Free Cash Flow Forecast Template for SMEs: Master Your Cash

Download our free cash flow forecast template & guide for Australian SMEs. Predict shortages & take control of your cash.

Ansh Malhotra

Sales are up. The invoice list looks healthy. Then payroll is due on Thursday, a supplier wants payment before the next order ships, and your bank balance says something completely different from your profit report.

That gap is where most SME stress lives.

A proper cash flow forecast template fixes that. Not because a spreadsheet is magic, but because it forces timing into the conversation. It shows when cash lands, when it leaves, and where the pressure points sit before they become emergencies. For Australian owners juggling BAS, super, rent, wages, stock buys and slow-paying customers, that visibility matters more than a tidy P&L.

If you want a second practical reference alongside this guide, Comfi's SME cash flow playbook is a useful companion read.

Table of Contents

Beyond Guesswork Your Businesss Financial Future

A founder checks the bank account before 7 am, does rough maths in their head, and tries to decide which payment can wait without causing damage. That's common in growing businesses. It happens in ecommerce brands carrying too much stock, trade businesses waiting on debtor receipts, and agencies with solid revenue on paper but weak cash timing.

The core problem usually isn't effort. It's that profit and cash aren't the same thing. You can book a strong month, issue invoices, and still be short because customers haven't paid yet, stock had to be bought early, or tax and supplier payments hit in the same week.

Australian government guidance treats a cash flow forecast as a planning tool, not an admin exercise. Business.gov.au's cash flow guidance says a forecast should be built from estimated figures for each future period and used to identify payment cycles, seasonal trends, shortages and surpluses so a business can plan ahead to cover payments.

That's the right lens. A cash flow forecast template isn't there to impress your accountant. It's there to answer operational questions fast.

What owners are really trying to solve

Most owners don't need more reports. They need clarity on a short list of decisions:

Payroll confidence: Can wages clear without scrambling?

Supplier timing: Should you place the next stock order now or stagger it?

Tax readiness: Is BAS covered when it falls due?

Growth discipline: Can you afford another hire, vehicle, or software stack this quarter?

Practical rule: If your numbers don't show timing, they won't help you manage cash.

A good template turns vague stress into visible trade-offs. It shows the week or month where the bank balance tightens. It shows whether the issue is slow collections, front-loaded stock purchases, debt repayments, or recurring overhead that has crept too high.

For many owners, this is the moment finance stops being rear-view reporting and starts becoming management. That's also why strategic planning matters. If you want the broader operating context behind the numbers, this article on strategic and financial planning is worth reading.

What changes once you use the forecast properly

The forecast doesn't remove uncertainty. It removes guesswork.

Instead of saying “we should be okay”, you can see the likely closing balance, the timing of major receipts, and the periods where a delay from one customer could create pressure. That changes how owners negotiate terms, schedule purchases, chase debtors and decide when to grow.

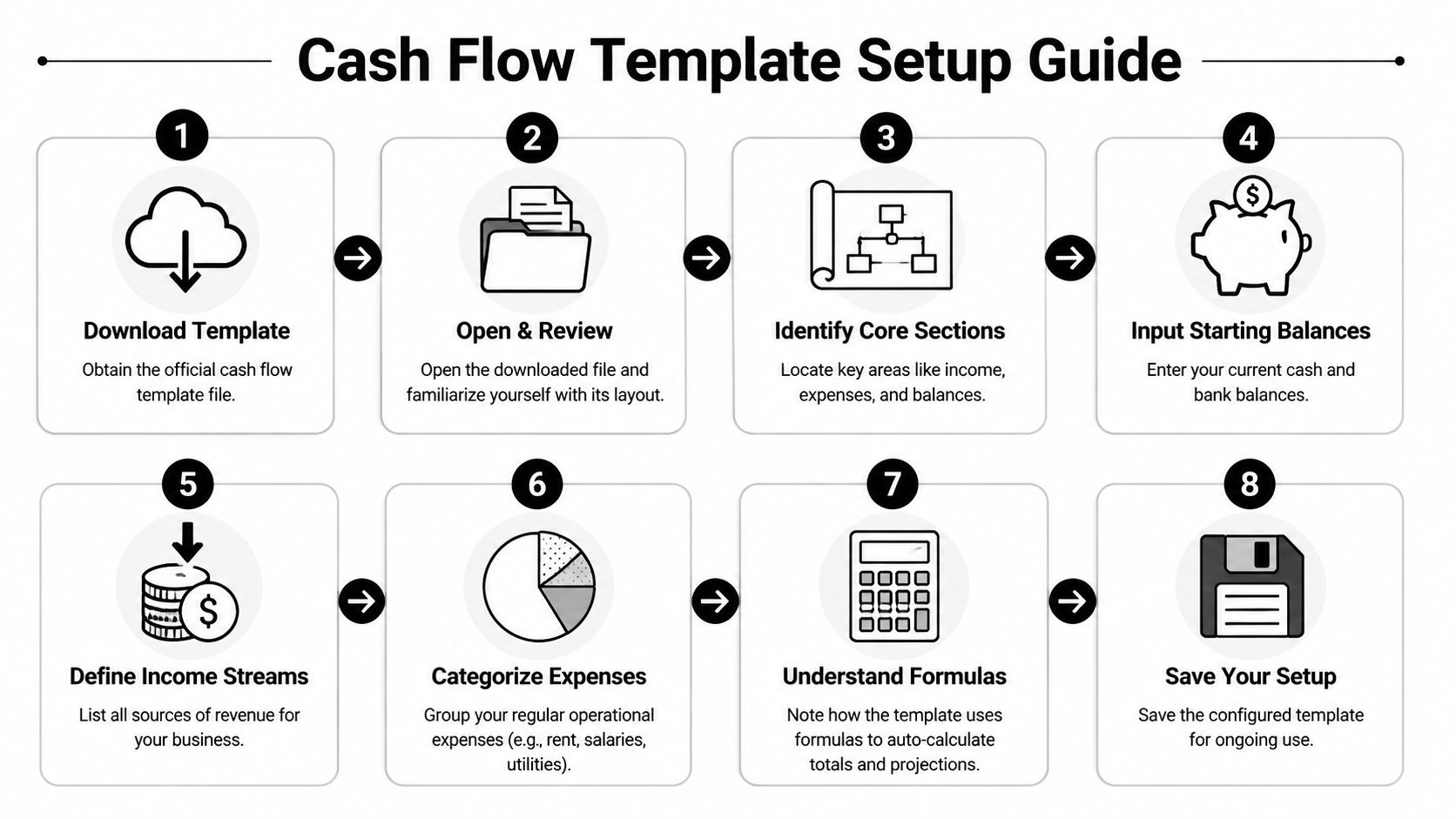

Your Cash Flow Template Setup Guide

The fastest way to make a cash flow forecast template useless is to overcomplicate it on day one. Start with a structure you'll actually maintain. The point is clarity, not clever formulas.

A solid template usually separates revenue, expenses and net cash flow with a manageable number of line items. Guidance aligned with common SME practice shows revenue sections typically contain 3 to 6 items and expenditure sections often contain 10 to 20 line items, which keeps the model detailed enough to be useful without turning it into a mess. The same guidance also reflects the move to dynamic spreadsheets that update figures automatically as you type, rather than manual bookkeeping sheets, as noted in this cash flow forecast template guide.

Start with the right forecast rhythm

For most Australian SMEs, a weekly view works best when cash is tight or moving quickly. A monthly view is fine for broader planning if collections and payments are stable.

Use one sheet for the forecast period and one for assumptions. Don't mix raw assumptions, historical notes and forecast outputs in the same block. That's how templates become fragile.

Before you touch formulas, define:

Forecast frequency

Weekly for short-term control. Monthly for easier medium-term review.Forecast horizon

Enough periods ahead to spot a cash dip before it arrives.Update routine

Pick one day each week to refresh actuals, move opening balances forward and adjust assumptions.

A video walkthrough can help if you want to see the mechanics in action.

Build the four core sections properly

Every practical cash flow forecast template should include these core sections.

Section | What goes in it | Why it matters |

|---|---|---|

Opening balance | Cash at bank at the start of the period | This anchors reality |

Cash inflows | Receipts from customers and other cash coming in | This shows actual incoming cash, not sales booked |

Cash outflows | Wages, rent, suppliers, tax, debt, software, equipment and other payments | This reveals pressure points |

Closing balance | Opening balance plus inflows minus outflows | This tells you whether the period is workable |

Use plain labels. “Customer receipts” is better than “operating income”. “Supplier payments” is better than “cost of sales accruals”. Owners should be able to scan the sheet and understand it in seconds.

Keep the template usable

Australian businesses often miss cash issues because line items are too vague or timing is wrong. Keep categories practical:

Customer receipts: Cash received in the period, not invoices issued.

Creditor payments: Cash paid to suppliers when settlement is expected.

BAS: GST and related tax outflows when they're due.

Superannuation: Employer contributions based on payment timing, not just payroll dates.

Debt repayments: Loan and finance repayments separated from normal operating costs.

Clean templates drive better decisions. Busy templates get ignored.

A few setup rules make a big difference:

Use separate rows for irregular costs: Annual insurance, licence renewals, big repairs and one-off subscriptions should never be buried in “other”.

Carry balances forward automatically: The closing balance of one period should feed the next opening balance.

Mark assumptions clearly: If a figure is estimated, label it so you can test it later.

Avoid false precision: Round where needed. The template is for management, not tax lodgement.

If the template isn't helping you answer “Can we pay everything on time?”, it needs simplifying.

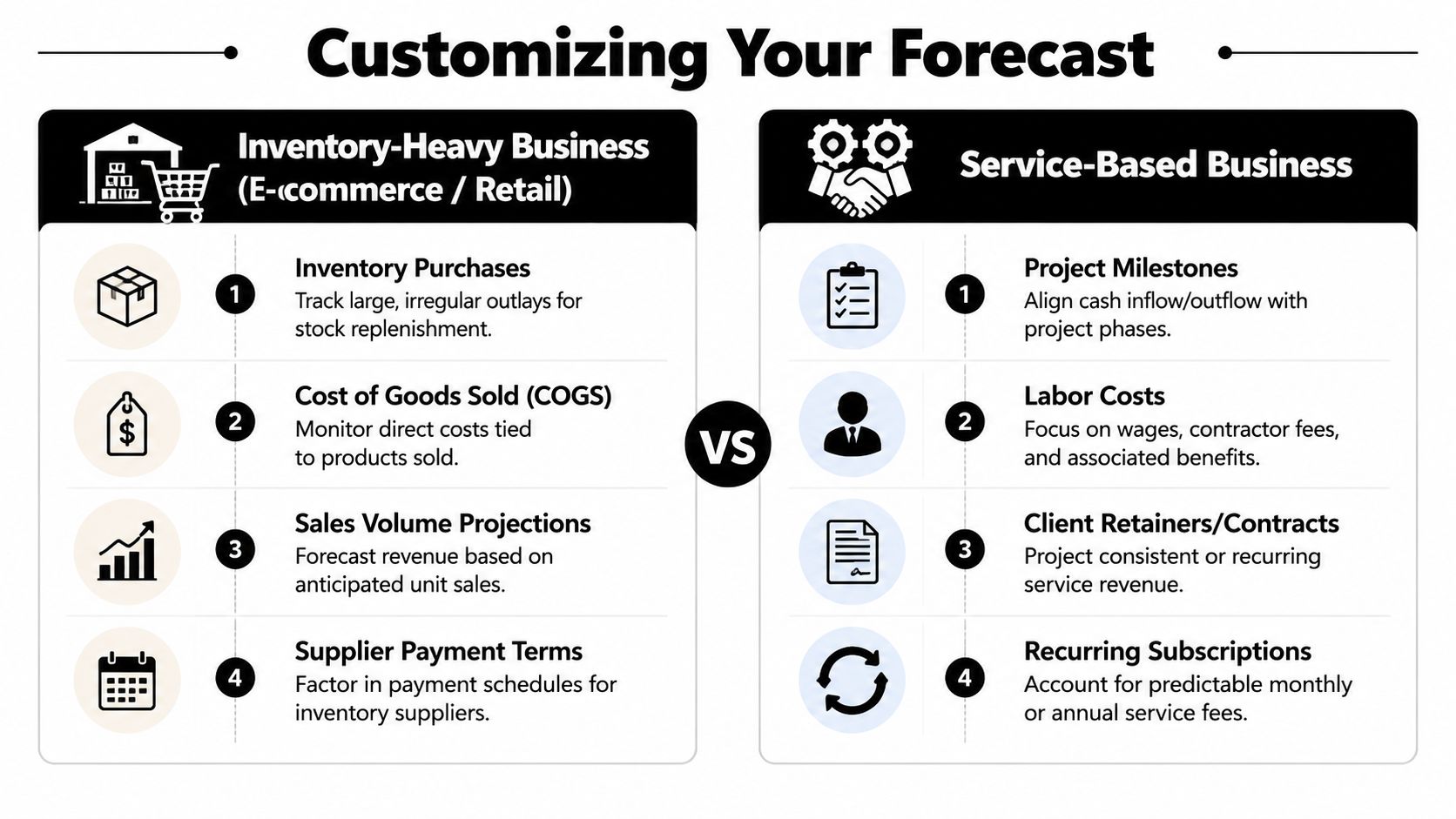

Customising the Forecast for Your Business Model

The same spreadsheet structure won't behave the same way in every business. A retail wholesaler and a design agency can both show the same monthly revenue and still have very different cash risk.

Most generic templates miss the main issue. They treat forecasting as simple inflow minus outflow maths and fail to model working-capital shocks. NAB's guidance points owners toward seasonality, one-off events and payment cycles, yet many templates still don't show how to reveal low-cash periods before they happen in stock-heavy or credit-based businesses, as outlined in NAB's cash forecast template guidance.

Inventory-heavy businesses

If you run ecommerce, retail, wholesale or manufacturing, the forecast has to show where cash gets trapped before a sale converts back into banked money.

Your template should include line items such as:

Stock purchases

Freight and landed costs

Supplier deposits

Customs or import-related cash outflows

Marketplace or merchant fee timing

Inventory build for seasonal peaks

The key mistake is forecasting stock purchases as a flat monthly amount. That rarely reflects reality. Stock is usually bought in lumpy cycles. Cash goes out well before the related receipts come in.

A practical setup might look like this:

Forecast area | What to model |

|---|---|

Sales period | When demand is expected to lift or slow |

Purchasing lead time | When stock must be ordered to support those sales |

Supplier terms | Whether payment is upfront, partial, or on terms |

Landed timing | When freight and related costs actually hit cash |

If you're planning equipment as part of growth, timing matters there too. This guide to financial planning for equipment acquisition is useful because it frames new assets as a cash commitment problem, not just a purchase decision.

A strong inventory forecast also separates fixed overhead from costs that rise with volume. If that distinction needs work, this article on fixed vs variable costs helps clean up the logic.

Stock doesn't just consume cash when it arrives. It often starts draining cash when you commit to buy it.

Service and trade businesses

Service firms have a different trap. They can look cash-light even with high margins because receipts lag delivery.

For agencies, consultancies, trades and project-based businesses, customise the forecast around:

Deposits

Progress claims or milestone invoices

Retainers

Final payments

Subcontractor costs

Payroll and contractor timing

Software and project delivery tools

Don't forecast income from the date work is booked. Forecast it from when cash is expected to hit the account. If you invoice at month-end on standard terms, that receipt may not appear until the next period. For trade businesses, progress claims and retention arrangements can create the same issue.

A clean service forecast usually tracks two things side by side:

work scheduled or invoiced

cash expected from that work

That split matters because “earned” and “received” are not interchangeable in a cash model.

One template two very different risks

Inventory-heavy businesses usually get squeezed by stock timing. Service businesses usually get squeezed by debtor timing.

The template should reflect that difference. Use the same overall framework, but change the line items and assumptions to suit the actual way cash moves in your business. Otherwise the sheet looks professional while hiding the true risk.

Using Your Forecast for Scenario Planning

A static forecast is only half-finished. Its full value comes when you test what happens if conditions change.

Build three versions not one

Keep one base file, then duplicate it into three scenarios:

Baseline

Optimistic

Pessimistic

The baseline should reflect what's most likely based on current trading, existing customer behaviour and known commitments. The optimistic version should show what happens if collections improve, sales land earlier, or a planned opportunity converts cleanly. The pessimistic version should assume pressure, not disaster.

Stress doesn't usually arrive as one dramatic event; it shows up through delayed receipts, tighter supplier behaviour, lower conversion, or a cost that hits earlier than expected.

If one late payment breaks the forecast, the business doesn't have a revenue problem. It has a timing problem.

What to change in each scenario

Use the same structure across all three versions so comparisons stay clean. Then adjust assumptions, not formulas.

For an optimistic case, you might change:

customer receipts arriving closer to expected dates

a new client or stronger sales period landing on time

discretionary spending staying controlled

For the baseline case, keep:

normal payment patterns

current staffing levels

expected recurring expenses

known tax and debt commitments

For the pessimistic case, test:

slower customer collections

delayed project starts

earlier stock purchases

a supplier asking for faster payment

a large annual or irregular outgoing landing in the same period as weaker receipts

Expert benchmarks show that a collection rate stress test simulating a 30-day payment delay from top customers reveals immediate liquidity breaches in 45% of Australian SMEs with inventory-heavy operations. That's why pessimistic scenario planning isn't excessive. It's practical risk management.

One useful method is to keep a short assumptions table at the top of the sheet.

Assumption area | Baseline | Optimistic | Pessimistic |

|---|---|---|---|

Customer payment timing | Normal behaviour | Faster collections | Delayed collections |

Sales conversion | Current trend | Stronger close rate | Weaker close rate |

Supplier timing | Existing terms | Stable terms | Earlier cash outflow |

Irregular costs | As scheduled | Unchanged | Hits sooner or costs more |

The point isn't to predict the future perfectly. It's to know which levers you can pull early. If the pessimistic case shows a weak closing balance, you can respond before the cash pinch arrives by tightening collections, moving purchases, pausing discretionary spend, or renegotiating timing.

Finding and Plugging Hidden Cash Leaks

A good forecast doesn't just predict balances. It exposes where cash keeps slipping away.

Where the leaks usually sit

The first leak is often supplier timing. Technical analysis shows 52% of Australian SMEs report unplanned cash shortfalls due to timing mismatches in supplier payments. A stronger template fixes that by mapping outflows by expected settlement date rather than invoice date.

The second leak sits in receivables drift. Cash collections start trailing invoiced work, but the owner only notices once the bank tightens. The forecast should make that gap visible period by period.

A third leak is non-operating cash outflows that are real but easy to underweight. Debt repayments, BAS, asset purchases and annual costs can all make an otherwise healthy month look broken.

What the forecast should make obvious

Review the template like a diagnostic tool, not a bookkeeping record.

Look for widening gaps: If sales or invoicing look fine but customer receipts stay soft, debtor timing is weakening.

Scan recurring outflows: If overhead rows are consistently heavy, the issue may be cost structure rather than revenue.

Check payment clustering: If suppliers, tax and wages bunch into the same period, the template should show a visible dip.

Separate operating and non-operating items: Otherwise debt and tax obligations disappear inside general expenses.

If you want a sharper lens on timing between buying, selling and collecting, this guide to the cash conversion cycle is directly relevant.

The biggest cash leaks are rarely hidden by complexity. They're hidden by bad timing assumptions.

When owners start using the forecast this way, they stop asking “Why are we always tight?” and start asking better questions. Which customer group pays slowly? Which supplier terms create pressure? Which costs are fixed but no longer justified? That's where control starts.

From Forecasting to Full Financial Control

A spreadsheet is a strong starting point. It's not the finish line.

Where spreadsheets start to break

Manual forecasts work well when the business is still simple enough for one person to update confidently. They struggle once transaction volume grows, stock cycles get messy, project billing varies, or multiple people touch the numbers.

That's when owners start seeing familiar symptoms:

the sheet is technically correct but already out of date

assumptions live in someone's head instead of the model

actuals and forecast don't reconcile cleanly

no one trusts the result enough to make decisions quickly

For venue and hospitality operators, this issue gets even sharper because margins, labour and timing move constantly. If you want a category-specific finance example, this guide to restaurant P&L statements is a useful reminder that reporting only matters when it helps operators act.

What better control looks like

The next level is to connect your forecast to live financial data from systems such as Xero or MYOB, then monitor a short list of operating KPIs alongside it. Cash runway, debtor days, stock pressure, creditor timing and recurring overhead all become easier to manage when the data refreshes regularly and the assumptions are visible.

That shift changes the role of finance. Instead of chasing yesterday's numbers, you use current numbers to decide:

whether to hire now or wait

how much stock to commit to

when to push collections harder

whether pricing needs attention

when to speak to the bank before pressure builds

A virtual CFO becomes valuable at this point because the job isn't building a prettier spreadsheet. It's translating the forecast into action, trade-offs and operating discipline. That includes pressure-testing assumptions, setting reporting cadence, tightening working capital, and helping owners make decisions before cash gets tight.

A cash flow forecast template is where most businesses should start. Full financial control begins when that forecast becomes part of how the business is run every week.

If you want help turning a spreadsheet into a working cash management system, Nexist offers practical support for Australian SMEs that need clearer forecasting, tighter working capital and better decision-making. Start with the Nexist Business Scorecard to get a clearer view of where cash is leaking and what to fix first.

cash flow forecast template, cash flow management, sme finance australia, virtual cfo, business forecasting

" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="dSFdkJotL" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="wscNJE44G" transform="translate(0 0.129)" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="sTpjGo1tb" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="s7ffpmKOD" transform="translate(0 0.129)" width="24px"/><g d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.000006px" id="D0ecaHEcW" transform="translate(0 0)" width="24px"><path d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z" fill="rgb(55, 184, 218)" height="24.000006px" id="IPLFE6zXx" width="24px"/><path d="M 4.02 0 L 0 0 L 0 12.092 L 4.02 12.092 Z" fill="rgb(255, 255, 255)" height="12.09201px" id="FWhtzAyuY" transform="translate(2.863 8.375)" width="4.02px"/><path d="M 2.274 0 C 0.899 0 0 0.904 0 2.089 C 0 3.25 0.871 4.179 2.221 4.179 L 2.247 4.179 C 3.648 4.179 4.521 3.25 4.521 2.089 C 4.495 0.904 3.649 0 2.274 0 Z" fill="rgb(255, 255, 255)" height="4.17876px" id="VmOsKv4kO" transform="translate(2.625 2.545)" width="4.52095px"/><path d="M 7.641 0 C 5.509 0 4.554 1.173 4.019 1.996 L 4.019 0.284 L 0 0.284 C 0.053 1.419 0 12.376 0 12.376 L 4.019 12.376 L 4.019 5.623 C 4.019 5.262 4.045 4.9 4.151 4.642 C 4.442 3.92 5.103 3.172 6.214 3.172 C 7.667 3.172 8.25 4.282 8.25 5.907 L 8.25 12.376 L 12.269 12.376 L 12.269 5.442 C 12.269 1.728 10.286 0 7.641 0 Z" fill="rgb(255, 255, 255)" height="12.37626px" id="n1XUbhaq0" transform="translate(9.105 8.09)" width="12.268830000000001px"/></g></g></g></g></svg>)