Virtual CFO Melbourne: A Founder's How-To Guide (2026)

Virtual cfo melbourne - Hiring a virtual CFO in Melbourne? Our guide covers costs, interview questions, KPIs & onboarding for SMEs. Find the right financial

Ansh Malhotra

You're probably feeling the contradiction already. Revenue is moving, the team is busy, customers are buying, but cash still feels tighter than it should. BAS deadlines creep up, payroll lands with a thud, stock sits longer than expected, and your reporting tells you what happened last month instead of what's about to hurt you next week.

That's where most founders start looking for a virtual cfo melbourne service. Not because they want corporate theatre. Because they want someone to stop the leaks, clean up the finance ops, and give them enough visibility to make decisions without living in spreadsheets.

A lot of firms talk about strategy. Fewer can trace the actual path from margin to cash. In practice, that path usually runs through receivables, inventory, pricing discipline, approvals, and reporting cadence. If those pieces are loose, growth gets expensive fast.

Table of Contents

Why Your Melbourne Business Needs an Operational Partner

Founders rarely wake up wanting a CFO. They wake up wanting fewer surprises.

The usual trigger isn't “we need more strategic insight”. It's more practical than that. Cash is leaving the business in ways that aren't obvious from the P&L. Customers pay too slowly. Stock is overbought. Purchase approvals are messy. Payroll and BAS create recurring stress because the timing is wrong, not necessarily because the business is unprofitable.

That's why the strongest virtual cfo melbourne engagements behave less like abstract advisory and more like an operational control layer. The work isn't only about board packs. It's about creating enough financial visibility to act before a small issue becomes a cash squeeze.

According to guidance on virtual CFO needs in Melbourne, most pages in this category focus on strategy and reporting, but rarely answer the founder's real question: when is cash leaking through inventory, receivables, or process bottlenecks? The same source notes that small businesses account for 97.2% of all businesses in Australia, and many are still managing finance tasks manually rather than through integrated systems.

Where the pain usually shows up

For most SMEs, the warning signs are operational before they look strategic:

Cash doesn't match profit: Sales look fine, but the bank balance says otherwise.

Admin starts driving the week: You spend more time chasing invoices, checking payroll, and reconciling numbers than leading the business.

Stock and debtors become invisible risks: Inventory looks like an asset until it stops moving. Receivables look healthy until collection slips.

Reporting arrives too late: By the time you review the numbers, the damage is already done.

Practical rule: If your finance function explains the past but doesn't change the next month's cash position, it's incomplete.

A good finance operator will also look outside pure accounting. Founders often need cleaner workflows, tighter handovers, and less manual friction between sales, operations, and finance. If you're trying to streamline workflows and boost success, it helps to think of a VCFO as part of your operating system, not just your reporting layer.

That broader lens matters when the owner's personal goals are tied to the business as well. If growth is meant to create freedom, not just more complexity, your finance setup should support that. That's one reason some founders also end up thinking more broadly about capital structure, risk, and long-term planning through related advisory conversations such as a private wealth advisor perspective.

What doesn't work

Some VCFO arrangements fail because they stay too high level. You get commentary, maybe a dashboard, maybe a monthly meeting. But no one owns collections cadence, stock discipline, purchase controls, or the monthly close rhythm.

That's not a CFO function. That's commentary.

The useful question isn't “Do I need a virtual CFO?” It's “Do I need someone who can identify where cash is getting trapped, then help fix the process causing it?” For many Melbourne businesses, the answer is yes well before they need a full in-house finance executive.

Pinpointing Your Exact Financial Pain Points

You can't hire well if your brief is vague. “Need better numbers” is too broad. “Need visibility” is better, but it still won't help you choose the right provider.

The useful starting point is to separate symptoms from leaks. Symptoms are what you feel. Leaks are what's causing the pressure.

Start with the symptom, then find the leak

Write down the recurring pain points in plain language. Keep it operational.

For example:

“Cash is always tight near BAS.” That may point to poor cash forecasting, tax provisioning, or slow collections.

“We're busy but margins feel thinner.” That may point to pricing drift, freight creep, discounting, or labour overruns.

“We keep buying stock but still run out of the wrong items.” That usually means weak reorder logic, poor SKU visibility, or no aged stock discipline.

“Month-end takes too long.” That often means unclear ownership, bad system setup, or manual workarounds across Xero, MYOB, inventory apps, or spreadsheets.

Don't ask a provider to “improve finance”. Ask them to reduce a specific form of friction that is costing you cash or time.

Once you've got the symptoms, group them into five buckets: cashflow, margin, stock, debtors, and reporting process. Most businesses will have one dominant bucket and one secondary one. That becomes your hiring brief.

Questions for inventory-heavy businesses

If you run e-commerce, retail, wholesale, food, importing, or manufacturing, your finance pain is often trapped in stock and gross margin rather than headline revenue.

Ask yourself:

Which SKUs make money and which only create activity?

Do you know your gross margin by SKU, customer group, or channel?

How much of your inventory is aged, slow-moving, or likely to need discounting?

Who decides reorder points, and on what logic?

Are freight, shrinkage, and write-downs visible in your margin review?

Can you explain why some items stock out while capital sits in slower lines?

If you can't answer those cleanly, you don't just need reports. You need a provider who can work between your accounting file, stock system, and purchasing process.

A practical brief for this kind of business might read like this:

Business issue | What to ask a VCFO to fix |

|---|---|

Cash tied up in stock | Build stock turns and aged inventory reporting, then tie it to purchasing decisions |

Margin erosion | Create a margin bridge by SKU, client, or channel |

Frequent stock imbalances | Review reorder-point logic and buying cadence |

Unclear landed profitability | Separate product margin from freight, discounts, and write-downs |

Questions for service and trade businesses

Service firms, agencies, consultancies, and trade businesses usually leak cash differently. The pressure often sits in work-in-progress, debtor delays, underquoted jobs, or weak visibility across teams.

Use these prompts:

Which jobs, clients, or service lines are profitable?

How long does it take to invoice after work is completed?

Do debtors slip because no one owns follow-up?

Are staff hours, subcontractor costs, and variations captured properly?

Do you know which clients consume the most management time relative to margin?

A founder's brief in this category should be blunt. “We need project profitability by job.” “We need debtors followed every week.” “We need month-end closed fast enough to make decisions.”

That clarity helps you avoid buying a generic retainer.

What your final brief should include

Before you speak to any provider, document these five items:

Primary pain point: The one issue hurting cash or time most.

Secondary pain point: The next issue that limits growth.

Systems in play: Xero, MYOB, Cin7, DEAR, Shopify, payroll tools, spreadsheets, job systems.

Operational owner: Who internally will work with the VCFO.

Success test: What would make you say “this is working” within the first quarter.

That last point matters. If you don't define success in operational terms, you'll end up measuring effort instead of outcomes.

Decoding Virtual CFO Pricing and ROI in Melbourne

Price matters. But on its own, it's the wrong decision lens.

A founder should absolutely understand market rates for a virtual cfo melbourne engagement. Then they should ask a harder question. What's the cost of continuing with poor visibility, weak controls, and delayed intervention?

What the market usually charges

One Australian guide estimates virtual CFO services at about A$1,500 to A$5,000 per month, or A$200 to A$400 per hour, while a full-time CFO in Australia is estimated at A$180,000 to A$300,000+ per year before superannuation and other employment overheads. The same guide notes this gives SMEs board-level financial control without the fixed executive cost. You can review those figures in this Australian virtual CFO pricing guide.

That's the direct price comparison. It's useful, but it still doesn't tell you whether the service is worth it.

A second pricing reference in the verified material gives a broader monthly range for virtual CFOs and a higher fully loaded annual cost for a full-time CFO once employment overheads are included. The key takeaway isn't the exact package design. It's that outsourced finance leadership is commonly positioned as a fraction of an in-house executive hire in the Australian SME market.

How to think about ROI properly

The return comes from fixing leaks that already exist.

If receivables are slow, the gain is improved collection discipline and more reliable cash timing. If stock is bloated, the gain is capital released from excess inventory and fewer panic borrowing decisions. If pricing is loose, the gain is stronger contribution margin. If month-end is messy, the gain is faster decisions and less founder time spent reconciling competing versions of the truth.

A cheap VCFO that produces elegant reports and no operational change is expensive. A higher-fee VCFO that fixes one major cash leak can pay for itself quickly.

Here's a better way to evaluate value:

Cash visibility: Can they tell you what cash is likely to do over the next few weeks, not just last month?

Control improvement: Are approvals, collections, stock rules, and variance reviews getting tighter?

Founder time: Are you spending less time stitching together numbers manually?

Decision speed: Can you make pricing, hiring, and purchasing decisions with confidence?

A short explainer can help if you want a visual take on how outsourced CFO support is typically framed in practice:

The strongest ROI cases usually come from businesses with visible friction already. Inventory-heavy operators. Fast-growing teams with poor reporting rhythm. Owners carrying the debtor chase themselves. In those cases, the value isn't theoretical. It sits in concrete process changes that improve cash and reduce noise.

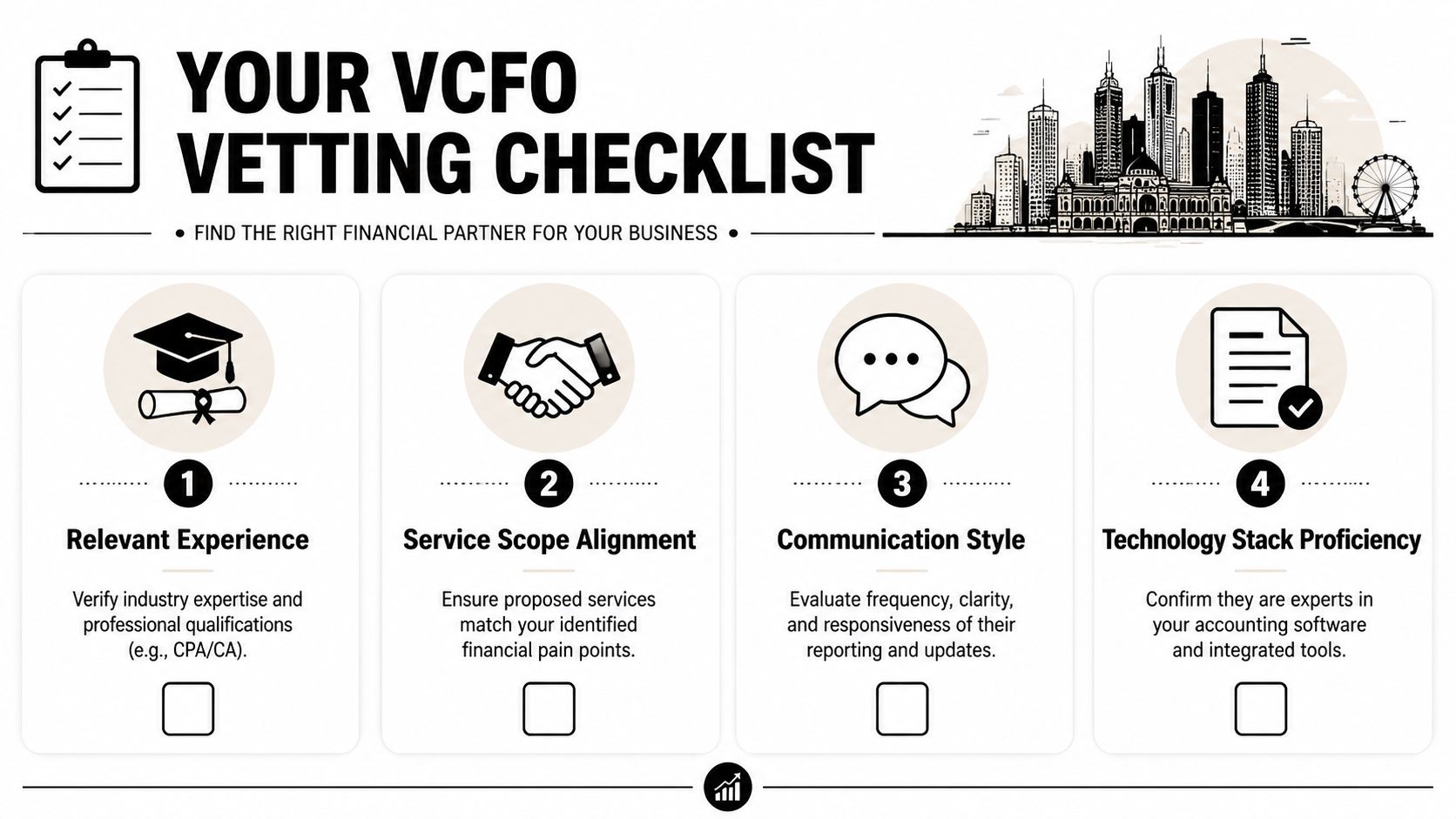

Your Checklist for Vetting Melbourne Virtual CFOs

Most founders buy too early on polish. The pitch sounds smart, the dashboard looks clean, and the provider speaks confidently about strategy. None of that proves they can fix a leaking cash conversion cycle.

The right question is simple. Can this provider move from diagnosis to execution inside the parts of the business where cash gets trapped?

What good providers can actually show you

According to this Australian guide to virtual CFO delivery, a high-performing VCFO should deliver forecasting, board-style reporting, and strategic modelling. For e-commerce, retail, and manufacturing, the technical process should include stock turns, aged inventory analysis, and reorder-point logic. The same guidance also warns that dashboards without operational ownership are a common failure, and that success should show up in improved cash conversion rather than cost savings alone.

That's exactly the standard to use in interviews.

Ask a provider to walk you through how they would handle:

Aged inventory: not just how they'd report it, but how they'd force action on it.

Debtor drift: who follows up, on what cadence, and how exceptions are escalated.

Margin slippage: how they isolate leakage by customer, SKU, job, or channel.

Forecasting rhythm: what gets updated weekly, monthly, and before key payment dates.

Variance management: what threshold triggers a conversation, and who owns the fix.

If they stay at the level of “we provide insight”, keep pushing. Insight is useful only when someone turns it into a repeated operating behaviour.

Interview questions that expose fluff

Use questions that require process detail, not philosophy.

Show me the first cashflow view you'd build for our business. What data do you need, and how often would it be updated?

If inventory is our main issue, how do you analyse aged stock, reorder points, and margin by SKU?

If debtors are late, what exact collection cadence do you implement?

What does month-end look like under your process, and who owns each step?

What will you change in our finance operations during the first month, not just report on?

Which systems do you work in directly?

How do you handle businesses where the problem sits partly in operations, not just accounting?

If the answer is mostly “we'll advise your team”, clarify whether they also help install the routine, templates, ownership, and meeting rhythm needed to make the advice stick.

Red flags are usually obvious once you ask better questions:

Generic dashboards with no intervention model

No mention of stock turns, debtor cadence, or approval workflows

Heavy focus on year-end or tax without weekly cash visibility

No clear onboarding sequence

No examples of how they work inside your software stack

Green flags are more operational:

They ask for bank feeds, AR ageing, AP ageing, inventory reports, and payroll timing early

They define who owns each recurring task

They distinguish lagging reports from leading indicators

They talk about exceptions, triggers, and routines

They're comfortable bridging finance and operations

If you want to assess the background of one option in the market, you can review Neha Malhotra's profile as part of your comparison alongside other providers. The point isn't brand preference. It's whether the person leading the work can operate at both finance and implementation level.

A simple scorecard you can use

Use a basic comparison table after each discovery call.

Evaluation Criterion | Provider A Score (1-5) | Provider B Score (1-5) | Notes & Evidence |

|---|---|---|---|

Relevant industry experience | |||

Ability to build weekly cash visibility | |||

Inventory and margin control capability | |||

Debtor management process | |||

Board-style reporting quality | |||

Technology stack proficiency | |||

Communication and response cadence | |||

Clear onboarding method | |||

Operational ownership model |

This forces evidence onto the page. It also protects you from choosing the smoothest salesperson instead of the strongest operator.

The First 90 Days A Roadmap for Onboarding

Monday morning. Payroll clears, two supplier payments hit, and a large customer invoice is still overdue. The bank balance is lower than expected, but no one can tell you whether it is a timing issue, a margin issue, or a process issue. That is the first 90 days a good VCFO should fix. The job is to create control early, then turn that control into repeatable routines your team can keep running.

Days 1 to 30

The first month is about getting to reliable numbers fast enough to make decisions this week, not next month.

Your VCFO should get access to the accounting file, bank feeds, payroll data, AR and AP ageing, tax lodgement dates, debt facilities, inventory reports where relevant, and any spreadsheet that management still relies on to fill system gaps. They also need to trace how information moves across tools such as Xero, MYOB, Shopify, Cin7, DEAR, Deputy, and Excel. That is usually where cash leaks hide. Duplicate data entry, delayed invoicing, stock adjustments posted late, and approvals that sit in someone's inbox all show up here.

By the end of the first 30 days, you should have four concrete outputs:

A verified cash position

A short list of immediate risks and cash leaks

A map of process bottlenecks across billing, collections, payables, inventory, and payroll

A weekly operating rhythm with clear owners

Ownership matters. If debtor follow-up sits with sales, invoice release sits with operations, and nobody owns disputed invoices, cash will keep slipping even if the reporting improves.

Days 31 to 60

The second month is where onboarding either becomes useful or stays stuck in observation.

A capable VCFO should now build a weekly cash view and a 13-week rolling forecast that reflects how the business runs. In a product business, that means purchase timing, supplier terms, stock cover, freight, and slow-moving inventory need to feed the model. In a services business, it means quoted work, WIP, invoicing discipline, collection patterns, contractor payments, and payroll timing must be visible. The forecast should not sit in isolation. It should connect to actions, thresholds, and accountability.

Good operators also start tightening the close process here. They reduce manual journals, clean up coding issues, set cut-off rules, and stop month-end from becoming a scramble. If you want to choose and track growth metrics, those metrics need clean source data and a routine for acting on exceptions.

A practical benchmark in this phase is simple. Can the founder and leadership team see, every week, where cash is getting tied up and who is responsible for fixing it?

Days 61 to 90

By the third month, the VCFO should be changing behaviour, not just producing reports.

This is when the forecast becomes part of management. Collections are reviewed weekly. Supplier payment timing is planned instead of improvised. Inventory purchasing follows demand and margin reality, not habit. Variance commentary points to causes and actions. If gross margin slipped, someone explains whether the problem came from pricing, waste, discounting, labour mix, or stock write-downs. If cash is tight, the team knows whether to push debtor calls, pause purchasing, re-sequence payments, or revise staffing plans.

The monthly close should also be cleaner and faster by now. Founders do not need a perfect board pack in week twelve. They need numbers they trust, fewer surprises, and enough lead time to act. For a useful reference point on the kind of reporting discipline and operational indicators that support this stage, see these business performance indicators for growing companies.

By day 90, most founders should be able to answer these questions without hesitation:

What will cash look like over the next 13 weeks?

Which customers, suppliers, or stock lines are creating pressure?

What process issue is causing the delay or leakage?

What action gets taken when a metric moves off plan?

Who owns each fix, and when is it due?

If those answers are still vague, the onboarding has not gone far enough. A VCFO should leave you with tighter cash control, clearer ownership, and less time wasted chasing numbers that should already be visible.

KPIs and Metrics That Prove Your VCFO's Worth

Monday morning is the true test. Payroll clears on Wednesday, a major customer is ten days late, and a supplier wants payment before releasing the next order. At that point, a VCFO proves their worth if the team already knows the cash position, the likely shortfall, and which lever to pull first.

A polished dashboard does not solve that problem. Clear operating numbers do.

The right KPIs show whether cash is getting stuck in receivables, inventory, weak pricing discipline, or slow internal follow-up. For Melbourne SMEs, that matters more than broad finance commentary because pressure usually builds in day-to-day operations long before it shows up in the monthly P&L.

The numbers that matter most

A useful KPI set starts with cash and works backward into the process creating the result. In practice, that usually means a small group of measures reviewed often enough to trigger action, not a large report full of lagging figures.

The core metrics usually include:

13-week rolling cash forecast: A near-term view of cash that is updated frequently and tied to actual collections, supplier commitments, wages, and tax dates.

Receivables ageing by customer: Which accounts are overdue, how long they have been sitting there, and whether someone is actively following them up.

Debtor collection cadence: Call dates, promised payment dates, disputes, and blocked invoices. This shows whether the issue is customer liquidity or your own process.

Inventory days or stock turns: How long cash sits in stock before it converts back into sales. Slow-moving lines often hide purchasing mistakes, weak reorder controls, or poor SKU discipline.

Gross margin variance: Whether margin slipped because of discounting, input costs, freight, waste, labour mix, or write-downs.

Actual versus forecast variance: Whether the business is getting better at predicting reality and whether forecast errors are being corrected quickly.

Founders who want a wider reference point on how to choose and track growth metrics should keep one rule in mind. If a metric does not help you collect faster, buy better, protect margin, or avoid a cash squeeze, it probably does not belong in the core pack.

What good reporting should trigger

Each KPI needs an owner and a response. If receivables over 30 days increase, the next step might be escalation calls, tighter payment terms, or fixing billing errors. If stock days rise, the response could be smaller purchase runs, clearance pricing on aged items, or changes to reorder points. If gross margin misses target, someone should be able to explain the cause in plain language and set a corrective action that week.

That is the difference between finance reporting and operating control.

A VCFO adds value when the metrics change behaviour across the business. Sales invoices go out faster. Credit holds are enforced. Purchasing follows demand instead of habit. Managers stop arguing about the numbers because the exceptions, actions, and owners are already visible. For a practical model of the kind of reporting that supports that discipline, see these business performance indicators for growing companies.

One caution. Do not judge a VCFO by the number of charts in the board pack or how polished the commentary sounds. Judge them by whether overdue debt falls, inventory frees up cash, forecast accuracy improves, and the business spends less time reacting late.

If your business is growing but cash still feels harder than it should, Nexist is one option to consider for virtual CFO support, growth accounting, and finance-first operational improvement. The firm works with Australian founders on forecasting, cashflow control, reporting, inventory and receivables issues, plus the systems and workflows that turn financial insight into action.

virtual cfo melbourne, cfo services melbourne, virtual cfo australia, sme financial management, growth accounting

" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="dSFdkJotL" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="wscNJE44G" transform="translate(0 0.129)" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="sTpjGo1tb" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="s7ffpmKOD" transform="translate(0 0.129)" width="24px"/><g d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.000006px" id="D0ecaHEcW" transform="translate(0 0)" width="24px"><path d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z" fill="rgb(55, 184, 218)" height="24.000006px" id="IPLFE6zXx" width="24px"/><path d="M 4.02 0 L 0 0 L 0 12.092 L 4.02 12.092 Z" fill="rgb(255, 255, 255)" height="12.09201px" id="FWhtzAyuY" transform="translate(2.863 8.375)" width="4.02px"/><path d="M 2.274 0 C 0.899 0 0 0.904 0 2.089 C 0 3.25 0.871 4.179 2.221 4.179 L 2.247 4.179 C 3.648 4.179 4.521 3.25 4.521 2.089 C 4.495 0.904 3.649 0 2.274 0 Z" fill="rgb(255, 255, 255)" height="4.17876px" id="VmOsKv4kO" transform="translate(2.625 2.545)" width="4.52095px"/><path d="M 7.641 0 C 5.509 0 4.554 1.173 4.019 1.996 L 4.019 0.284 L 0 0.284 C 0.053 1.419 0 12.376 0 12.376 L 4.019 12.376 L 4.019 5.623 C 4.019 5.262 4.045 4.9 4.151 4.642 C 4.442 3.92 5.103 3.172 6.214 3.172 C 7.667 3.172 8.25 4.282 8.25 5.907 L 8.25 12.376 L 12.269 12.376 L 12.269 5.442 C 12.269 1.728 10.286 0 7.641 0 Z" fill="rgb(255, 255, 255)" height="12.37626px" id="n1XUbhaq0" transform="translate(9.105 8.09)" width="12.268830000000001px"/></g></g></g></g></svg>)