Key Person Risk: Protect Your Business Future

What is key person risk & its impact? Quantify financial damage & implement strategies to protect your SME's future.

Ansh Malhotra

You already know where this shows up.

The founder who still approves every supplier payment. The sales lead who carries the top accounts in their mobile. The operations manager who knows exactly how stock is reordered, but nowhere has it written down. The bookkeeper who can get payroll out on time because they alone know which workarounds keep the system moving.

If one of those people is suddenly unavailable for a few months, the problem isn't abstract. Cash collection slows. Orders get missed. Clients get nervous. Margins slip because someone else is guessing their way through pricing, purchasing, or fulfilment.

That's key person risk. And in most Australian SMEs, it has less to do with insurance brochures than with operational dependence. If the business can't function smoothly without one individual, you don't have a people issue alone. You have a cash flow issue, a systems issue, and often a value issue.

Table of Contents

The Bus Factor and Your Business Value

Take a simple scenario. Your top salesperson can't work for three months. They hold the trust with your biggest clients, they know which customers pay late, they know what pricing concessions were made, and they're the person your team leans on when a deal starts drifting.

If they disappear, revenue rarely stops in one dramatic moment. It leaks out through slower follow-up, weaker renewals, delayed quotes, softer negotiation, and clients who suddenly feel less certain about staying. That's why founders should think about key person risk through the lens of the bus factor. How many people could be “hit by a bus” before the business stalls?

In Australia, this isn't rare. A survey cited in insurer guidance found that 71% of small businesses were dependent on one or two key individuals for their success, yet only 22% had key person life insurance in place according to Nationwide's summary of key person risk data.

That gap matters, but not just because of insurance. It matters because most founders underestimate how much of the business still runs through one person's habits, judgment, and memory.

What founders usually miss

A key person isn't always the owner. It can be the estimator who prices jobs accurately, the warehouse lead who spots stock issues before they turn into write-offs, or the finance manager who knows exactly how to chase debtors without damaging relationships.

When that person goes missing, the first signs often show up in the same places covered by strong business performance indicators. Cash conversion gets worse. Gross margin becomes inconsistent. Lead times blow out. Team confidence drops because no one is sure who owns what.

Practical rule: If one person's absence would force you into daily firefighting, you already have key person risk.

Why this affects value, not just operations

Buyers, lenders, and investors don't separate “operations risk” from “business value” as neatly as owners do. If revenue depends on one relationship-holder, or if service quality depends on one specialist, the business is less stable. Less stability means more risk. More risk affects confidence in future cash flow.

That's why the bus factor is more than a thought exercise. It's a fast way to test whether your business is built on systems or personalities. If the answer is personalities, the fix isn't motivational. It's operational.

Identifying Your Key People It Is Not Just the CEO

Most founders start with the obvious answer. “I'm the key person.” Sometimes that's true. Often it's incomplete.

The sharper question is this. Whose absence would interrupt cash flow, delivery, compliance, or customer retention within days, not months? That's how you find concentration points.

In many Australian SMEs, the highest-risk roles sit below the executive layer. The issue is rarely title. It's dependency.

Start with four pressure points

Review your business across these areas:

Sales and relationships

Look for the person who holds client trust, renewal history, pricing judgment, or referral networks. If customers buy because they trust that one person, the role is critical.Operations and fulfilment

This is often the scheduler, warehouse lead, production manager, or ops coordinator who keeps work moving. If they go missing and the team can't maintain service levels, they're a key person.Finance and cash control

Some businesses rely on one person for payroll, creditor timing, debtor follow-up, BAS prep, lender reporting, or approval flows. If that knowledge is trapped with one individual, the business is exposed.Technology and systems

For Australian IT and service businesses, key person exits can trigger downtime and security vulnerabilities because system knowledge is often held by only a few ageing specialists, directly linking this concentration to valuation loss, as noted by AdventOne's discussion of key man risk in IT environments.

Ask better diagnostic questions

Don't ask, “Who is important?” Everyone in a good team is important.

Ask questions that reveal dependency:

Who makes decisions no one else can confidently make?

Whose relationships would be difficult to transfer quickly?

Who knows a process that isn't documented anywhere?

Who can log into or administer a critical system that others can't access?

Who regularly solves exceptions rather than following a standard process?

If this person took unexpected leave tomorrow, what would stop first?

The person doing the workaround is often the key person, not the person with the senior title.

Separate inconvenience from real risk

Not every hard-to-replace employee creates key person risk. Some departures are painful but manageable. Others create immediate operating stress.

A useful distinction looks like this:

Situation | Usually difficult but manageable | Usually true key person risk |

|---|---|---|

Knowledge | Others know most of the role | Knowledge sits mainly with one person |

Relationships | Clients deal with a team | Clients rely on one individual |

Systems access | Shared access and handover exist | One person controls access or settings |

Decision-making | Rules and approvals are clear | Decisions rely on personal judgment |

Recovery path | A backup can step in quickly | Replacement requires rebuilding from scratch |

Don't forget hidden specialists

The key person in a growth-stage business is often someone the owner doesn't initially name.

It might be the ecommerce manager who understands channel margins and stock reorder logic. It might be the freight coordinator who knows the exceptions that keep delivery promises realistic. It might be the long-serving administrator who owns the rhythm of invoicing, payroll, and supplier communication.

Founders usually find these people by following friction. Where does work slow down when someone is away? Where does the team say, “We'll wait until they're back”? That's where your concentration risk sits.

How to Quantify Key Person Risk in Dollars

Most owners know key person risk is bad. That isn't enough. If you want action, you need to convert concern into numbers.

There are two financial views that matter. The first is the direct operating hit if a critical person disappears. The second is the effect on business value if an outsider sees that dependency and prices the risk accordingly.

William Buck notes that a key person discount typically ranges from 10% to 25% of enterprise value, while private businesses can face much larger implied discounts depending on the level of dependence, as explained in William Buck's analysis of key person risk and valuation.

The operating view

Start with what breaks in the first few weeks. Don't try to build a perfect model. Build a useful one.

Focus on five cost buckets:

Lost gross profit from reduced sales, delayed projects, or weaker retention

Replacement cost for recruiting, onboarding, and temporary support

Rework and error cost when someone else handles tasks badly or slowly

Working capital strain from slower invoicing, debtor collection, or stock mistakes

Owner time diversion when the founder gets dragged back into low-value operational rescue

The point isn't precision to the dollar. The point is to make the commercial impact visible enough that the business stops treating this as a soft issue.

A simple calculator you can use

Build a worksheet for any role you believe is critical.

Impact Area | Estimated Monthly Cost ($) | Duration (Months) | Total Impact ($) |

|---|---|---|---|

Lost gross profit | |||

Temporary replacement support | |||

Recruitment and onboarding | |||

Project or delivery delays | |||

Debtor collection slowdown | |||

Inventory or purchasing errors | |||

Founder time pulled into operations | |||

Customer churn or account instability |

Fill this in role by role. Sales lead. Operations manager. Finance manager. System admin. You'll usually find one or two roles create far more downside than the rest.

What to estimate if you don't have clean data

If your reporting is still rough, use observed business behaviour.

For example, ask:

Revenue exposure

Which customers or channels are tied closely to this person?Margin exposure

Does this person make pricing, stock, rostering, or purchasing decisions that protect margin?Timing exposure

How quickly would the absence hit invoicing, collections, order flow, or service delivery?Dependency depth

Can someone competent step in with notes, or would they need to reverse-engineer the role?

This is also where turnover context helps. If you're already seeing role churn or team instability, you should model risk more conservatively. A practical primer for businesses tracking turnover can help sharpen how you think about role continuity and replacement pressure.

If you can't explain the monthly cash impact of losing a person, you probably haven't understood the role deeply enough.

The valuation view

Operational loss is only half the problem. The market also discounts businesses that are too person-dependent.

A founder often says, “We'd cope.” A buyer asks, “Why should I pay full value for a business that only works because one person still holds the engine together?” Those are different standards.

Use this lens:

If the business runs through one relationship-holder, expect value pressure.

If margins depend on one person's judgement rather than process, expect value pressure.

If systems access and key controls are concentrated, expect value pressure.

If the founder is still the default approval path, expect value pressure.

That's the commercial case for mitigation. You're not documenting SOPs and cross-training people to look organised. You're protecting cash flow now and preserving negotiating power later.

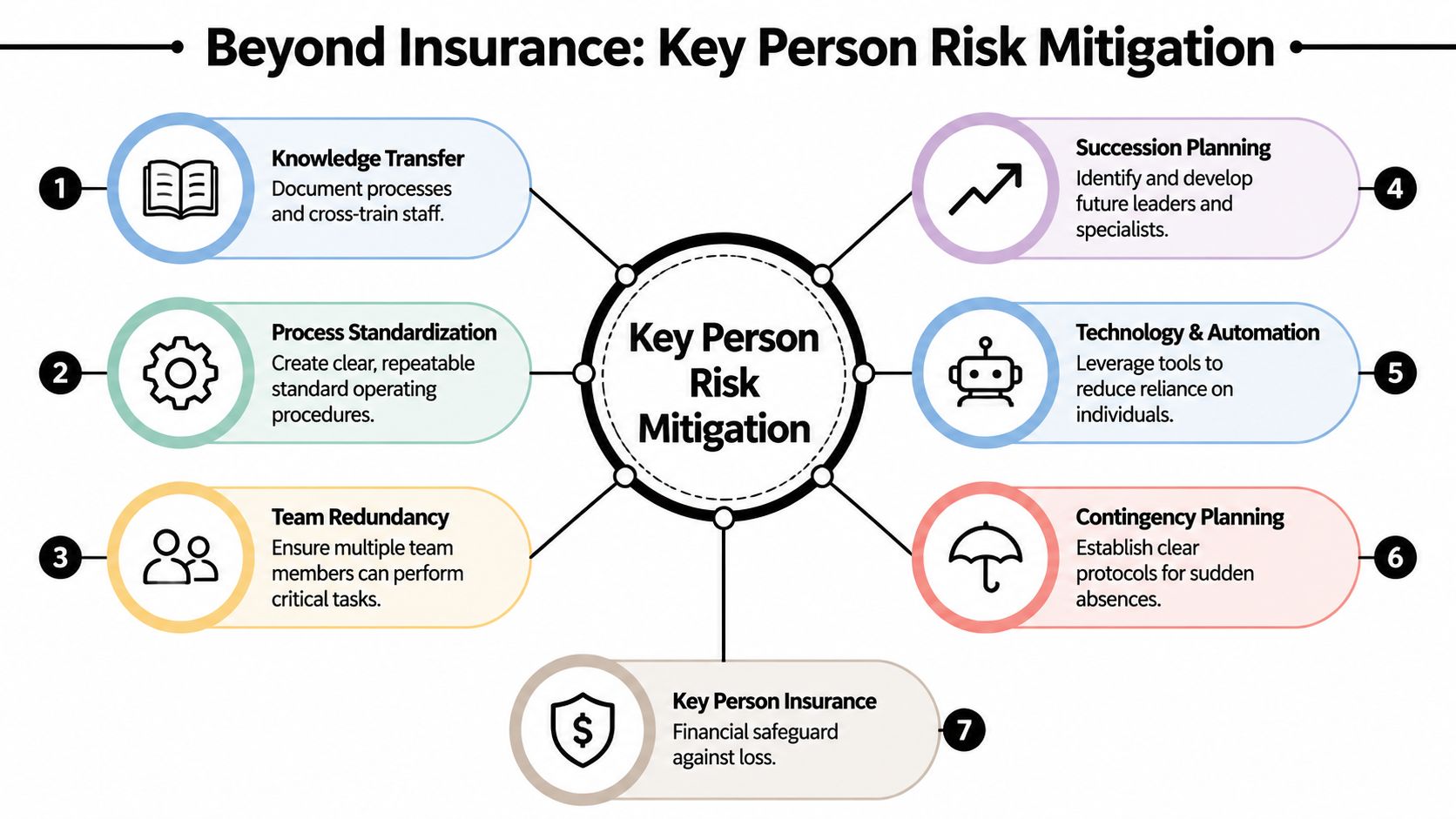

Mitigation Strategies Beyond Just Insurance

Insurance has a place. If a key person dies or becomes disabled, insurance can provide liquidity and breathing room.

But insurance doesn't log into Xero, approve supplier payments, handle debtor disputes, transfer customer trust, or explain why the stock reorder settings were changed last quarter. For most Australian SMEs, the bigger issue is operational dependence. A more useful response links exposure to measurable controls such as documented SOPs, delegated approvals, cross-training, and finance dashboards that show where the owner is the bottleneck, as discussed in this perspective on operational key-person exposure.

Knowledge transfer that actually works

Most businesses say they need documentation. Fewer build documentation that another person can use under pressure.

Good knowledge transfer has three parts:

Record the task

Explain the judgment behind the task

Prove someone else can do it

That last part is where most SOPs fail. A screen recording no one has tested isn't continuity.

Use practical formats:

Step-by-step SOPs for recurring tasks such as payroll, invoicing, purchasing, month-end close, stock ordering, customer onboarding

Decision rules for areas where judgment matters, such as discount limits, payment plans, reorder thresholds, or escalation triggers

Exception logs that capture the irregular problems a key person usually solves from memory

Cross-training without creating chaos

Cross-training often gets handled badly. Owners tell two people to “shadow each other” for a week, then assume the risk is solved.

It isn't.

Cross-training works when you assign a backup for a specific workflow, set a date for them to perform it, and review where they get stuck. If the backup still needs constant prompting, you don't have redundancy yet.

A stronger approach:

Nominate one primary backup for each critical process

Schedule live handovers where the backup completes the task

Rotate real responsibility occasionally so the process doesn't go stale

Review failure points immediately after the handover

Owner warning: If every exception still comes back to you, you haven't delegated. You've only redistributed admin.

A short explainer on managing insider risk effectively is useful here because role dependency and access dependency often travel together.

Systems that reduce dependence

The strongest businesses remove unnecessary heroics from day-to-day work. That usually means standardising the flow of decisions and making operational data visible.

Useful examples include:

Area | Fragile setup | More resilient setup |

|---|---|---|

Approvals | Founder approves everything | Clear delegated approval limits |

Cash flow | One person watches the bank balance | Shared dashboard for cash, debtors, creditors |

Inventory | Reorders happen from memory | Reorder rules and review cadence |

Invoicing | Invoices wait for one person | Trigger-based workflow with backup owner |

Client delivery | Account history sits in email threads | Shared CRM notes and handover records |

This is where automation earns its keep. Xero, approval workflows, recurring invoice rules, CRM task assignment, shared reporting, and stock alerts can remove dependence on memory and manual chasing. The benefit isn't novelty. It's consistency.

Here's a useful overview that complements those controls:

Succession planning for smaller businesses

Succession planning sounds corporate, so many founders ignore it. That's a mistake.

In an SME, succession planning can be simple:

Name the interim owner of each critical role

List the top five responsibilities that must continue if the person is absent

Document external contacts tied to the role

Set authority limits so backups know what they can decide

Review capability gaps and train deliberately

If the business has personal wealth structures, lending exposure, or family ownership considerations tied to the founder, it's also worth understanding how the business and personal side connect. Guidance from a private wealth advisor perspective can help owners think more clearly about continuity beyond day-to-day operations.

The businesses that handle key person risk best don't rely on a single fix. They combine documentation, role backup, process discipline, automation, and financial visibility. Insurance can support that system. It can't replace it.

The Digital Dimension of Key Person Risk

A lot of key person risk content still assumes the threat is mainly human capital. That's outdated.

For many Australian firms, the fragile point is the combination of person, process, and platform. One person knows the payroll password, the Xero admin settings, the lender portal, and the stock reorder rules. That creates a single point of digital failure, as described in Echelon Health's discussion of modern key person exposure.

The real question to ask

Don't ask only, “Who knows the system?”

Ask, “Can we still invoice, pay staff, access cash, and serve customers if that person is unavailable tomorrow?”

That question changes the conversation. It turns key person risk from an HR concern into an operational continuity issue.

Where digital dependency usually hides

In smaller businesses, digital concentration often sits in ordinary places:

Accounting access such as Xero admin permissions, bank feed setup, payroll settings

Banking and finance portals including lender logins, payment approvals, merchant facilities

Operations tools such as inventory software, shipping platforms, rostering apps, ecommerce back ends

Security recovery including password resets, MFA devices, and email admin access

If all of that sits with one employee or founder, a sudden absence can stop work immediately. The problem isn't just delay. It's confusion, access lockouts, and rushed workarounds that create fresh risk.

A business with good staff and poor access design is still fragile.

Build a digital continuity pack

A practical fix is to create a controlled digital emergency kit. Not a random spreadsheet of passwords. A governed access structure that another authorised person can use when needed.

Include:

System ownership register listing each critical platform and its owner

Admin and backup admin roles for finance, payroll, banking, operations, and cloud tools

Access instructions for handover, recovery, and emergency escalation

Approval map showing who can release payments, run payroll, or change key settings

Review rhythm so old access, old devices, and old assumptions don't linger

Role-based access matters here. So does discipline around shared visibility. The goal isn't to let everyone into everything. The goal is to ensure the business doesn't stop because one person took the keys home.

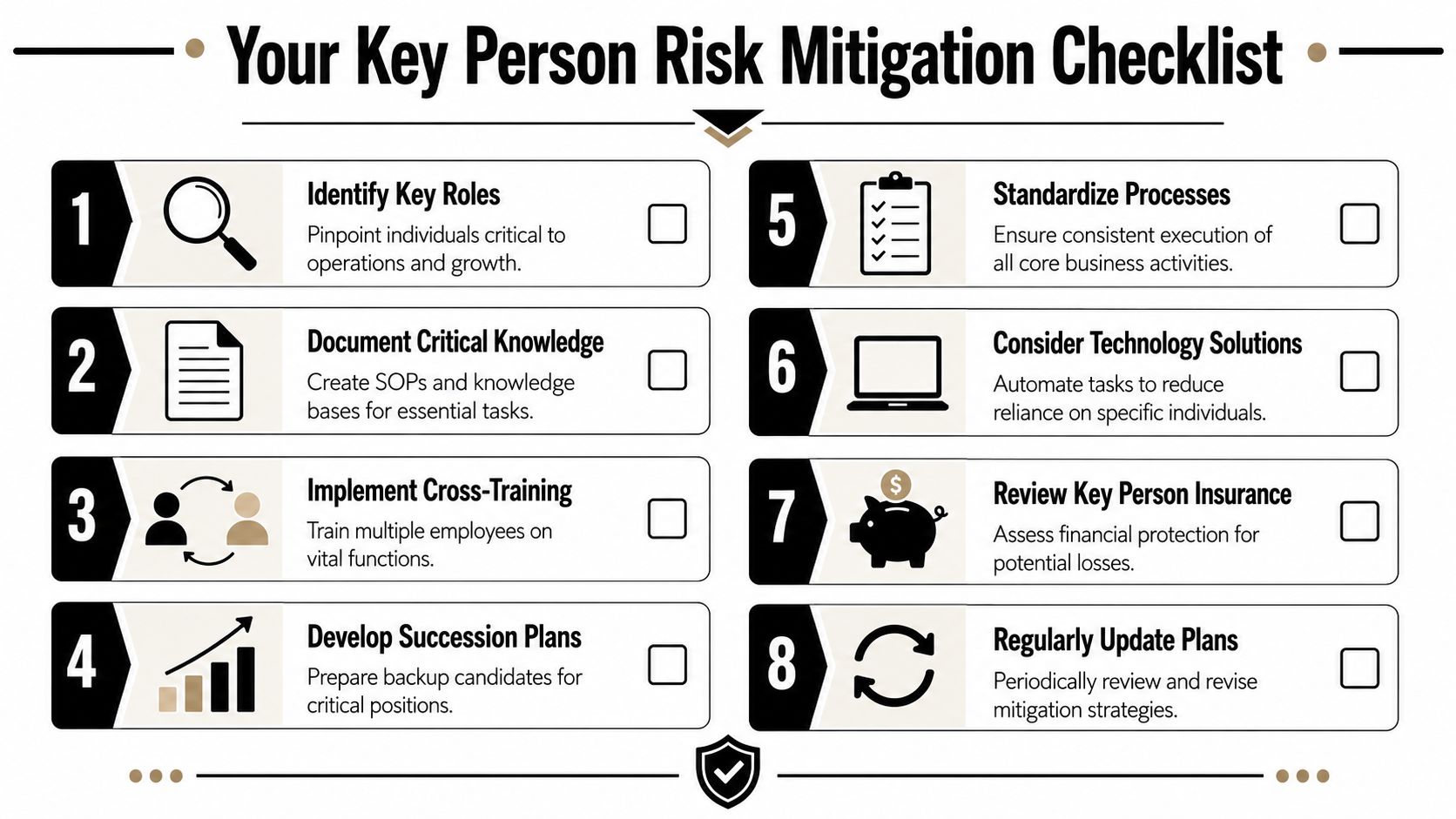

Your Key Person Risk Mitigation Checklist

Most businesses don't need a grand transformation to reduce key person risk. They need a disciplined starting point and a short list of actions that get done.

Use this checklist by timeframe. Keep it practical. If a task doesn't make the business easier to run without one individual, it probably isn't the priority.

This week

Start by exposing the obvious weak points.

List the roles that would disrupt cash flow fast

Don't overthink the org chart. Name the people whose absence would affect sales, collections, payroll, stock, delivery, or client retention.Map critical systems and approvals

Identify who controls bank access, Xero admin, payroll, lender portals, inventory settings, and customer communication.Choose one process to document immediately

Pick a live process such as payroll, invoicing, debtor follow-up, or stock ordering. Document it while the current owner performs it.

This month

Move from awareness to operating protection.

Assign backups for the highest-risk tasks

One named backup per process is better than vague shared ownership.Test the backup in real conditions

Let them run the task, not just observe it. Watch where they hesitate.Create a simple risk register

Track the role, what depends on it, what systems are involved, whether an SOP exists, and whether a backup has been tested.Review whether insurance fits your exposure

Insurance may help with financial shock, but only after you've identified what the actual business interruption would look like.

This quarter

Here, resilience starts to show up in daily performance.

Standardise recurring processes

Turn ad hoc routines into documented workflows with approval limits and clear ownership.Build shared visibility into the numbers

Use finance dashboards so cash, receivables, payables, margin pressure, and stock movement aren't trapped with one person.Tighten digital continuity

Review admin access, backup access, recovery methods, and who can operate essential platforms.Update founder dependency points

If the owner is still the default decision-maker for pricing, collections, stock, hiring, or supplier approval, redesign the flow.

The best time to fix key person risk is when the business is stable. Once the person is gone, you're paying for every missing process in real time.

If you want a useful benchmark, ask whether the business could keep operating for a sustained period without one critical person while still getting paid, paying staff, serving customers, and making timely decisions. If the answer is no, that's your next operating project.

A grounded view of leadership and advisory support can also help when founders are still too central to execution. Reading about Neha Malhotra's background and approach gives a sense of how finance-led operators think about turning owner dependency into scalable systems.

If key person risk is showing up in your cash flow, reporting, stock control, or day-to-day decision bottlenecks, Nexist can help you turn that dependence into documented process, clearer controls, and a business that keeps moving without constant founder intervention.

key person risk, business continuity, succession planning, risk management, sme finance

" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="dSFdkJotL" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="wscNJE44G" transform="translate(0 0.129)" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="sTpjGo1tb" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="s7ffpmKOD" transform="translate(0 0.129)" width="24px"/><g d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.000006px" id="D0ecaHEcW" transform="translate(0 0)" width="24px"><path d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z" fill="rgb(55, 184, 218)" height="24.000006px" id="IPLFE6zXx" width="24px"/><path d="M 4.02 0 L 0 0 L 0 12.092 L 4.02 12.092 Z" fill="rgb(255, 255, 255)" height="12.09201px" id="FWhtzAyuY" transform="translate(2.863 8.375)" width="4.02px"/><path d="M 2.274 0 C 0.899 0 0 0.904 0 2.089 C 0 3.25 0.871 4.179 2.221 4.179 L 2.247 4.179 C 3.648 4.179 4.521 3.25 4.521 2.089 C 4.495 0.904 3.649 0 2.274 0 Z" fill="rgb(255, 255, 255)" height="4.17876px" id="VmOsKv4kO" transform="translate(2.625 2.545)" width="4.52095px"/><path d="M 7.641 0 C 5.509 0 4.554 1.173 4.019 1.996 L 4.019 0.284 L 0 0.284 C 0.053 1.419 0 12.376 0 12.376 L 4.019 12.376 L 4.019 5.623 C 4.019 5.262 4.045 4.9 4.151 4.642 C 4.442 3.92 5.103 3.172 6.214 3.172 C 7.667 3.172 8.25 4.282 8.25 5.907 L 8.25 12.376 L 12.269 12.376 L 12.269 5.442 C 12.269 1.728 10.286 0 7.641 0 Z" fill="rgb(255, 255, 255)" height="12.37626px" id="n1XUbhaq0" transform="translate(9.105 8.09)" width="12.268830000000001px"/></g></g></g></g></svg>)