Optimize Profit: Inventory Valuation Methods for 2026

Choose the right inventory valuation methods (FIFO, Weighted Average) for your Australian business. Understand their impact on profit, tax, and cashflow in

Ansh Malhotra

Sales are up. The bank balance is tight. Your warehouse is full, but it doesn't feel like you're holding wealth. It feels like you're holding stress.

That's where most founders start asking better questions about stock. Why does profit look healthy while cash is under pressure? Why did gross margin shift when pricing barely moved? Why does the year-end result feel different from what the ops team saw month to month?

A lot of inventory advice stops at definitions. It tells you what FIFO means and how weighted average works, then leaves out the part founders care about most. How your inventory value changes cash flow, BAS, and year-end profit. That gap matters for Australian SMEs because inventory is a major working-capital bucket, especially in retail, ecommerce, wholesale, and manufacturing, and cost volatility in materials and freight makes the choice more than academic, as noted in this inventory valuation overview.

If you sell on fast-moving channels, the pressure gets sharper. Founders trying to protect margin on social commerce often need a cleaner handle on COGS before they can price confidently. That's why guides like HiveHQ's TikTok Shop profit advice are useful alongside proper valuation discipline. And if you need finance leadership around these decisions rather than basic bookkeeping, a virtual CFO model usually gives you the missing layer between numbers and action.

Table of Contents

Why Your Inventory Value Is More Than Just a Number

The founder problem behind the stock number

A founder looks at the dashboard and sees three different stories.

Sales look fine. The P&L says margin is acceptable. The bank account says something's off.

That disconnect often sits inside inventory. Stock isn't just an asset sitting on the balance sheet. It's cash you already spent, profit you may or may not have earned yet, and a number that directly changes what appears in cost of goods sold.

When purchase prices move around, the method behind that inventory number starts shaping the story. Two businesses can buy the same products, sell the same units, and still report different gross profit depending on how they assign cost to those sales.

Practical rule: If you don't trust your stock value, you can't trust your gross margin.

Where the pressure actually shows up

For most Australian SMEs, the consequences show up in places founders feel immediately:

Cash flow pressure because too much money is tied up in slow-moving or overvalued stock

Tax timing because reported profit changes when COGS changes

BAS and management reporting friction when internal numbers don't line up cleanly with year-end treatment

Pricing mistakes because the team uses stale or smoothed costs without realising it

This is why inventory valuation methods matter so much in practice. They aren't only for accountants closing out the year. They shape how you judge product margin, reorder timing, and whether a sales spike helped the business.

Founders usually don't need a textbook. They need clarity on one question. Which method gives the cleanest, most usable view of the business you run?

A simple example using one product

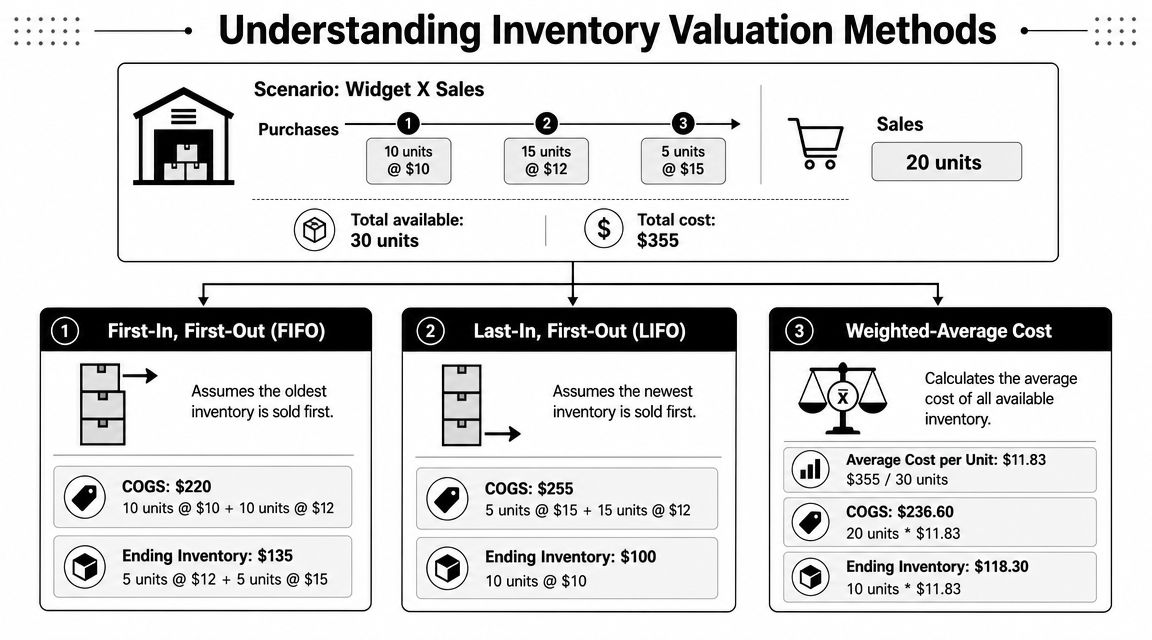

Use one product and one month of buying activity.

You purchase:

10 units at $10

15 units at $12

5 units at $15

That gives you 30 units with a total cost of $355.

You then sell 20 units.

The sales activity is the same under every method. What changes is which cost gets assigned to the 20 units sold, and which cost remains in ending stock.

How FIFO works

FIFO means first-in, first-out. The oldest purchase costs move into COGS first.

In the example, the 20 units sold would be costed as:

10 units at $10

10 units at $12

So:

COGS = $220

Ending inventory = $135

That ending inventory is made up of:

5 units at $12

5 units at $15

FIFO is easy to understand because it often lines up with physical flow. Older stock gets sold first. For food, cosmetics, seasonal products, and many retail lines, that logic makes operational sense too.

In a rising-cost environment, FIFO usually pushes older, lower costs into COGS first. That can make gross profit look stronger in the short term, because current sales are matched against earlier purchase costs.

How weighted-average cost works

Weighted-average cost blends all purchase costs into one average unit cost.

Using the same example:

Total cost = $355

Total units = 30

Average cost per unit = $11.83

That means:

COGS = $236.60

Ending inventory = $118.30

Weighted average is popular when goods are homogeneous and you don't practically separate one batch from another. Think bulk items, standard components, or fast-moving stock where the finance team wants cleaner month-to-month KPI tracking.

Weighted average tends to reduce the noise created by fluctuating supplier prices. That makes management reporting steadier, even when purchasing conditions aren't.

The trade-off is that it can smooth reality too much if you need exact visibility into how recent cost increases are affecting current margin.

Here's a useful explainer if you want a walkthrough in video form:

Where specific identification fits

Specific identification tracks the actual cost of the exact item sold.

This works when each unit is unique or high value. Examples include:

vehicles

custom machinery

fine jewellery

artwork

one-off configured equipment

If you sell a specific unit, you assign that specific unit's cost. It gives the cleanest matching between cost and sale price, but only when your systems can track each item properly. For most ecommerce brands, retailers, and wholesalers with repeat SKUs, it's too heavy.

What LIFO is and why Australian businesses can't use it for statutory reporting

LIFO means last-in, first-out. The newest costs go into COGS first.

In the example:

5 units at $15

15 units at $12

So:

COGS = $255

Ending inventory = $100

LIFO matters mainly because founders read overseas content and assume it's an option everywhere. It isn't. For Australian entities reporting under AASB and IFRS-aligned rules, FIFO and weighted average are permitted cost formulas, but LIFO is not permitted, as outlined in this summary of inventory valuation methods under AASB-aligned reporting.

That matters because Australian businesses can't use LIFO as a way to push recent cost inflation through COGS for statutory reporting. If margins are under pressure, the answer has to come from purchasing discipline, pricing, stock turn, and better visibility at SKU level.

Comparing the Methods Side by Side

What changes when costs are rising

When supplier prices climb, your valuation method changes three things founders watch closely. COGS, reported profit, and the value left in stock.

FIFO usually leaves newer costs in ending inventory. Weighted average blends the effect. Specific identification depends on the exact item sold.

That means the choice isn't just about compliance. It changes how profitable the business appears, how stable your KPIs look month to month, and how much confidence you can place in product margin reporting.

A method that looks good in the accounts can still be a poor management tool if it hides what's happening at SKU level.

Inventory Valuation Method Comparison

Metric | First-In, First-Out (FIFO) | Weighted-Average Cost (WAC) | Specific Identification |

|---|---|---|---|

COGS during rising costs | Usually lower earlier, because older costs move into COGS first | Smoothed, because costs are blended across units | Depends on the actual unit sold |

Ending inventory value | Often closer to recent replacement cost because newer layers remain in stock | Sits between older and newer purchase layers due to averaging | Reflects the exact unsold items on hand |

Reported gross profit | Often appears stronger during inflationary periods | More stable and less volatile across reporting periods | Can vary sharply based on the exact mix sold |

Tax impact | Higher reported profit can mean more taxable profit sooner | Usually moderates swings in taxable profit | Depends on the actual cost attached to each item sold |

Operational simplicity | Straightforward if physical flow matches cost flow | Often simplest for homogeneous goods and fast-moving standard SKUs | Operationally demanding because every item must be tracked individually |

Best fit | Retail, perishables, import-heavy businesses wanting stock closer to current landed cost | Wholesale, manufacturing inputs, bulk or standardised goods | Cars, art, custom equipment, high-value serialized items |

What often goes wrong | Founders like the stronger margin but miss the risk of overconfidence on pricing | Teams use the average cost and overlook fast-moving recent cost increases | Businesses try to use it without disciplined serial or batch tracking |

One practical point matters more than the method labels. Your accounting method has to support decision-making, not just year-end compliance.

If your team prices off blended costs but buys in volatile landed-cost cycles, weighted average may keep reports calm while hiding pressure in newer purchase batches. If you use FIFO for imported goods, the balance sheet may look more current, but month-end profit can look better than the cash reality feels.

Navigating Australian Accounting Rules and Tax

A founder orders heavily before Christmas, freight spikes, demand softens in January, and the stock room is still full in March. On paper, inventory still looks healthy. In the accounts, that number may already be too high.

What AASB 102 means in practice

Under AASB 102, Australian businesses measure inventory at the lower of cost and net realisable value, and the permitted cost formulas include FIFO and weighted average. LIFO is not permitted.

For an SME, the practical question is simple. Can you still sell that stock for enough to recover its recorded cost after completion, freight, discounts, and selling costs? If not, the value comes down and the hit runs through profit.

That matters because inventory is not just a balance sheet line. It affects borrowing capacity, tax timing, dividend decisions, and how much confidence you can place in your margin.

Why NRV catches founders late

Net realisable value, or NRV, usually becomes a problem after operations have already made the mistake. The common pattern is overbuying, slow sell-through, margin pressure, then discounting. Finance records the consequence at month-end or year-end, but the cash pain started earlier when money was tied up in stock that was not moving.

FIFO can increase that risk in a rising-cost environment. The closing stock can include newer, higher-cost purchases. If market pricing falls or clearance activity starts, those higher-cost units may no longer be recoverable at full value. The write-down then reduces profit in the period you recognise it, even though the buying decision happened months earlier.

For founders, impact shows up in three places:

Reported profit drops when the write-down is booked

Working capital tightens because stock no longer supports the same asset value

Banking or investor discussions get harder if earnings and current assets weaken at the same time

I see this most often in import-heavy businesses, seasonal retail, and product businesses carrying too much range depth. The accounting adjustment is the last step. The commercial issue is that cash sat in the wrong inventory for too long.

What consistency means for tax and reporting

Method choice matters for tax timing, but the bigger issue for many Australian SMEs is whether reported profit tracks the cash reality closely enough to support decisions.

As discussed earlier, AASB requires consistency. You cannot swap methods casually to improve a result in one period, then switch back later. If the stock system uses one logic, management reports use another, and the year-end file applies manual overrides on top, gross margin becomes hard to trust. Once that happens, purchasing, pricing, and cash planning all suffer.

The trade-off is practical. A method that produces cleaner month-to-month reporting may still delay visibility on cost pressure. A method that keeps closing stock closer to recent cost may lift profit in some periods and bring forward taxable income. Neither outcome is automatically right or wrong. The right choice is the one your systems can apply consistently and your leadership team can use to make better buying and pricing decisions.

That is why inventory policy should sit inside strategic and financial planning for Australian SMEs, not just inside the year-end compliance file.

A workable review routine usually includes:

Inventory ageing by SKU, category, or batch

Landed cost tracking where freight, duty, or FX moves change true margin

Regular NRV reviews for seasonal, damaged, obsolete, or discount-prone items

Clear write-down rules so issues are recognised early, not parked until year-end

Founders do not need a textbook answer here. They need numbers they can trust. If your inventory method overstates margin, delays write-downs, or hides cost pressure, it will show up in cash before it shows up in the accounts.

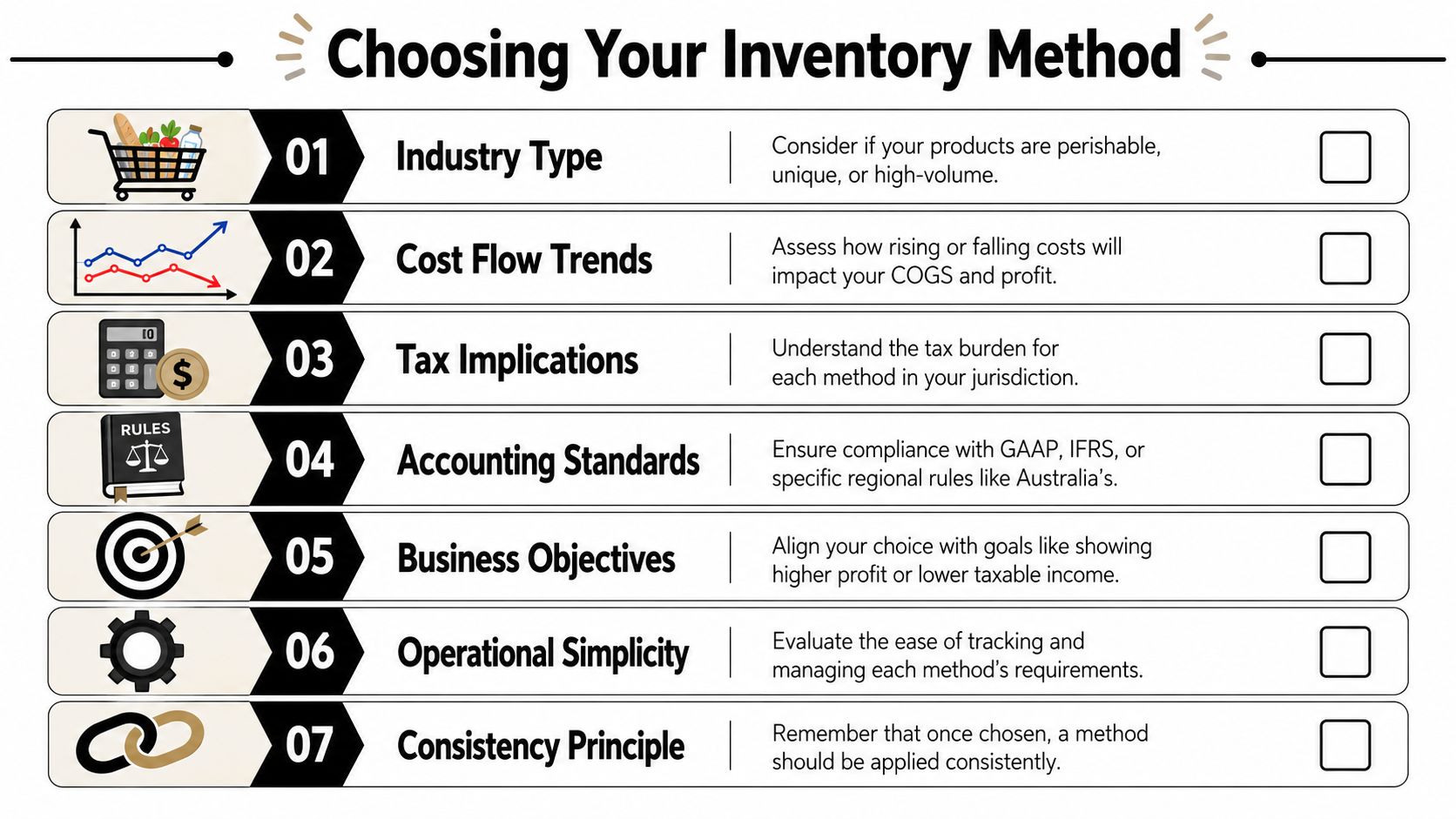

How to Choose the Right Method for Your Business

A founder buys a container of stock at one cost, the next container lands higher because freight and FX moved, and the month still looks profitable on paper. Then BAS, supplier payments, and the next reorder hit at once. The inventory method you choose affects how quickly those cost increases show up in COGS, how much profit you report, and how much tax you may pay before the cash is in the bank.

The right method is the one that matches how stock moves, how your system records cost, and what the leadership team needs to see each month. Under AASB, the choice also has a practical tax effect because reported profit changes with inventory values. For Australian SMEs, that makes this a cash flow decision as much as an accounting one.

Retail and ecommerce

Retail and ecommerce businesses usually care about three things. Margin visibility, reorder timing, and cash tied up in stock.

Weighted average often suits businesses with repeat SKUs, frequent purchasing, and little operational value in tracking individual cost layers. It smooths gross margin when supplier prices move around. That makes monthly reporting easier to read. The trade-off is slower visibility on rising replacement cost, so pricing decisions can lag if import costs are climbing fast.

FIFO often suits businesses that physically sell older stock first or need closing stock values closer to recent landed cost. In a rising-cost environment, FIFO usually pushes older, lower costs into COGS first. Reported profit can look stronger in the short term. So can the tax bill. That is useful if the numbers reflect real pricing power. It is dangerous if the business is under-recovering current replacement cost.

If you are setting growth targets or reviewing margin by channel, link the inventory method back to your strategic and financial planning for Australian SMEs. Inventory policy should support pricing, purchasing, and cash planning, not sit off to the side as a finance-only choice.

Manufacturing and wholesale

Manufacturers and wholesalers need a method management can practically use.

Weighted average usually works better when raw materials are interchangeable and purchase prices move often. It produces a steadier gross margin line, which helps when the team reviews monthly performance, tenders, and production efficiency. The downside is that it can blur sudden input cost spikes. If resin, steel, timber, or imported components jump in cost, the margin pressure may appear later than the purchasing team needs.

FIFO usually works better when batch timing matters, stock rotates in a predictable order, or recent landed cost is important for quoting and replenishment. It can give a sharper read on what current stock would cost to replace. But founders should go in with open eyes. In periods of rising cost, FIFO can lift accounting profit and bring taxable income forward even while cash is getting tighter.

A simple test helps here. If higher reported profit would make you feel better, but your next stock order would still strain cash, do not choose a method based on optics.

High-value unique items

Specific identification is required when each item has its own cost base and that difference matters.

That applies to businesses selling custom machinery, vehicles, project-based inventory, specialist equipment, and other serial-tracked items. One unit may include extra freight, imported parts, or custom labour that another unit does not. Averaging those costs produces weak job margin data and poor pricing decisions. In these businesses, the key question is whether your systems and warehouse discipline are good enough to track each item properly. If they are not, start there.

Physical control matters more than many founders expect. Teams that improve scanning, serial tracking, and stock movement accuracy usually get better cost data as a result. For practical ideas, see optimizing asset management for operations.

A decision framework founders can use

Use these questions to narrow the choice:

Are the items interchangeable or materially different?

Interchangeable items usually point to weighted average or FIFO. Distinct items point to specific identification.How fast do input costs move, and how quickly do you need that pressure to show up in margin?

If you need an earlier signal, FIFO often gives a clearer read than weighted average.Does physical stock flow match the cost flow?

If the warehouse rotates older stock first, FIFO may fit. If stock is pooled and picked without regard to purchase batch, weighted average is often easier to run cleanly.What matters more right now: stable monthly reporting or faster visibility on replacement cost?

Weighted average usually helps with stability. FIFO usually helps with current cost visibility.Could a higher inventory value increase reported profit before the cash benefit is real?

If yes, test the tax impact before locking in the method.Can your software and team apply the method consistently every week?

A theoretically better method is a poor choice if it creates manual fixes, reconciliation delays, or margin numbers no one trusts.

A good choice is usually boring. It fits the operation, holds up under AASB, and gives founders a margin number they can use to price stock, plan cash, and avoid paying tax too early on profit that has not turned into cash yet.

Implementation and Day-to-Day Inventory Control

Set the method in software, then match the real-world process

Once you've chosen a method, set it properly in your accounting stack and inventory tools. For many SMEs that means configuring the logic inside Xero, MYOB, Cin7, DEAR Inventory, Unleashed, or a connected ERP, then checking that the stock system and finance file are treating cost the same way.

Many businesses commonly encounter issues here. The software says FIFO, but the warehouse picks whatever pallet is easiest. Or the inventory app tracks landed cost one way while the accounting file journals stock adjustments another way. The result is bad margin reporting and slow reconciliations.

If your business also manages equipment, scanners, warehouse hardware, or distributed stock-handling assets, it helps to borrow ideas from broader operational control. This guide to optimizing asset management for operations is useful because inventory accuracy often improves when physical handling discipline improves too.

The controls that stop cash leaks

Software won't save a weak process. Daily and monthly controls matter more than the initial setup.

The minimum operating rhythm should include:

Regular stocktakes so the books reflect physical reality

Cycle counts on high-value, high-volume, or high-risk SKUs

Ageing reviews so old stock doesn't sit at full value indefinitely

Landed-cost checks when freight, duty, or supplier pricing moves

Reconciliation between platforms if ecommerce channels, inventory software, and accounting systems all touch stock

A lot of ecommerce businesses also need tighter rules around returns, bundles, kits, and channel-specific SKUs. If that's your world, practical guidance on ecommerce inventory management helps close the gap between what the platform says you sold and what the accounts say it cost.

The strongest inventory process is boring. It's consistent, timely, and easy to audit. That's what protects cash. That's what makes margin reporting usable. And that's what stops year-end surprises from building undetected through the year.

If inventory is tying up cash, distorting profit, or making your reporting hard to trust, Nexist can help you get control of it. We work with Australian founders to tighten stock processes, improve margin visibility, and turn the finance function into a practical tool for better decisions.

inventory valuation methods, fifo vs weighted average, inventory accounting, cost of goods sold, australian accounting standards

" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="dSFdkJotL" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="wscNJE44G" transform="translate(0 0.129)" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="sTpjGo1tb" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="s7ffpmKOD" transform="translate(0 0.129)" width="24px"/><g d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.000006px" id="D0ecaHEcW" transform="translate(0 0)" width="24px"><path d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z" fill="rgb(55, 184, 218)" height="24.000006px" id="IPLFE6zXx" width="24px"/><path d="M 4.02 0 L 0 0 L 0 12.092 L 4.02 12.092 Z" fill="rgb(255, 255, 255)" height="12.09201px" id="FWhtzAyuY" transform="translate(2.863 8.375)" width="4.02px"/><path d="M 2.274 0 C 0.899 0 0 0.904 0 2.089 C 0 3.25 0.871 4.179 2.221 4.179 L 2.247 4.179 C 3.648 4.179 4.521 3.25 4.521 2.089 C 4.495 0.904 3.649 0 2.274 0 Z" fill="rgb(255, 255, 255)" height="4.17876px" id="VmOsKv4kO" transform="translate(2.625 2.545)" width="4.52095px"/><path d="M 7.641 0 C 5.509 0 4.554 1.173 4.019 1.996 L 4.019 0.284 L 0 0.284 C 0.053 1.419 0 12.376 0 12.376 L 4.019 12.376 L 4.019 5.623 C 4.019 5.262 4.045 4.9 4.151 4.642 C 4.442 3.92 5.103 3.172 6.214 3.172 C 7.667 3.172 8.25 4.282 8.25 5.907 L 8.25 12.376 L 12.269 12.376 L 12.269 5.442 C 12.269 1.728 10.286 0 7.641 0 Z" fill="rgb(255, 255, 255)" height="12.37626px" id="n1XUbhaq0" transform="translate(9.105 8.09)" width="12.268830000000001px"/></g></g></g></g></svg>)