivity and financing strain.

That's the part many operators underestimate. Chasing debtors isn't just annoying. It takes owner attention, finance hours, and management energy away from pricing, delivery, hiring, and sales.

Practical rule: If you're regularly short on cash while showing profit, review debtors before you blame overheads.

For inventory-heavy businesses, the pain doubles. Cash is already tied up in stock, then more of it gets trapped in receivables. For service businesses, the issue often hides behind “good clients” who always pay, just never on time. In both cases, the business funds the gap.

What strong accounts receivable management actually changes

Good accounts receivable management improves one thing founders care about most. Cash certainty.

That means:

Invoices go out immediately: Not at month-end when someone gets around to it.

Terms are enforced consistently: Not renegotiated by silence.

Overdues are visible early: Not discovered after a supplier calls.

Collections are prioritised: Staff time goes to the balances most worth recovering.

The shift is operational as much as financial. Teams stop treating invoicing and collections like admin and start treating them like part of the cash conversion cycle. If you want a broader finance framework for that mindset, this guide to strategic and financial planning is a useful companion.

Most SMEs don't have a revenue problem. They have a conversion problem. They've made the sale, delivered the work, and lodged the invoice. The cash just hasn't landed.

Build Your AR Fortress with a Strong Credit Policy

Most debtor problems start before the first invoice is ever sent. They begin when a business gives terms too easily, accepts vague approval processes, or assumes a customer who sounds credible will behave like one.

A credit policy fixes that. Not a long corporate document nobody follows. A practical set of rules the sales team, finance team, and owner use.

Set rules before the sale gets emotional

Once the job is done or the stock is delivered, your influence decreases. Before that point, you can still shape the risk. That's why the strongest credit control happens at onboarding.

Australian policy settings have already recognised that payment behaviour affects business survival. The Productivity Commission has noted that long payment times and poor payment behaviour can strain SME cash flow, and Australia's Payment Times Reporting Scheme was introduced on 1 January 2021 to increase transparency around how quickly large businesses pay small suppliers, as outlined in this discussion of receivables and payment reform.

That matters for a founder because receivables performance is now a strategic metric, not just an accounting clean-up item.

What a workable SME credit policy should include

Don't overcomplicate this. A good SME credit policy usually fits on a few pages and covers the decisions that matter.

Who gets terms

New customers shouldn't automatically receive credit. Some should prepay. Some should pay a deposit. Some can earn terms after a period of clean payment behaviour.

Credit limits

Set an exposure ceiling per customer. If a client wants more work beyond that limit, they either pay down the balance or get management approval.

Payment terms

Keep terms explicit in quotes, proposals, service agreements, and invoices. If your documents conflict, customers will default to whichever version benefits them.

Evidence you'll check

For Australian SMEs, that can include ASIC register checks, trade references, signed account forms, and a review of whether the buying entity matches the trading name you've been given.

Who can approve exceptions

Sales teams should not be able to extend terms casually to close a deal. Exceptions need one owner.

The easiest bad debt to manage is the one you never approve.

Credit policy mistakes that create slow debtors

A lot of businesses think they have a collections issue when they have a customer-selection issue.

Common failures include:

Loose onboarding: No signed terms, no purchase order process, no verified entity details.

Unlimited exposure: Work keeps being delivered while old invoices stay unpaid.

Vague responsibilities: Sales assumes finance is handling it. Finance assumes the account manager is “keeping the relationship warm”.

No stop-work trigger: The customer can stay overdue without any commercial consequence.

A simple approval model

A practical model for SMEs is to divide customers into three lanes:

Customer type | Terms approach | Risk stance |

|---|---|---|

New or uncertain | Upfront payment or deposit | Protect cash first |

Established and reliable | Standard terms with set limit | Monitor monthly |

Slow-paying or disputed | Reduced terms or staged billing | Tight control |

This doesn't make you difficult to deal with. It makes you organised. Customers usually adapt quickly when your process is clear. They push boundaries when it isn't.

Optimise Your Invoicing for Faster Payments

If an invoice is unclear, incomplete, or hard to pay, the customer has a reason to delay. Sometimes that delay is genuine. Often it's just friction. Either way, you wait longer.

Fast collection starts with invoice quality. Not just the layout, but the surrounding payment process.

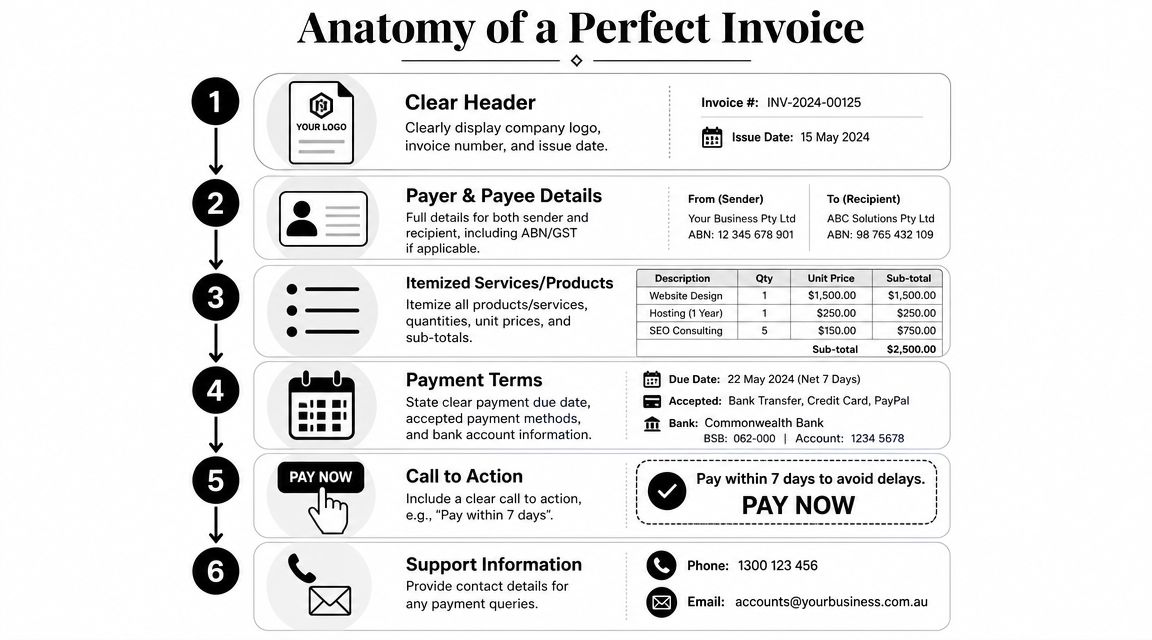

Build an invoice that removes excuses

A good invoice answers every question before the customer asks it.

Include:

Clear issuer details: Legal entity, ABN, contact details, and invoice number.

Accurate customer details: The correct legal name, contact, and delivery or job reference.

Specific line items: Enough detail for approval without creating clutter.

A visible due date: Not hidden in fine print.

Payment instructions: Bank details, payment link, accepted methods, remittance contact.

Supporting references: PO number, project code, site address, or timesheet reference where relevant.

If you invoice trades, agencies, wholesalers, or project-based service businesses, add whatever the customer's accounts payable team needs to approve it first time. Missing references create disputes that aren't really disputes. They're process failures.

Match invoice design with modern payment rails

Australia's payment environment is changing what “paid quickly” can look like. The New Payments Platform, PayTo-style account-to-account payments, and government-led e-invoicing adoption are all pushing businesses towards fewer invoice errors and faster payment flow, as discussed in this overview of modern receivables processes in Australia.

That doesn't mean technology fixes a messy process by itself. If invoice data is wrong, automation only sends wrong invoices faster. If payment rails aren't integrated, customers still face friction between receiving the bill and making the payment.

A fast payment method attached to a bad invoice doesn't produce fast cash. It produces a faster dispute.

For many SMEs, the best practical combination is:

structured invoice data

immediate digital delivery

simple account-to-account payment options

clean remittance handling

bank reconciliation that doesn't rely on someone guessing what came in

If you're improving the workflow behind that, this resource to discover invoice automation tips is worth reviewing.

A quick walkthrough helps here before the system goes live:

Timing matters as much as formatting

The best invoice in the world won't help if it goes out late. One of the simplest operating disciplines is to invoice on completion, on dispatch, on milestone sign-off, or on the agreed recurring billing date. Not “when admin catches up”.

That's especially important in hospitality supply, transport, and wholesale where billing volumes are high and small errors stack up quickly. The businesses that get paid faster usually aren't doing anything magical. They're issuing cleaner invoices sooner and making payment easy.

Automate Your Reminders and Dunning Process

Manual follow-up always starts with good intentions. Then the owner gets pulled into operations, the bookkeeper is waiting on context, and overdue invoices sit untouched until they become awkward.

Automation solves the consistency problem. Not the judgement problem. You still need human escalation for disputes, relationship-sensitive accounts, and larger balances. But the routine reminders should run without relying on memory.

Use a staged reminder sequence

A workable reminder cadence doesn't need to be aggressive. It needs to be predictable.

A simple model looks like this:

Pre-due reminder: Friendly message before the due date with invoice attached and payment options included.

Due-date reminder: Brief note confirming the invoice is due today and inviting the customer to raise any issue immediately.

Early overdue follow-up: Direct but calm message asking for payment timing and checking whether there's an approval problem.

Escalation sequence: Formal language, tighter deadlines, and internal review of whether supply should continue.

The tone should change as the account ages. The system should do that automatically.

Sample reminder language that works

Pre-due

Hi [Name], just a quick reminder that invoice [number] falls due on [date]. I've attached it here for convenience. If anything is missing for approval, let us know today.

Due date

Hi [Name], invoice [number] is due today. Payment details are included on the invoice. If payment has already been processed, please disregard this reminder.

Overdue

Hi [Name], invoice [number] is now overdue. Can you confirm payment status or advise if there's anything holding this up on your side?

That wording works because it's clear, not theatrical. It doesn't accuse the customer too early, and it doesn't leave the next step vague.

Where automation helps and where it doesn't

Automation is ideal for:

Routine reminders: Every customer gets a timely nudge.

Attachment handling: The right invoice and statement go with the message.

Task creation: If no response arrives, the system allocates a call or review task.

Audit trail: Your team can see every touchpoint in one place.

Automation is weak when:

A dispute needs context: Someone has to resolve the commercial issue.

The account is strategic: A relationship owner may need to step in.

The debtor is gaming the process: Standard reminders won't shift deliberate delay.

If your business has recurring billing or subscription-style payments, the thinking behind dunning overlaps with card-failure recovery. This guide on involuntary churn prevention is helpful because it shows how structured reminder logic can recover revenue without creating unnecessary customer friction.

The mistake that makes reminders useless

Many SMEs wait too long to start. They stay polite for too long because they don't want to upset the customer, then jump straight from silence to frustration.

That gap hurts you twice. The customer learns your terms are flexible, and your team loses time chasing debt that should have been addressed much earlier. A reminder process works best when it feels routine, not personal.

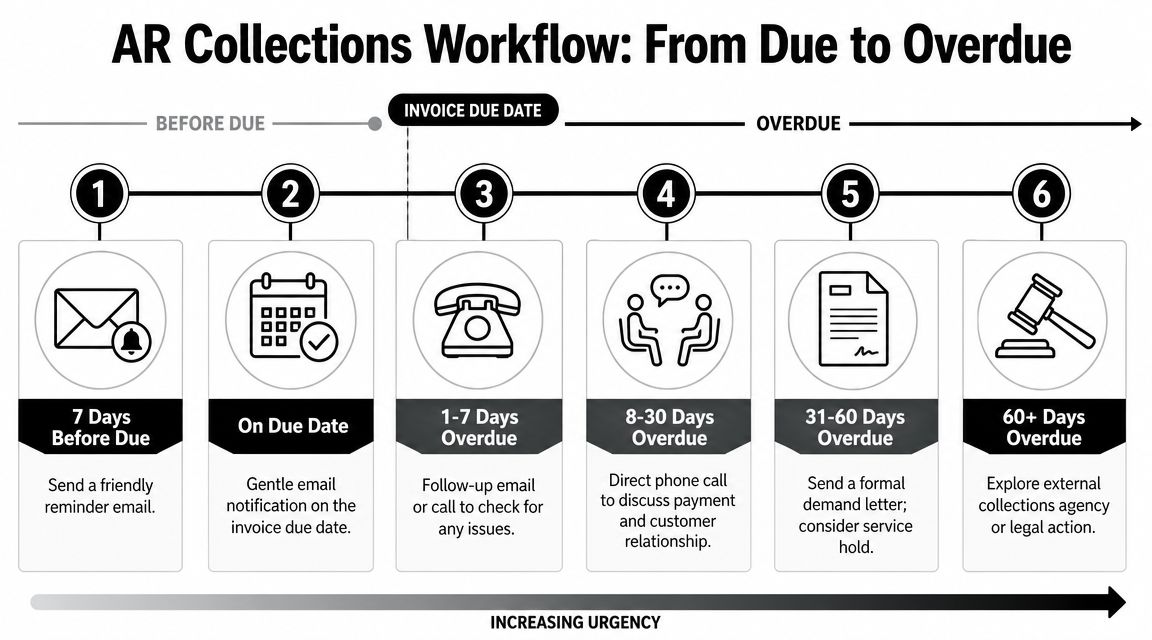

Execute a Smart Collections and Dispute Workflow

Once an invoice is overdue, you need a workflow, not good intentions. The whole point of collections is to make decisions in the right order, with the right level of effort, based on the value and risk of the debt.

Australian AR teams that perform well usually work from an ageing-led model. That means they start with clean invoice data, begin reminders before due date, escalate as soon as invoices become overdue, and segment follow-up by ageing bucket, as outlined in this AR collections workflow guide.

Use your ageing report as a work queue

Your ageing report should drive action every week. In tighter cash cycles, it should be reviewed more often.

A practical model:

Age bucket | Primary action | Who owns it |

|---|---|---|

Current | Confirm invoice received and approved | Automation or AR officer |

1 to 30 days overdue | Email plus follow-up call if needed | AR officer |

31 to 60 days overdue | Direct phone call, payment plan discussion, possible service hold | Finance lead or owner |

61 to 90 days overdue | Formal demand, senior escalation, review of ongoing exposure | Management |

90+ days overdue | Decide on agency, legal pathway, or write-off | Management with adviser input |

Teams often waste effort on the wrong debtors, spending time chasing easy low-value balances while larger, riskier accounts keep ageing.

Handle disputes fast or they become hiding places

Not every overdue invoice is a collections problem. Some are operational failures wearing a finance label.

Typical examples:

the PO number is missing

the customer says the wrong entity was invoiced

a quantity or rate doesn't match the quote

the work was approved verbally but not documented

the customer claims they never received the invoice

Each dispute needs an owner and a deadline. If nobody owns it, it sits in limbo while the debtor ages and the relationship gets murkier.

Log every touchpoint, every promise to pay, and every dispute note. If it isn't recorded, your team will repeat work and lose leverage.

Decide based on economics, not emotion

Many SMEs bleed time when they treat every invoice as equally worth chasing. It isn't.

The core decision is not “can we collect this?” It's “is the recovery effort worth more than the expected cash outcome?”

Use this lens:

Automate low-risk, low-value invoices where a reminder sequence usually does the job.

Personally chase invoices that are material, strategically important, or tied to ongoing work.

Escalate externally when internal follow-up is stalling and the balance justifies fees and management time.

Write off debts where staff time, management distraction, and third-party cost are likely to exceed recovery.

A collections call should also sound commercial, not emotional. Keep it simple:

“I'm calling about invoice [number], which is overdue. I want to confirm whether payment is scheduled, or whether there's an issue we need to resolve today.”

That phrasing does two things. It asks for a date, and it flushes out disputes quickly.

The biggest mistake is treating write-offs like defeat. Sometimes writing off a small, stale balance is the most disciplined financial decision available. The bad move is spending more to chase it than you'll recover.

Choosing Your Accounts Receivable Tech Stack

Most SMEs don't need enterprise software. They do need a system that matches their transaction volume, team capacity, and complexity.

The right tech stack for accounts receivable management depends on where the bottleneck sits. For some businesses, Xero or MYOB features are enough. For others, those platforms handle the ledger but not the workflow.

Start with what your accounting platform already does

Before buying another app, tighten the core system.

If you use Xero, MYOB, or QuickBooks, check whether you're already using:

Automated invoice sending

Recurring invoice templates

Statement generation

Basic payment reminders

Bank feed reconciliation

Customer contact accuracy

Many SMEs underuse the tools they already pay for. They've bought software but kept spreadsheet habits.

Know when built-in features stop being enough

You've outgrown basic accounting-platform receivables when:

overdue follow-up depends on one person's memory

disputes live in email threads

collectors can't see notes in one place

payment promises aren't tracked

customer segmentation is impossible

reporting doesn't show where action is stuck

That's the point where dedicated AR tools start earning their keep.

What dedicated AR platforms add

Products like EzyCollect, Upflow, and Chaser sit on top of your accounting system and manage the workflow around collection.

They usually help with:

Reminder logic: Different sequences by customer type or ageing bucket.

Shared visibility: Notes, promises, disputes, and follow-up history in one place.

Payment portals: Fewer excuses, easier customer action.

Collector prioritisation: Staff work the most important accounts first.

Reporting: Better visibility into ageing, follow-up activity, and collection bottlenecks.

Here's the practical distinction:

Tool category | Best for | Limitation |

|---|---|---|

Accounting software only | Lower-volume, simple receivables | Weak workflow control |

Add-on payment apps | Faster payment acceptance | Doesn't solve collections process |

Dedicated AR automation | Growing teams with overdue complexity | Extra setup and change management |

If you're mapping both sides of working capital at once, this guide to accounts payable automation in Australia is useful because AR and AP process quality usually rise or fall together.

Buy for process fit, not feature envy

The best stack is the one your team will use every week.

Check for:

clean integration with your ledger

clear audit trails

easy note logging

customer-level workflows

practical reporting for ageing and follow-up

support for your actual invoicing and payment process

If the tool is powerful but nobody updates it, you've just created a more expensive spreadsheet.

Measure Success with Key AR Metrics and SOPs

If AR performance only gets discussed when cash is tight, you're managing symptoms. The discipline comes from tracking a small set of metrics and documenting the routine so results don't depend on one person remembering what to do.

Australia's collections environment already tells you why this matters. The ATO's debt book remains a major macro signal that collections capacity is under strain, with total collectable debt reported in the tens of billions of dollars, as noted in this analysis of receivables management economics. For SMEs, the practical lesson is simple. A “better” collections process still fails if the labour cost of follow-up outweighs the likely recovery.

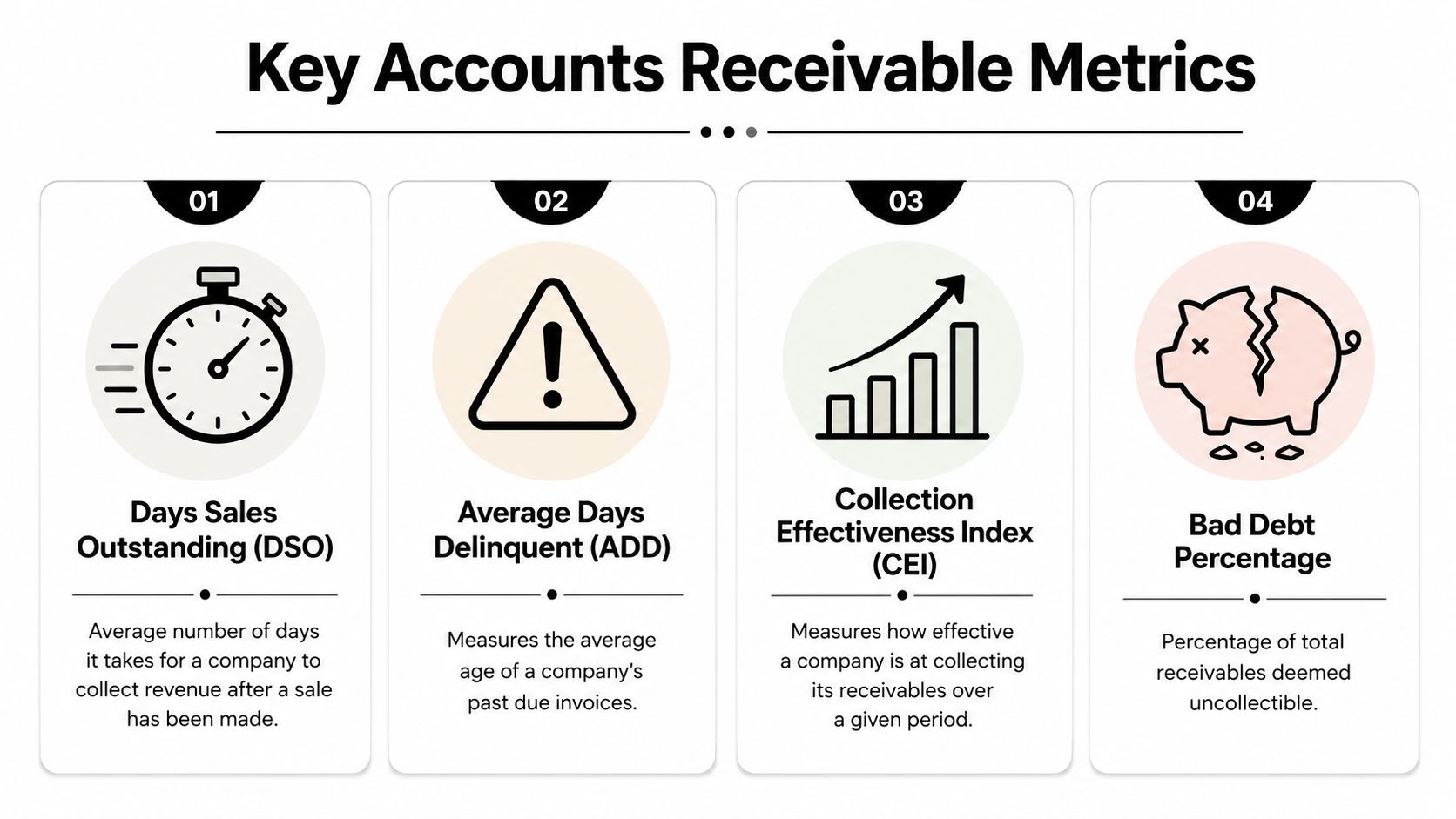

Track the metrics that change behaviour

You don't need a sprawling dashboard. You need metrics that tell you whether cash is moving and whether your team is using time well.

Days Sales Outstanding

Formula:

DSO = (Accounts Receivable ÷ Total Net Credit Sales) × Number of Days

This shows how long it takes, on average, to convert credit sales into cash. Use it as a trend metric, not a vanity metric. If it rises, inspect invoice timing, dispute volume, and overdue follow-up quality.

Average Days Delinquent

Formula:

ADD = DSO - Best Possible DSO

This isolates the overdue portion more clearly. If DSO is stable but ADD worsens, your issue may be concentrated in late accounts rather than broad billing delay.

Collection Effectiveness Index

Formula:

CEI = [(Beginning AR + Monthly Credit Sales - Ending Total AR) ÷ (Beginning AR + Monthly Credit Sales - Ending Current AR)] × 100

This is useful because it focuses on collection effectiveness within the period, rather than being distorted by fresh sales.

Bad debt percentage

Formula:

Bad Debt Percentage = Write-offs ÷ Total Receivables or Credit Sales

Track it consistently using one method. The exact benchmark matters less than whether it is improving, and whether write-offs are strategic or neglected debt aging into failure.

Good AR reporting doesn't just show what is overdue. It shows where your team is spending effort and whether that effort is worth the cash recovered.

Sample AR ageing report

Use a report structure your team can review quickly in a weekly meeting.

Customer | Invoice # | Total Due | Current (Not Yet Due) | 1-30 Days Overdue | 31-60 Days Overdue | 61-90 Days Overdue | 90+ Days Overdue |

|---|---|---|---|---|---|---|---|

Customer A | INV-001 | $ | $ | ||||

Customer B | INV-002 | $ | $ | ||||

Customer C | INV-003 | $ | $ | ||||

Customer D | INV-004 | $ | $ | ||||

Customer E | INV-005 | $ | $ |

This report becomes powerful when paired with action notes. Without next steps, it's just a list.

Turn the process into an SOP

A proper SOP keeps collections from becoming personality-driven. It also protects you when staff change.

A basic AR SOP should define:

Invoice timing: When invoices must be raised after delivery or milestone completion.

Reminder schedule: What goes out before due date, on due date, and after.

Escalation path: Who handles each ageing bucket.

Dispute handling: Who owns investigation and required response time.

Stop-supply rules: When ongoing work pauses.

Write-off approval: Who can approve and at what threshold.

Weekly review cadence: Which balances are reviewed and by whom.

Pair that with a regular management review. If you're building more disciplined reporting rhythms across the business, this article on the quarterly business review is a useful next step.

The businesses that get paid well usually do ordinary things consistently. They issue clean invoices, review ageing weekly, escalate early, resolve disputes quickly, and stop throwing expensive labour at low-value debt.

That's what mature accounts receivable management looks like. Not louder chasing. Better economics.

If your business is profitable on paper but cash still feels tight, Nexist helps Australian founders fix the mechanics behind it. That includes receivables, forecasting, SOPs, reporting, and the day-to-day finance systems that put real cash in the bank instead of leaving it trapped in operations.

accounts receivable management, cash flow management, sme finance australia, invoice management, debt collection

" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="dSFdkJotL" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="wscNJE44G" transform="translate(0 0.129)" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="sTpjGo1tb" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="s7ffpmKOD" transform="translate(0 0.129)" width="24px"/><g d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.000006px" id="D0ecaHEcW" transform="translate(0 0)" width="24px"><path d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z" fill="rgb(55, 184, 218)" height="24.000006px" id="IPLFE6zXx" width="24px"/><path d="M 4.02 0 L 0 0 L 0 12.092 L 4.02 12.092 Z" fill="rgb(255, 255, 255)" height="12.09201px" id="FWhtzAyuY" transform="translate(2.863 8.375)" width="4.02px"/><path d="M 2.274 0 C 0.899 0 0 0.904 0 2.089 C 0 3.25 0.871 4.179 2.221 4.179 L 2.247 4.179 C 3.648 4.179 4.521 3.25 4.521 2.089 C 4.495 0.904 3.649 0 2.274 0 Z" fill="rgb(255, 255, 255)" height="4.17876px" id="VmOsKv4kO" transform="translate(2.625 2.545)" width="4.52095px"/><path d="M 7.641 0 C 5.509 0 4.554 1.173 4.019 1.996 L 4.019 0.284 L 0 0.284 C 0.053 1.419 0 12.376 0 12.376 L 4.019 12.376 L 4.019 5.623 C 4.019 5.262 4.045 4.9 4.151 4.642 C 4.442 3.92 5.103 3.172 6.214 3.172 C 7.667 3.172 8.25 4.282 8.25 5.907 L 8.25 12.376 L 12.269 12.376 L 12.269 5.442 C 12.269 1.728 10.286 0 7.641 0 Z" fill="rgb(255, 255, 255)" height="12.37626px" id="n1XUbhaq0" transform="translate(9.105 8.09)" width="12.268830000000001px"/></g></g></g></g></svg>)