AASB 16 Leases: Your SME Guide for 2026

Master AASB 16 leases with our practical guide for Australian SMEs. Understand the impacts on your balance sheet, KPIs, and learn how to implement it correctly.

Ansh Malhotra

You review your month-end pack, glance at the balance sheet, and wonder why debt looks heavier even though you haven't taken on a new loan. Cash in the bank hasn't changed. The business is trading as usual. Yet financial risk indicators look worse, return measures look flatter, and your lender is suddenly asking sharper questions.

For many Australian founders, that's when AASB 16 leases stops being an accounting topic and becomes a banking topic.

If your business leases a warehouse, office, vehicle fleet, equipment, or retail site, rent is no longer just a line in the profit and loss. In practical terms, the standard treats many lease commitments more like financed use of an asset than a simple monthly occupancy cost. That changes how outsiders read your numbers, and it changes what you need to explain.

Table of Contents

Why Your Leases Suddenly Matter More Than Ever

A common founder scenario goes like this. You sign a warehouse lease because stock has outgrown the old site. The business needs the space, the rent is affordable, and operationally it's the right move. Then the year-end accounts land and the business looks more indebted than expected.

Nothing “went wrong”. The reporting changed.

AASB 16 Leases became mandatorily effective for annual reporting periods beginning on or after 1 January 2019 in Australia, marking the single most significant change to lease accounting since the introduction of operating and finance lease distinctions in 1979 (HLB Australia's overview of AASB 16). That's the point where many leases stopped being disclosed only in the notes and started appearing directly on the balance sheet.

Why this matters to founders, not just accountants

Before this shift, many operating leases stayed “off the books” in the main statements. Founders still paid the rent, banks still cared about fixed commitments, but the balance sheet often looked lighter than the economic reality.

Now the numbers tell a fuller story. That's useful for lenders and investors, but it can feel brutal if you're seeing the impact for the first time.

A lease can change your reported debt position even when your cash movements haven't changed at all.

For SMEs, this lands hardest in businesses that rely on property, vehicles, plant, or specialist equipment. Retailers, wholesalers, manufacturers, trade businesses, logistics operators, and hospitality groups feel it quickly because leases are often part of how the business functions.

Your lease is also a strategy decision

This isn't just about compliance. Lease terms now shape reported debt levels, covenant headroom, and how easy your business is to explain to a bank.

That means commercial negotiation matters more than many founders realise. If you're reviewing premises terms, incentives, obligations, and risk allocation, these strategic commercial real estate insights are useful because the legal structure of the deal often drives the finance consequences later.

If you only treat rent as “monthly overhead”, you'll miss the bigger issue. Under AASB 16, the lease becomes part accounting entry, part financing decision, and part lender narrative.

The Core of AASB 16 From Two Columns to One

The easiest way to understand AASB 16 is to forget the technical wording for a moment and think about the difference between borrowing a car for a weekend and committing to use one for years. One feels like a simple rental. The other looks much closer to financing access to an asset over time.

That's the mindset shift. For lessees, the old split between operating leases and finance leases largely disappears.

What changed for lessees

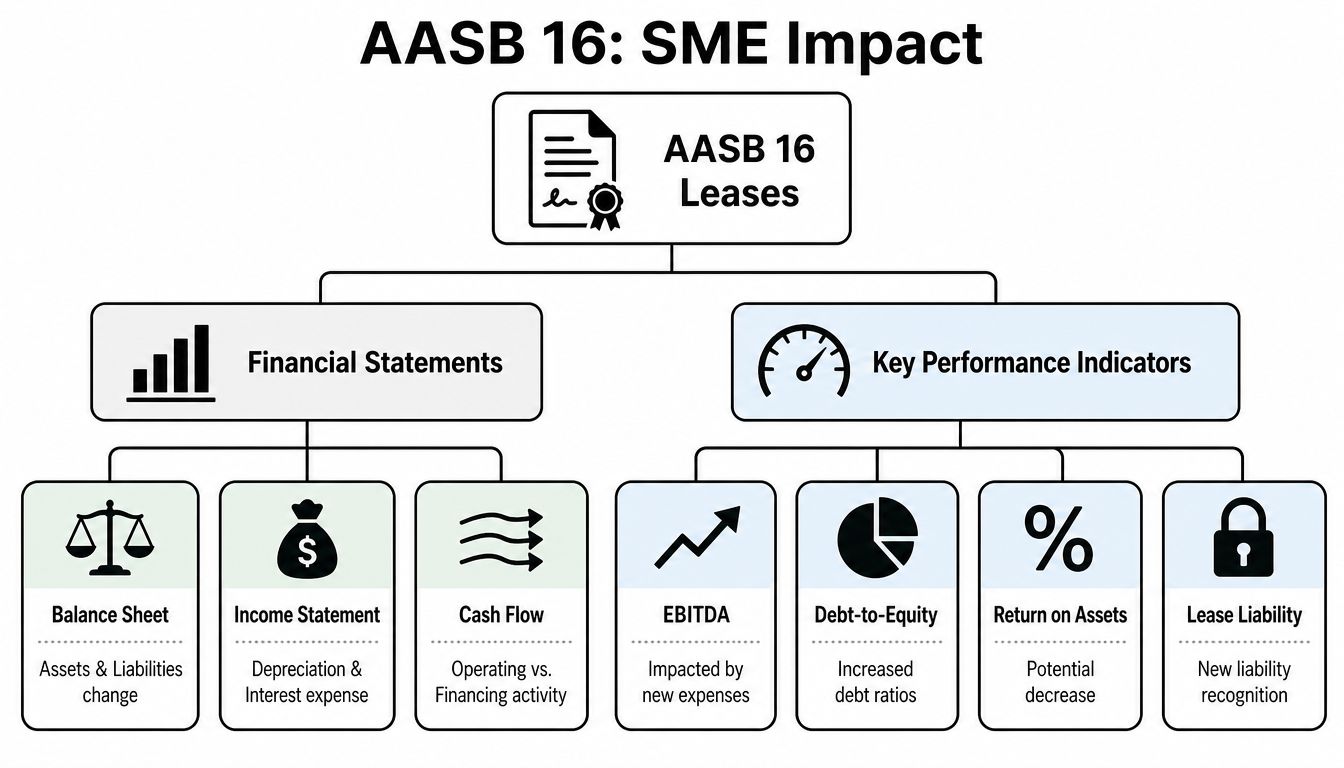

AASB 16 mandates a single lessee accounting model requiring entities to recognize a right-of-use (ROU) asset and corresponding lease liability on the balance sheet for all leases exceeding 12 months, unless the underlying asset is of low value, thereby eliminating the previous distinction between operating and finance leases for lessees (AASB material discussing the single lessee model).

In plain English, that means this:

You recognise an asset because your business has the right to use something valuable for a period of time.

You recognise a liability because your business has committed to make lease payments.

That's why founders often say, “It looks like debt appeared from nowhere.” It didn't appear from nowhere. The standard moved an existing commitment into the main statements.

A practical example helps. If you lease forklifts for your warehouse under a longer-term arrangement, AASB 16 pushes you away from treating the cost as only a monthly operating charge. Instead, it asks you to show both the right to use the forklifts and the obligation to pay for that right.

If you're exploring other financing structures around physical assets, including asset-backed furniture investments via leaseback, it's worth noticing how quickly commercial form and accounting treatment can interact.

The two balance sheet items that matter

The first new item is the right-of-use asset. Think of it as the accounting value of your access to the leased asset over the lease term.

The second is the lease liability. Think of it as the present value of what you still owe under the lease.

Practical rule: If the lease runs longer than a year and it isn't a low-value asset, start by assuming it belongs in your AASB 16 review.

This doesn't mean every lease is managed the same way in practice. Short-term rentals and low-value items can be treated differently. But for the leases that matter, the balance sheet now carries both sides of the arrangement.

AASB 117 vs AASB 16 A Snapshot for Lessees

Aspect | Old Standard (AASB 117) | New Standard (AASB 16) |

|---|---|---|

Lessee model | Two models for lessees, operating and finance lease treatment | Single lessee model for most leases |

Balance sheet recognition | Many operating leases stayed off balance sheet | Most leases over 12 months appear on balance sheet |

Asset recognised | Usually only for finance leases | Right-of-use asset recognised for covered leases |

Liability recognised | Usually only for finance leases | Lease liability recognised for covered leases |

Profit and loss pattern | Operating lease rent often recognised as a straight-line expense | Expense presentation shifts to depreciation and interest |

Short-term leases | Typically expensed | Can still be exempt if term is less than 12 months at commencement |

Low-value assets | Treatment was less central to the model | Can be exempt from on-balance sheet recognition |

Founder takeaway | Rent often looked simpler in the accounts | Lease decisions now affect leverage and balance sheet optics much more directly |

The key point isn't academic. Under AASB 117, many founders could discuss rent as a trading cost. Under AASB 16, they also need to discuss it as a balance sheet and financing issue.

Real-World Impacts on Your SME Financials and KPIs

Most founders feel the effect. AASB 16 doesn't usually change whether the lease was a good commercial decision. It changes how the decision shows up in the numbers your banker, investor, board, and management team rely on.

Balance sheet pressure without new borrowing

The first visible shift is the gross-up. Assets rise because the right-of-use asset comes on. Liabilities rise because the lease obligation comes on.

That can make a stable business look more debt-heavy overnight. If your lender watches debt-to-equity closely, the optics matter even when no fresh external borrowing occurred.

For founder-led SMEs, difficulties arise. The team knows the business hasn't taken a reckless turn, but the covenant report can still look tighter. If your banking package was drafted before AASB 16 was properly considered, you can end up arguing about form instead of discussing operating performance.

Profit and loss changes that confuse non-accountants

Your profit and loss also changes shape. Instead of a simple lease expense running through as rent, covered leases push expense presentation toward depreciation of the right-of-use asset and interest on the lease liability.

That matters because the pattern is different. Early in a lease, the interest component can make total expense recognition feel heavier than founders expect. Later, the pattern changes again.

The new model affects almost all Australian businesses and impacts reported performance metrics, incentive-based remuneration, balance sheet presentation, and stakeholder communications, with 64.3% of investors in a CPA Australia survey citing enhanced comparability as a supported benefit (discussion of the investor view and business impact).

One practical result is that EBITDA can look stronger than before, even though cash hasn't improved. That's because rent expense may no longer sit in the same place in the profit and loss. Founders need to be careful not to celebrate a cosmetic uplift.

If you want a quick refresher on how the operating result is normally read before lease presentation muddies the picture, this guide to a profit and loss statement is a helpful reset.

Here's a simple way to frame the KPI effects:

Debt-to-equity: Usually looks weaker because liabilities increase.

Return on assets: Can soften because the asset base gets larger.

EBITDA: Can improve on paper without a matching cash benefit.

Interest cover: Can shift because part of the old rent line becomes interest.

For asset-heavy operators, lease-heavy reporting also sits alongside a broader cost question. Looking at occupancy, equipment, maintenance, and replacement through a total cost lens helps. These Facility Management Insights are useful for thinking beyond the monthly lease invoice.

A short explainer is worth watching if you want the reporting mechanics in visual form:

Cash flow and covenant conversations

Cash flow is where founders often say, “So what changed?” The answer is that the economics of the lease may not have changed, but the classification and interpretation often do.

That's why I tell founders to separate three questions:

What are we paying in cash?

How is it presented in the accounts?

How does the bank define debt and covenant calculations?

Those three are not always aligned.

If your covenant definitions still assume the old presentation, fix the wording before the next awkward reporting pack lands in the lender's inbox.

Banks are usually workable when the issue is raised early and clearly. They're less flexible when they think management doesn't understand its own numbers.

Worked Examples Breaking Down the Numbers

Theory is useful. Journal logic is better. Once founders can see the flow, AASB 16 feels less mysterious.

Example one office lease on balance sheet

Take a simple office lease with fixed annual payments over a multi-year term. Under AASB 16, the business starts by measuring the lease liability at the present value of unpaid lease payments. The right-of-use asset is then usually built from that liability, adjusted for items such as initial direct costs or prepaid lease payments.

You don't need to be deep in technical accounting to understand the practical flow:

At commencement, recognise a right-of-use asset and a lease liability.

During the lease, unwind interest on the liability.

Also during the lease, depreciate the right-of-use asset.

When cash is paid, reduce the liability for the principal component and record the interest component separately.

The opening journal is conceptually:

Debit right-of-use asset

Credit lease liability

Then, during the first reporting period, you'd typically see entries along the lines of:

Debit interest expense

Credit lease liability

and

Debit depreciation expense

Credit accumulated depreciation on the right-of-use asset

When the payment goes out:

Debit lease liability

Debit interest expense, if needed depending on timing

Credit cash

That's why the numbers feel different from the old rent model. One lease now affects the balance sheet, profit and loss, and cash flow statement in different ways.

A forecasting model helps here because lease accounting doesn't live in isolation. It changes KPIs, debt presentation, and timing across periods. If you're building lender-ready reporting, a three-way forecast is the right place to integrate lease effects instead of tracking them in a separate side file.

Example two where exemptions usually apply

Now contrast that with two common exceptions.

A short equipment hire

If the lease term is less than 12 months at commencement, the short-term lease exemption may apply. In practice, that often means you continue to recognise the cost as rent or hire expense rather than bringing a right-of-use asset and lease liability onto the balance sheet.

A low-value asset

If the underlying asset is low value, the exemption may apply. A small office printer is the classic example many advisers use. In those cases, many businesses keep the accounting treatment simple and expense the payments as incurred.

SMEs often overcomplicate things. They either capitalise too much because they're nervous, or they miss major leases because they assume everything is exempt.

Don't waste time modelling every tiny office item while a property lease and vehicle schedule sit unreviewed.

A sensible working rule is to focus first on contracts that are long-term, material, and central to operations. Get those right before polishing edge cases.

Your AASB 16 Implementation Checklist

Most implementation problems don't come from debits and credits. They come from incomplete contract capture, weak assumptions, and no process for keeping the register current.

CPA Australia's post-implementation review confirms that while Australian listed companies generally consider AASB 16 working well overall, the standard has introduced high administrative costs and complexity in identifying embedded leases across diverse agreements and estimating the incremental borrowing rate (IBR) (Bentleys summary of the post-implementation issues).

That finding lines up with what SMEs struggle with. The accounting entry is rarely the hardest part. Finding every relevant contract usually is.

Phase one find every lease and lease-like contract

Start with a full contract sweep. Don't stop at documents labelled “lease”.

Look through:

Property agreements: offices, warehouses, retail sites, storage.

Equipment arrangements: plant, vehicles, forklifts, machinery, specialist tools.

Service contracts with dedicated assets: outsourcing or supply arrangements where a specific asset is effectively controlled by your business.

Old contracts with rollover terms: especially where renewal options have been exercised informally.

Embedded leases are where founders get caught. The contract might be filed under operations, procurement, or legal, not finance.

Phase two gather the inputs that drive the accounting

Once you've identified the contracts, build a clean lease register. At minimum, capture:

Counterparty and asset details: who the lease is with and what asset is involved.

Start and end dates: including extension and termination options.

Payment profile: fixed payments, timing, and anything else that affects the liability.

Initial direct costs and prepayments: these can affect the right-of-use asset.

Ownership and purchase options: if relevant to the commercial substance.

The register should live somewhere central. If one person keeps it in a private spreadsheet and no one updates it when a lease changes, the reporting will drift quickly.

Phase three calculate assess and keep it live

The most judgement-heavy input is often the incremental borrowing rate, or IBR. Under AASB 16, lessees must measure the lease liability using the IBR for each lease, which is the rate the lessee would pay to borrow funds to acquire an asset of similar value, though entities may use a portfolio rate if leases share similar characteristics, as noted in the verified source linked earlier to the investor-impact discussion.

That sounds technical, but the founder version is simpler. It's the borrowing rate that best reflects your business, the asset, and the lease term when the lease itself doesn't give you an obvious internal rate.

Use this working checklist before sign-off:

Check lease term judgement: Have you considered renewal periods you're reasonably likely to take?

Review exemptions carefully: Are short-term and low-value conclusions supportable?

Model covenant impact: What happens to debt levels and interest-based ratios?

Decide transition approach clearly: Full retrospective gives one style of comparability, modified retrospective gives a more practical path for many businesses.

Set an update rhythm: Reassess modifications, renewals, and new contracts as part of monthly close.

The businesses that handle AASB 16 well don't treat it as a one-off conversion project. They treat it as an ongoing contract-management discipline.

Tools and Processes to Manage Lease Accounting

Tool choice should match lease complexity. Not every SME needs specialised software. Some absolutely do.

When a spreadsheet is enough

If you have one or two straightforward leases with fixed terms and simple payment schedules, a disciplined spreadsheet can work. But “disciplined” is doing a lot of work there.

The spreadsheet needs version control, clear formulas, documented assumptions, and a reconciled lease register. If no one else can follow the logic after the preparer goes on leave, it isn't a system. It's a risk.

When software earns its keep

Once you have multiple sites, frequent modifications, vehicle fleets, or asset classes with different payment structures, manual tracking becomes fragile. Dedicated lease accounting software helps by automating amortisation schedules, remeasurements, disclosure support, and audit trails.

That doesn't mean software fixes bad process. It just makes a good process scale better.

Good lease accounting starts with contract discipline, not with buying another app.

For founders who already rely on finance leadership to tighten forecasting, reporting, and systems, a virtual Chief Financial Officer model is often the missing layer. Its value isn't data entry. It's setting the policy, defining ownership, and making sure lease decisions feed into banking strategy and monthly reporting.

The process matters more than the tool

Three habits make the difference:

Use one lease register: Legal, operations, and finance should all point to the same source of truth.

Assess contracts before signing: Don't wait until month-end to discover a “service agreement” contains a lease.

Review lease movements monthly: New sites, renewals, exits, and modifications should be part of close, not an annual scramble.

If you build those habits, the accounting becomes manageable. If you skip them, even the best software won't save you from messy covenant reporting and awkward audit questions.

Founder FAQs on AASB 16 Leases

Do co-working memberships count as leases

Sometimes yes, often no. The key issue is whether the contract gives your business control over the use of an identified asset for a period of time in exchange for consideration. If you're paying for flexible access to shared space rather than control over a specific office or area, it may not meet the lease test.

This is one of those areas where the contract wording matters more than the marketing brochure.

What happens when rent changes or a lease is modified

If rent changes because of a modification, extension, or other contractual update, you may need to remeasure the lease. In practice, that means your existing schedule might no longer be right.

That's why founders shouldn't file signed variations and assume finance will “pick it up later”. Lease changes need a reporting response, not just a legal file note.

Will AASB 16 affect valuation or lending

It can affect how others interpret your numbers, especially if they're looking quickly. A lender may focus on covenant definitions and adjusted gearing. A buyer or investor may normalise the accounts to understand underlying trading performance.

The practical point is this. AASB 16 rarely tells the whole story on its own. But it absolutely changes the starting point for the conversation.

If you're raising debt or discussing a refinance, explain the lease impact upfront. Reconcile pre-AASB 16 style views to current reporting so the other side can see what's commercial performance and what's presentation.

What mistake do SMEs make most often

They focus on the journal and ignore the contract population.

Founders usually assume the biggest risk is “getting the math wrong”. More often, the business misses a lease, applies weak lease-term judgement, or forgets to update a modified contract. That creates a reporting problem first, then a credibility problem.

A close second is failing to speak to the bank early. If your covenants, board pack, and monthly KPI set haven't been adapted for AASB 16, you're leaving too much room for confusion.

The best approach is simple:

Know which contracts matter

Document your assumptions

Model the ratio impact

Explain the result in plain English

That's what banks, investors, and boards need.

If your balance sheet looks heavier, your covenants feel tighter, or your reporting still doesn't clearly separate accounting presentation from cash reality, Nexist can help you rebuild the finance picture properly. Their team works with Australian founders on forecasting, cash flow, lender-ready reporting, and the operating systems behind clean decision-making, so lease accounting becomes manageable instead of disruptive.

aasb 16 leases, lease accounting, australian accounting standards, sme financial reporting, virtual cfo services

" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="dSFdkJotL" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="wscNJE44G" transform="translate(0 0.129)" width="24px"/><g d="M 0 24.129 L 0 0.129 L 24 0.129 L 24 24.129 Z M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.12890599668026px" id="sTpjGo1tb" width="24px"><path d="M 0 24 L 0 0 L 24 0 L 24 24 Z" fill="transparent" height="24px" id="s7ffpmKOD" transform="translate(0 0.129)" width="24px"/><g d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z M 6.883 8.375 L 2.863 8.375 L 2.863 20.467 L 6.883 20.467 Z M 4.899 2.545 C 3.524 2.545 2.625 3.449 2.625 4.634 C 2.625 5.795 3.496 6.724 4.846 6.724 L 4.872 6.724 C 6.273 6.724 7.146 5.795 7.146 4.634 C 7.12 3.449 6.274 2.545 4.899 2.545 Z M 16.747 8.09 C 14.614 8.09 13.659 9.263 13.124 10.086 L 13.124 8.374 L 9.105 8.374 C 9.159 9.508 9.105 20.466 9.105 20.466 L 13.124 20.466 L 13.124 13.713 C 13.124 13.352 13.15 12.99 13.257 12.732 C 13.547 12.01 14.209 11.262 15.319 11.262 C 16.773 11.262 17.355 12.372 17.355 13.996 L 17.355 20.466 L 21.374 20.466 L 21.374 13.532 C 21.374 9.818 19.391 8.09 16.747 8.09 Z" fill="transparent" height="24.000006px" id="D0ecaHEcW" transform="translate(0 0)" width="24px"><path d="M 24 3 C 24 1.344 22.656 0 21 0 L 3 0 C 1.344 0 0 1.344 0 3 L 0 21 C 0 22.656 1.344 24 3 24 L 21 24 C 22.656 24 24 22.656 24 21 Z" fill="rgb(55, 184, 218)" height="24.000006px" id="IPLFE6zXx" width="24px"/><path d="M 4.02 0 L 0 0 L 0 12.092 L 4.02 12.092 Z" fill="rgb(255, 255, 255)" height="12.09201px" id="FWhtzAyuY" transform="translate(2.863 8.375)" width="4.02px"/><path d="M 2.274 0 C 0.899 0 0 0.904 0 2.089 C 0 3.25 0.871 4.179 2.221 4.179 L 2.247 4.179 C 3.648 4.179 4.521 3.25 4.521 2.089 C 4.495 0.904 3.649 0 2.274 0 Z" fill="rgb(255, 255, 255)" height="4.17876px" id="VmOsKv4kO" transform="translate(2.625 2.545)" width="4.52095px"/><path d="M 7.641 0 C 5.509 0 4.554 1.173 4.019 1.996 L 4.019 0.284 L 0 0.284 C 0.053 1.419 0 12.376 0 12.376 L 4.019 12.376 L 4.019 5.623 C 4.019 5.262 4.045 4.9 4.151 4.642 C 4.442 3.92 5.103 3.172 6.214 3.172 C 7.667 3.172 8.25 4.282 8.25 5.907 L 8.25 12.376 L 12.269 12.376 L 12.269 5.442 C 12.269 1.728 10.286 0 7.641 0 Z" fill="rgb(255, 255, 255)" height="12.37626px" id="n1XUbhaq0" transform="translate(9.105 8.09)" width="12.268830000000001px"/></g></g></g></g></svg>)